As calls grow louder for Fed action to help rein in inflation, it’s important the public understands what’s at stake and what, precisely, it is that some commentators are suggesting in terms of policy action.

In “Fed, Biden Risk Credibility Crisis With Inflation Cliffhanger,” I wrote that almost without exception, the people arguing for a Paul Volcker-style response to inflation are people who wouldn’t be affected by the ensuing recession.

That’s a crucial point. It’s highly unfortunate that financial media outlets and (especially) mainstream news networks don’t alert readers and viewers to that reality.

It’s very easy for Fed critics to make a compelling case for draconian policy action by framing the issue as a decision between paying higher and higher prices for groceries and accepting slower overall economic growth. If you ask a random voter whether they’d accept a period of below-trend growth if it means not paying $6 for a gallon of milk, they’ll generally say “yes.” Determining what below-trend grow might mean for one’s personal economic circumstances requires extrapolation, whereas you don’t have to do any extrapolating to understand what surging grocery prices mean for your wallet.

Note that neither outcome matters much for someone like Larry Summers or Jeremy Grantham (both of whom weighed in on this debate last week). Recessions are irrelevant for multi-millionaires and billionaires. So is $6 milk.

For everyday people, there are two key interrelated points.

First, it’s not clear that a gradualist Fed can make much of a difference when it comes to arresting price pressures as they’re currently manifesting in the US. That’s because rate hikes won’t help get container ships unloaded or otherwise help much when it comes to alleviating the well-documented supply chain bottlenecks and labor market frictions currently bedeviling the world’s largest economy.

Second, to the extent the Fed can make a difference given the current conjuncture, it would be through engineered demand destruction. Or, more colloquially, squeezing the economy such that everyday people aren’t in a position to keep consuming goods and services. As demand collapses, the proverbial tea kettle comes off the boil and eventually, price pressures abate as producers catch up, rebuild inventories and so on.

Sundry multi-millionaire and billionaire Fed critics (some of whom are being paid by media outlets like Bloomberg to weigh in on what the Fed should and shouldn’t do) are effectively saying the following to everyday people: Suffer through an engineered recession — if you were smarter, you’d know it’s for your own good. (Note that no media outlet is offering you a paid contributor gig to weigh in.)

In a November 12 note, BofA’s Ethan Harris took a useful trip down memory lane in the course of differentiating between what he called “good and bad tightening cycles.”

Central banks, Harris said, can either be a “good cop” or a “bad cop.”

“Good cop” central banks “set out to normalize rates and back off if there are signs that the market or economy ‘can’t take it.'” “Bad cop” central banks “deliberately try to cool the economy and markets as a way of fighting unwanted inflation.”

To be sure, there are good arguments for a “bad cop” approach. But considering it’s been more than 40 years since the US has witnessed such a deliberately restrictive domestic monetary policy stance, it’s at least worth letting the public know that just as there are serious risks associated with a central bank that purposefully stays behind the curve at the risk of allowing inflation to spiral, there are also risks associated with draconian action aimed at strangling inflation by throttling demand.

After noting that the Fed’s response to rising prices in the post-pandemic era has so far been “remarkably benign,” BofA’s Harris wrote that,

History suggests that at some point next year, the Fed will have to shift gears. If inflation settles in near the planned overshoot they can move from uber dovish to mildly hawkish. If inflation settles above the planned overshoot they will need to become much more hawkish. That means either accepting a natural correction in the markets and economy or deliberately inducing such a correction. The Fed will want to warn the markets well in advance of actually hiking rates. Moreover, once the Fed gets going it will likely hike faster than the market expects.

The message for everyday folks is that the “bad cop” approach to addressing higher prices won’t be painless.

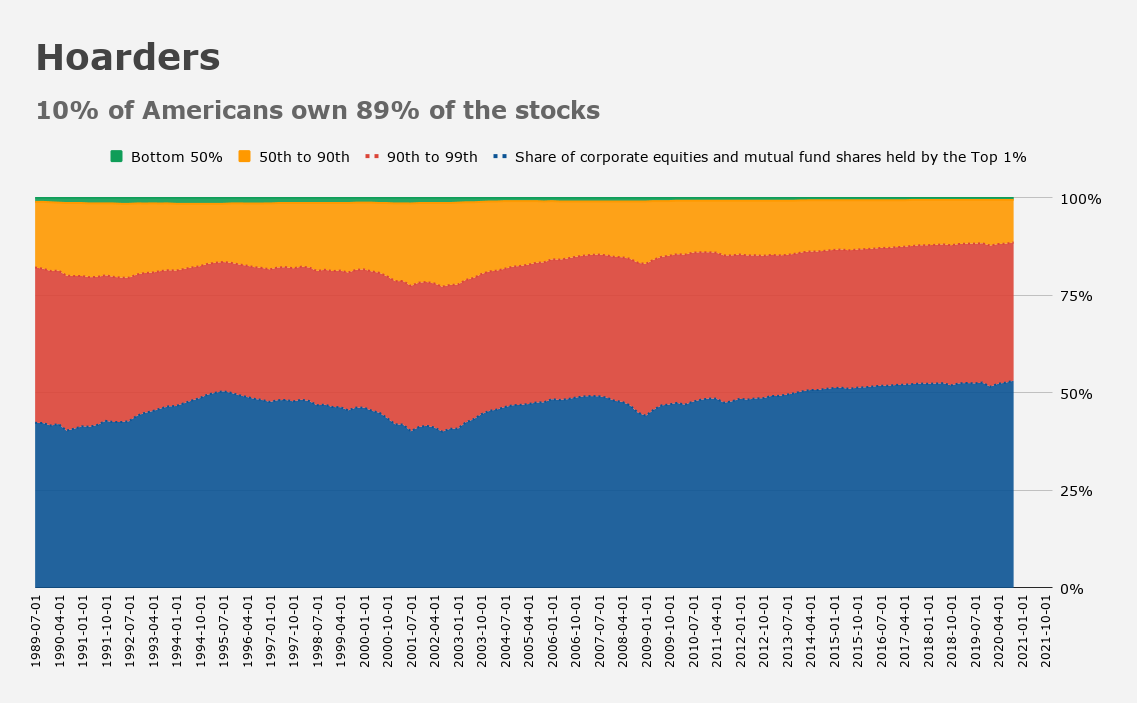

Advocates of such an approach often point to the unequal distribution of financial assets (which are overwhelmingly concentrated in the hands of the wealthy) as evidence that, at least as far as market fallout is concerned, rich people would shoulder the lion’s share of the burden. But that misses two critical points.

First, someone with a $50 million stock portfolio can absorb a 50% decline and still have $25 million. Such a person was rich before the crash and remains rich in its aftermath. Someone with a $50,000 stock portfolio who suffers a 50% decline is left with just $25,000. Such a person was “on their way” before the crash, but in its aftermath is left with barely enough to cover one year’s mortgage payments.

Second, engineering a market correction in a vacuum (an impossibility, but let’s pretend), wouldn’t be sufficient to arrest rising prices, because it likely wouldn’t have a large enough impact on aggregate demand. The problem with the vaunted “wealth effect” (the supposed “trickle down” dynamic that translates rising stock prices into consumption) is that the people who control the vast majority of corporate equities are those with the lowest marginal propensity to consume. Crushing their portfolios will affect demand for things that don’t matter — things like fine art, trophy watches and super yachts.

For regular people, a dramatic decline in stock prices that’s confined to Wall Street is a gut punch to 401(k)s, but just as the inexorable rise in equity prices post-financial crisis wasn’t accompanied by broad-based gains for the middle class or scorching-hot economic growth, neither will a controlled demolition of the stock market necessarily entail the kind of across-the-board demand destruction necessary to bring down inflation. For that, you need to engineer a real recession in the real economy that hurts real people. (So, not the people you see advocating for such an approach on financial television.)

None of the above should be construed as an argument in favor of a Fed that throws caution to the wind vis-à-vis inflation. Unlike so many of the folks you see quoted in the mainstream media or shouting for a Volcker-style policy pivot on populist finance blogs, I openly admit that whatever approach the Fed takes, it almost surely won’t affect me in such a way as to render my life less comfortable.

The point is simply to reiterate that the risks are two-way. You just wouldn’t know it from listening to pundits, who are increasingly prone to insisting the Fed engineer a recession in order to tame inflation. Note that critics almost never use the phrase “engineered recession.” Saying that would make their arguments seem much less convincing to everyday folks.

“Investors’ perception [is] that positive economic progress, combined with the realized upside risk for inflation at this point in the cycle has served to reinforce the case for the Fed to pull back from the emergency policy stance currently in place,” BMO’s Ian Lyngen and Ben Jeffery wrote late last week.

They went on to dryly note that “the mixed track record of central bankers in prior attempts at orchestrating soft landings (i.e. almost never) implies there is a real risk of overshooting on the tightening cycle at this stage in the recovery.”

{kind=link}

Evidently, Musk, Bezos, and Zuckerberg are now all selling shares.

Presumably, the money will not be sitting in cash, and has to be put somewhere.

Diversification away from mega-cap tech stocks, and into what?

We should be careful about lumping everyone who suggests tight(er) policy together. We’re near record lows for real yields. There has to be some middle ground between easy money and draconian tightening.

“There has to be some middle ground between easy money and draconian tightening.”

Oh, there is. But mainstream financial media doesn’t like to talk about that because it doesn’t sell or generate clicks and most of your popular financial blogs rely on bombast and conspiratorial narratives to sustain their readership, so “middle ground” is anathema. 🙂

Something that bothers me the most, is the Trump tariffs are not brought up as the cause for inflation. Keeping interest rates at the zero bound for as long as they have will cause inflation eventually. It seems like we are heading for a recession because high prices does cause demand destruction, unless you are talking about, the food you need to eat to survive, the oil to heat your house, or the gas you need to get to work.

H-Man, you have to wonder if the fed tightens, demand drops, maybe not so many bottlenecks. The problem is does it take one aspirin or two to make the headache go away.