It’s too early to retreat into your backyard doomsday bunker.

In general, but also vis-à-vis your strategic bias in markets.

According to Goldman’s Zach Pandl and a long list of colleagues, growth is likely to slow in the second half of next year, but should stay a semblance of robust in the near-term, while central banks aren’t likely to tighten aggressively.

That means that although winter could present new challenges including another COVID wave or energy shocks, it’s “premature to take a defensive stance already.”

The message was delivered via the 2022 edition of the bank’s “Top Ten Themes” series, an annual exercise. Number three on the list was “Too early for the risk bunker.”

The key point is that although the fiscal impulse is set to wane, “continued COVID-related medical improvements, pent-up saving and inventory rebuilding should keep growth at an above-trend pace at least for the early part of next year in the major economies.”

There are caveats. There always are. In this case, the market has already upgraded its growth view. Or at least according to the bank’s growth factors (figure below).

Between that and the distinct possibility that COVID cases could rise over the winter months while energy markets remain turbulent, Goldman conceded that “the path for cyclical assets [may be] bumpier than it has been in the last two months.”

Still, the bank reckoned, it’s “premature” to turn “completely defensive.”

I’d be remiss not to note that the bond market hasn’t exactly been screaming “pro-cyclical” lately. Rather, it’s been shouting something about a growth scare, a policy mistake or a combination of the two. At the same time, Wednesday’s theatrics underscored the potential for fireworks in the event inflation continues to surge.

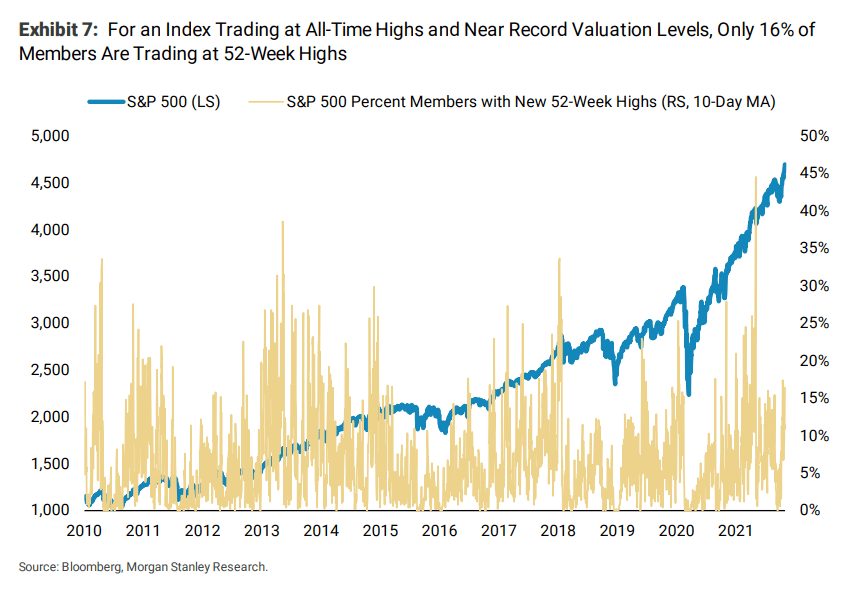

Equities are fine, though, caught up as they are in another options-driven, “YOLO”-inspired melt-up on poor breadth. Of course, given new record lows in reals (figure below), what do you expect?

As one strategist told Bloomberg this week, “we maintain a pro-risk positioning simply because we believe real rates are going to remain negative and therefore the overall monetary policy is going to be accommodative for months to come.”

In addition to the contention that a strategic pro-cyclical stance remains appropriate (or at least as it relates to developed markets in the near-term), other themes for 2022 from Goldman include the notion that the pace of growth will slow as the recovery moves “from a sprint to a marathon.”

Relative to bonds and credit, valuation constraints are less binding on stocks, the bank said, but cautioned that their “model of macro valuation in equities suggests that rising yields and underlying inflation, together with a slowing in the rate of labor market progress, are pushing ‘macro-consistent’ valuations steadily lower, and the market has started to look expensive relative to macro conditions on these measures for the first time in the cycle.”

The bank mentioned supply constraints. Markets have priced in some inflation and rate risk, so in the event supply frictions ease, risk assets could stage a relief rally, but Goldman noted that because “markets looked through a large portion of transitory inflation risk, so should [they] discount easing inflation to a degree.”

Additionally, Goldman predicted persistent tightness in commodity markets (to the obvious benefit of commodity-linked assets), said market participants will be forced to ponder the “once unthinkable” prospect of an ECB exit from negative rates over time, cautioned that Chinese authorities may countenance slower growth and suggested divergent paths out of the pandemic will lead to rotations and nonlinear shifts at the sector and country level.

Finally, when it comes to risks, it’ll be “the usual suspects,” the bank said.

“COVID-related risks [are the] most obvious ‘deep challenge’ to the cyclical picture,” Goldman remarked, adding that “other macro risks include US fiscal drag, China’s deleveraging, and more persistent inflation and rate pressures.” Investors should be wary of politics, the bank warned, before helpfully noting that “hedging this collection of risks [is] more complicated than normal.”

There’s a disparity, Goldman mused, between “unusually high macro volatility and lower asset volatility.” Assuming markets “keep their faith in the broad destination,” that disconnect can be resolved in benign fashion, with macro volatility settling down.

However, Pandl closed the 26-page piece by saying simply, “The flip side is that markets are still vulnerable to anything that shakes confidence, particularly more challenging news on the health front or more persistent underlying inflation pressure.”

{kind=link}

I’m confused how the market has priced in inflation? Sure, we’re seeing record highs almost daily so that speaks to the higher profit side of inflation. But what about the forthcoming reductions in sales? That certainly doesn’t seem to be priced in at all. Either that or we’re going to see massive credit spikes and then we’re looking at increasing defaults which could become systemic. Either way, I still don’t see how indeterminent

indeterminant transitory inflation that should well continue through 2022 has been priced in or even accounted for.