Earlier this week, in “2018 Redux?“, I talked a bit about a possible parallel between Q4 2021 and the infamous mini-bear market that played out three years ago at the end of what, if you measure from the post-GFC lows in the shadow rate, was among the most acute Fed tightening cycles in history.

If there’s an analogue, it involves the Fed (and other central banks) tightening into a slowdown with equities perched near record highs on extreme multiples.

BofA thinks it’s at least possible that stocks could experience a “prolonged grind lower, à la Q4 2018,” as distinct from the “sharp collapses” seen in and around “Volpocalypse” and the COVID shock.

In a note out Friday, SocGen’s Albert Edwards also warned of a correction and suggested a global recession might be in the offing. In itself, that’s not really news. I’m not sure I can remember a time when Edwards didn’t profess to believe a downturn might be imminent. This time, though, he brought along some arguments about the interplay between monetary policy and energy costs that are worth a quick mention.

The world is, of course, facing an acute energy crunch which this week manifested in, among other things, a spike in European gas prices so absurd that Vladimir Putin felt compelled to verbally intervene, if only to set the stage for the Kremlin to exploit the crisis for geopolitical gain. In China, things are arguably even worse and analysts have spent the last several weeks cutting estimates for the world’s second-largest economy. Sharply higher gas prices fed the rally in crude, which traded at multi-year highs this week. OPEC+ exacerbated the situation by declining to increase production beyond the scheduled November hike.

“High energy prices will hugely impact the debate about whether the post-pandemic surge in inflation is transitory or permanent,” SocGen’s Edwards said Friday, adding that “fears of a price/wage spiral seem much more realistic as ultra-tight labor markets conspire with households being bludgeoned by higher energy prices and the cost of living more generally.”

One major takeaway from the September jobs report in the US was that the labor market remains woefully out of balance. An underwhelming headline print suggested labor supply hasn’t even begun to catch up with demand, while an above-consensus read on average hourly earnings underscored wage pressures.

Evidence that inflation is likely to stick around longer than expected (especially considering the surge in energy prices) has prompted central banks to take steps towards policy normalization, whether it’s the forthcoming Fed taper, the BOE’s hawkish turn or hikes from Norway and New Zealand. (As a quick aside, the RBNZ hike was really just August’s aborted hike on a delay. A snap lockdown prevented the bank from raising rates two months ago.)

This sets up a potentially unpalatable macro conjuncture. “As energy prices surge with a backdrop of central bank tightening, it’s starting to feel a bit like July 2008,” Edwards remarked, recalling “unparalleled central bank madness as the ECB raised rates just as oil prices hit $150 and the recession arrived.”

At the same time, the fiscal impulse is poised to wane, even if Democrats do manage to come to terms on a compromise that advances Joe Biden’s economic agenda. Edwards called the US “particularly vulnerable with the OECD estimating a huge fiscal tightening next year.”

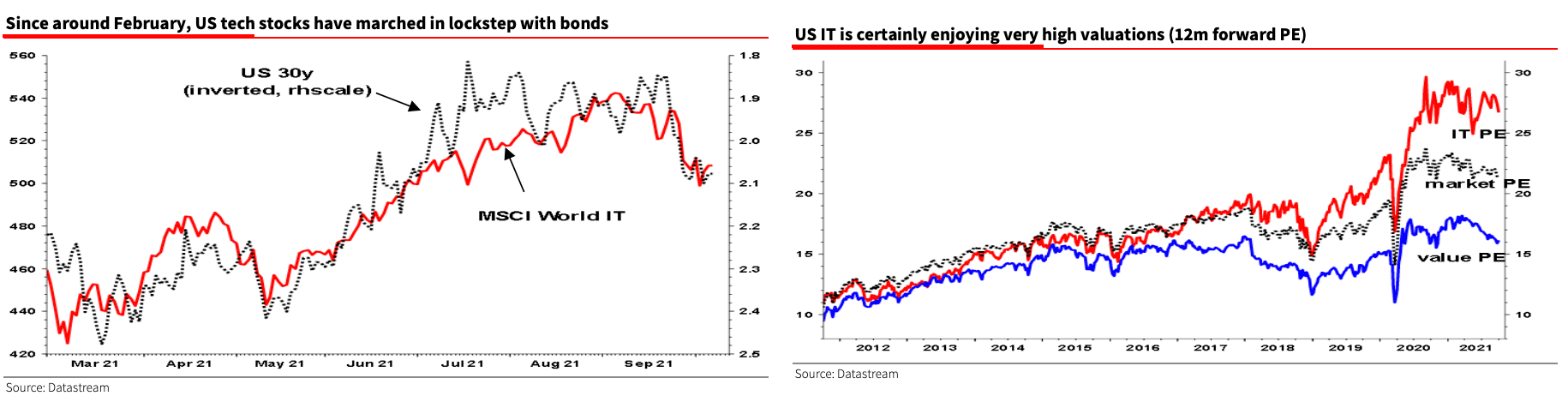

What does all of this mean for stocks? Well, the read-through is as straightforward as it is familiar. First, higher yields (whether as a result of surging energy prices or something else) are a drag on the market’s most important stocks. Albert cited “an old friend” who reckoned that if long-bond yields in the US hit 2.4%, tech stocks could dive 15%.

Beyond that, though, Edwards recapped a set of familiar talking points about the extent to which some tech names are merely masquerading as growth stocks when they’re really cyclicals.

“Yes, the US tech sector has enjoyed extraordinarily robust profit growth, particularly during the 2020 COVID recession, but that allowed the tech cyclicals to continue in the pretense that they were also ‘Growth’ stocks by turning in a robust profit performance,” he said, warning that “an ordinary recession would put these ‘growth’ imposters to the sword, just as they were in 2001.”

Ultimately, Albert suggested equity investors “should think hard about the likelihood that higher energy prices and bond yields will trigger a ‘wholly unexpected’ recession.”

As for the 2018 analogue and a possible Powell Pivot Part Deux, Albert wrote that even though a move up to, say, 2.25% on US 10s wouldn’t “violate the bond bull market, it would certainly feel like a violation to equity investors, and particularly to tech investors who have built nosebleed valuations on ultra-low bond yields.”

Any derating that might accompany such a yield spike “could yet see a December-2018-like Powell Pivot just weeks into a Fed Taper,” he said.

H-Man, you have to love Albert, perma bear frozen in the arctic, but always great data to back up the opinions and then, always, a touch of history.

I was amusing myself last week trying to estimate the empirical duration of some FAAMNG stocks based on the last couple of months. It was huge, like 20-30 I think. Those stocks do discount substantial (impossible) terminal growth rates, if you do a reverse DCF. But not enough for that level of duration. So either their duration is super non-linear (convex) or most of their correction so far reflects something other than mere yields (sniffing a recession?)

The energy shortages in China and Europe feel somewhat self inflicted. China is trying to reduce domestic coal mining while boycotting Australian coal, UK has hardly any NG storage (or native gasoline lorry drivers?), Europe competes with UK for NG, energy price controls muffle conservation signals, fragmented and deregulated utilities whose plan B is to go BK. Reminds one of Texas, people freezing and seeing deregulated utilities go BK while neighboring states had plenty of electricity.

Meanwhile, US storage levels look okay, but much of the embedded energy we consume is in imports. I do think energy prices are a bigger inflationary threat than higher wages for waiters and cooks. The Fed’s job is getting harder.

I know the models show what they show, but somehow the idea that 2.4% on the long bond would crash tech stocks is logically silly to me. Besides,those stocks need a bit of a house cleaning anyway.