We’re back to worrying about whether the mega-cap leadership can stomach higher bond yields. “Mega-cap tech getting hit as Treasury yields climb,” read one headline on Monday.

A couple of weeks back, in the course of recapping a series of familiar talking points, I mentioned that the biggest risk from extreme index concentration might not necessarily be the concentration itself, but rather the extent to which the secular growth trade (of which mega-tech is representative), is tethered so closely to rates and the curve.

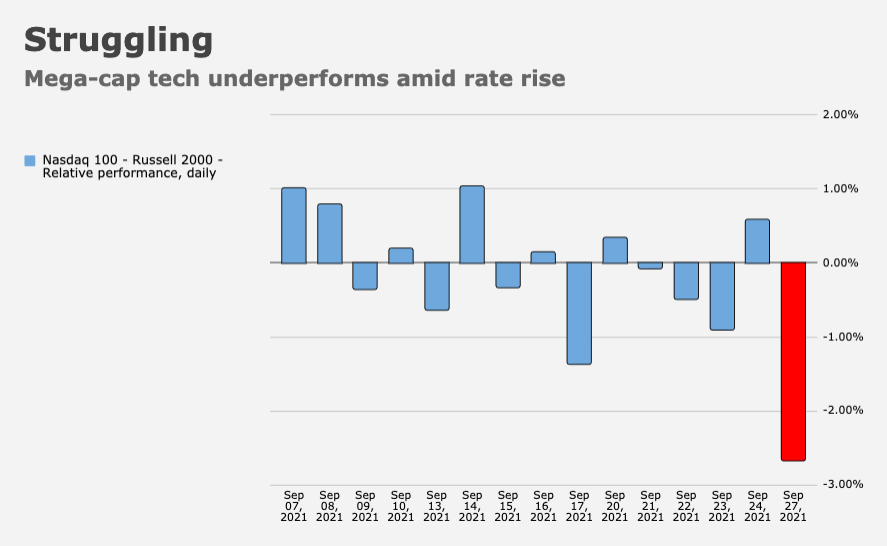

With 10-year yields back near 1.50% Monday, it wasn’t terribly difficult to explain large intraday underperformance for the Nasdaq 100 versus, say, the Russell 2000 (figure below).

When you think about rates you really need a nuanced take here, though. In addition to considerable ambiguity about which factors mattered most in explaining last week’s “delayed reaction” to the September FOMC, the breakdown matters.

“Real yields have been marching higher recently as it continues to look more like the broad rates selloff has been a risk premium trade, as opposed to a view on heightened or accelerating growth or inflation expectations, particularly with the latter going nowhere but sideways since the start of June,” Nomura’s Charlie McElligott wrote.

Two- and five-year yields hit the highest since April 2020 and February 2020, respectively, ahead of what ended up being a soft two-year sale and a decent five-year auction.

“We’re apprehensive of assuming that the US rates market will simply pick up where we left off in late March when 10-year yields reached 1.77%,” BMO’s Ian Lyngen and Ben Jeffery said, noting that although they’re “content with a decidedly bearish skew for the time being… a straight shot to >2.00% 10s is difficult to envision” considering the long list of familiar macro headwinds and likely dip-buying interest. They’re most bearish on fives, for obvious reasons. “The realities of the Fed’s SEP have created a floor for five-year rates, for all intents and purposes,” they remarked.

You can write your own script when it comes to explaining higher yields and you’ll be able to find something, somewhere to justify it. As noted here late last week and again over the weekend, the multitude of potentially relevant factors means the number of plausible narratives is essentially limitless.

That said, Nomura’s McElligott suggested there’s “an important message with regard to the move higher in nominal yields being more about real yields and ‘tight’ Fed policy down the road, versus some potentially misinterpreting the higher nominal yields as a pure read on ‘reflation’ trade dynamics or that sentiment for ‘above trend growth’ is picking back up again.” The simple figure (below) helps illustrate the point.

Ultimately, though, the result is the same. “Regardless of the ‘true’ catalyst versus narratives, it’s bearish for bonds either way, and that’s driving a thematic trade in equities which has many nervous, because most have legged-back into the duration-proxy ‘Growth’ equities versus reducing ‘Cyclical Value’ over the course of this past quarter,” Charlie went on to write.

And that brings us full circle. It’s back to wondering whether the “broad” market can make new highs in the face of higher yields. One way or another, the burgeoning bond selloff could be construed as bad news for secular growth tech. If reals are rising, it’s a threat and if we actually do get a reinvigorated reflation trade, that’s bad news too because then the macro rationale will favor a rotation back to cyclicals and re-opening plays.

“A collapse in bond yields, we believe on the back of the Delta variant, halted the previous Value rally, but as we write today, with yields rising, Value is very much in the ascendency, while the Nasdaq and Quality stocks are in the red,” SocGen’s Andrew Lapthorne said Monday. “So, in a multi-asset context, Value is important not just because of its relative cheapness to other stocks, but also due to its ability to make money when bond yields are on the rise.”

If the mega-caps can’t hold up, that’ll make it more difficult for the benchmarks to rise, creating a bit of diversification desperation if you’re relying on a simple 60:40. Indeed, a simple version of that mix is down almost 1% this month, the most in nearly a year.

In between pendulum swings, time ticks away …

Summarised in the slogan “We can know more than we can tell”, Polanyi’s paradox is mainly to explain the cognitive phenomenon that there exist many tasks which we, human beings, understand intuitively how to perform but cannot verbalize the rules or procedures behind it.[2]

This “self-ignorance” is common to many human activities, from driving a car in traffic to face recognition.[3] As Polanyi argues, humans are relying on their tacit knowledge, which is difficult to adequately express by verbal means, when engaging these tasks.[2] Polanyi’s paradox has been widely considered a major obstacle in the fields of AI and automation, since the absence of consciously accessible knowledge creates tremendous difficulty in programming.[4]

Just one thought, barely related to the post but this is a convenient place to put it.

“Delta” is over, as a market factor. The US new case curve peaked two weeks ago and is plunging. Other Covid metrics – deaths, hospitalizations, whatever – are lagging so don’t matter (to the markets). Look at stocks: vaccine and Covid test names are rolling over while reopening names are hooking up.

This shouldn’t be a surprise. We’ve discussed before that “peak Delta” would be in September.

Delta was one of the two largest risk factors in the last few months, and its end is bullish. A bad Fed surprise was the other largest risk factor, but that’s also largely receded; the coming taper is no longer a “surprise”, if it ever was.

There are, as always, new things to worry about. China power shortages, debt ceiling, more Evergrande fallout, etc. None of these are as threatening as the pair of Delta & Fed were.

For me, the only believable reasons that Delta should be over, is that either we have achieved herd immunity, or that vaccination rates are up.

If not, then we’re just set up for the next wave after this one.

I don’t have a strong opinion about whether there will be a next big Covid wave in the US.

The argument for “no” is that some 80-90% of US has some degree of immunity now, from vaccination or from having had Covid (that is the claim, I haven’t done the modeling).

The argument for “yes” is that immunity wanes and new variants can develop a degree of immune evasion.

Stock behavior suggests that investors favor “no”, because companies are generally not being rewarded for clinical data, EUA, or even approval of new Covid therapeutics or vaccines. Granted, investors are not necessarily gifted at predicting pandemic behavior.

The situation varies by country. Asia is in a different boat. India likely has even more widespread immunity than the US.

The point, though, is that whether there is a next Covid variant wave with a different Greek letter, or not, Delta’s wave in the US is ending. In the real world, it is declining weekly. As an investment risk, it’s over.

In October 2018 we saw the same dynamics. Yields rose and equity ignored it for some days on the narrative that yields hinted at solid growth and rising EPS could absorb the yield rise. Then the oil debacle came, linked also to the Kashoggi murder matter. Suddenly the narrative made a 180° upside down turn, and it changed into the spectre of rising yields + deflation, equity was mistakening the real reasons for the oil debacle and assuming it was a sign of global slowdown. Let’s see if Evergrande + chip shortage + energy crunch changes that again. Oddly oil was at 80$, same level as today.

I add that central banks + fiscal policies can sustain demand, they are impotent if the shock comes from supply.

Personally I think a secular equity decline will start in some months but we will see a final surge before that. Current energy/supply chain issues will be solved, it’s like a queue forming after an accident on a highway. Even if cars 10 miles ahead are moving slowly you are still. There is whole math explaining how a queue forms, develops, and slowly dissolves.

The reasons I believe a stock market decline is coming is for another comment another day