Earlier this week, while documenting yet another sobering, if not totally depressing, outlook piece suggesting returns for US equities are likely to be lackluster over the next decade, I briefly mentioned Goldman’s characterization of the post-World War II investment landscape as a story of “three long ‘super cycles.'”

The bank’s Peter Oppenheimer contends we’re currently at the end of the third super cycle and that going forward, a trio of factors together argue for lower returns on the index.

Those factors are: Valuations, low rates and high margins.

Read more: ‘We’re At The Opposite End Of A Stock Super-Cycle,’ Goldman Says

The corollary is that the three super cycles began under the opposite conditions. It’s worth highlighting a few additional points from the bank’s strategy paper on the post-pandemic cycle considering the growing chorus of warnings about poor long-term prospects for stocks.

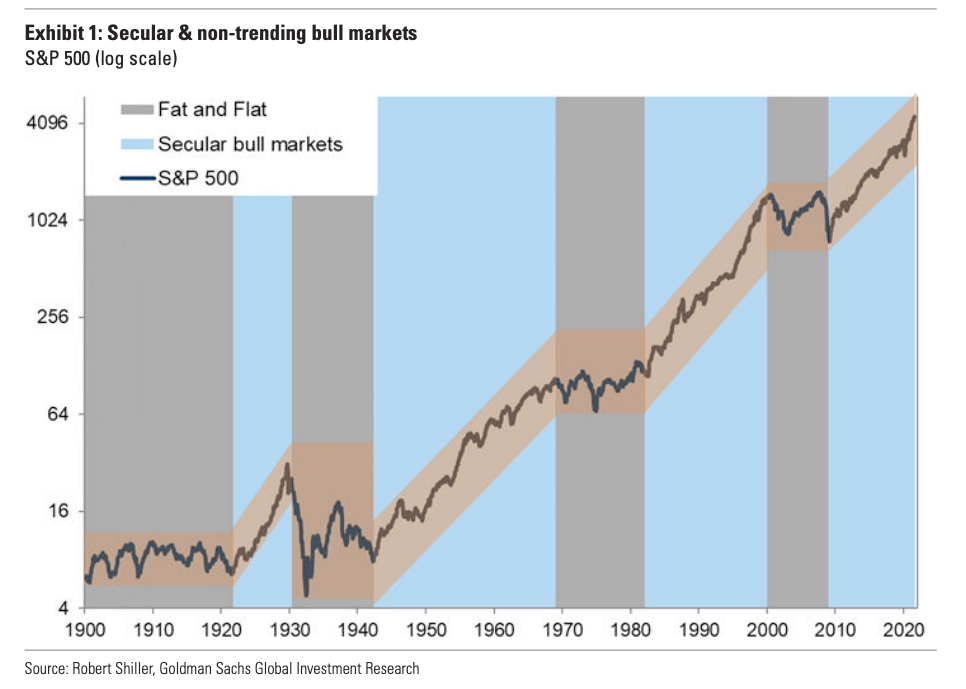

The figure (below, from Goldman) shows you the three long super cycles, which Oppenheimer emphasized have been “punctuated by occasional sharp drawdowns and often quite sharp ‘mini’ bear markets.”

Despite the drawdowns, bear markets and intermittent crises, Goldman still conceptualizes the three periods as constituting “secular super cycles” (which, incidentally, is also what Tesla will call its first motorcycles).

The key to understanding these cycles is that they benefited from key structural tailwinds and accelerants, some of which are unlikely to be present or persist in the decades ahead.

While not pretending to offer any revelations, it’s worth pointing out the obvious, if only because we tend to take things for granted until those things disappear — no matter how many times we remind ourselves that our current favorable conditions aren’t guaranteed to persist. (That’s a needlessly circuitous way of repeating the old adage, “You don’t know what you’ve got ’till it’s gone.”)

Goldman walked through the three “super” periods.

The 1945-1968 post-war boom was characterized by an “economic environment conducive to strong returns in equity markets [while] valuations also recovered from their post-war levels aided by a secular decline in the equity risk premium as many of the risks to the global system faded.”

Between 1982 and 2000, disinflation and moderation were the key macro themes, while valuation expansion “pushed up both equity and fixed income returns at the same time,” the bank wrote.

Meanwhile, the US and the UK embarked on the long road towards establishing capital’s dominance at the expense of… well, at the expensive of pretty much everything else. Or, as Goldman politely put it, the world witnessed “a wide range of deregulation, reform and privatization under the Reagan and Thatcher administrations.”

Oppenheimer went on to note that “not only did interest rates stay low as a result of the purging of global high inflation, but the end of the Cold War helped push the equity risk premium down further.”

Finally, Goldman recapped the “2009-onwards” rally. I doubt most market participants need a retelling of that story.

The key is that, as Goldman emphasized, “each of these have in common a combination of low starting valuation, falling or low cost of capital and a low starting margin.”

By contrast, the current conjuncture finds valuations stretched to historical extremes and margins at records.

“Generally, strong economic growth and regulatory reforms also played a part in reducing the risk premium in equity markets [and] in the decades from 1980, a combination of supply-side reforms, technological change and globalization also pushed up margins,” Oppenheimer wrote, noting that “the post-financial-crisis cycle extended most of these trends.”

Supply-side reforms, having succeeded in increasing corporate profitability and shareholder wealth, but having failed miserably when it comes to fostering favorable outcomes for labor and the masses, are giving way rapidly to demand-side stimulus which, in turn, could be inflationary with consequences for bond yields and risk-free rates.

Globalization is under siege, not just from populist politics, but now from the pandemic and the attendant reshoring impetus.

And, finally, tax havens have worn out their welcome in a political environment defined by an aversion to spiraling inequality engendered by runaway corporate profits and capitalism run totally amok.

For me, the most interesting question going forward is how many of the would-be anti-globalists, Fed critics, populist finance bloggers and other persistent critics of the “existing order” will be truly happy in a scenario where making money in capital markets isn’t as easy as it’s been for the last several decades.

The majority of such crusaders — from the libertarian blogger crowd to the Progressive economists to the rare analyst willing to chance a contrarian take to the caustic hedge fund managers who deride the Fed on television while benefitting handsomely from monetary largesse — are rich. Certainly relative to the average American family and in many cases in an absolute sense.

To put it bluntly, most of them are united in having benefited for years from the very same conjuncture they so readily deride, even as their critiques of the system vary by ideological bent. Or, more aptly, by purported ideological bent.

Remember: Nobody is genuine. To quote Walter Donovan, “Didn’t I warn you not to trust anyone, Dr. Jones?”

What the Goldman chart suggests to me is that sharp drawdowns in markets are needed to set the table (so to speak) for the next leg up. By refusing to countenance such a drawdown post-GFC, the Fed and other CBs would seem to be guaranteeing the low-return environment many analysts are warning about.

Precisely and they cannot allow the sharp drawdown because the system is too fragile to handle them. As we saw in the GFC moves down result in losses far higher than the values of the original assets. We cannot raise rates until we make our systems more robust and we cannot do that save by policy choices which we refuse to make because keeping the fragility maximizes profits next quarter. We insist that we be hoisted by our own petards.

“As we saw in the GFC moves down result in losses far higher than the values of the original assets” — which is why Buffett called derivatives “financial weapons of mass destruction.”

Entering a fourth (decades long) super cycle.

Increasing automation, robotics, clean/abundant energy (fusion), screens, supercomputers, blockchain, etc. will all decrease the need for human workers. Manufacturing will be less dependent on China, as we replace human workers with automation. Human beings will be more interested in entertaining themselves than having a family. A decrease in human population will help with cleaning up the Earth.

This will be a stock picker’s playground.

The population reduction won’t go fast enough. The Earth, IMHO, is beyond redemption already. While we might actually slow down the climate “rot,” the problem has already exceeded the point of no return and even slower growth will only continue the problem at a slower rate. Decreasing the need for workers is not a solution to anything. People who don’t work don’t buy anything. Economic growth becomes permanently negative. It’s possible my grandson (now 12) could live out the current century, though frankly I don’t think there will be much to see at that point.

And people that don’t work generally suffer disproportionally from psychological ailments which lead to big social problems.

I agree. The last supercycle damaged the family unit and other aspects of our society. The list is long of what can be damaged in the next super cycle.

Capitalism can be brutal.