While only time will tell whether Monday’s selloff on Wall Street was just another blip on the radar screen or the beginning of something more sinister, there was some agreement on one thing: Mechanical selling and systematic flows contributed to the rout.

That risk was known. Things that used to be esoteric — “ostensible arcana” as I’ve playfully described modern market structure — are now going mainstream. The concept of a “window for movement” in and around options expiration is now thoroughly socialized, for example.

Given that, it likely came as no huge surprise that the new week kicked off with fireworks, especially considering mainland Chinese markets were on holiday, and China is the locus of macro concerns.

Key now is whether (and to what extent) the tumult engenders more systematic deleveraging, which in turn tips more dominoes.

Read more: If This, Then $137 Billion Of ‘Hard Mechanical Deleveraging’

Obviously, market participants will be keen to follow every incremental piece of news out of China. Traders want clues as to what lengths Beijing will go to in order to avert a disorderly outcome as Evergrande slides into the abyss. At the same time, further evidence of a meltdown in the property sector won’t be greeted warmly by nervous investors.

But one immediate concern is whether there will be aftershocks from Monday’s tumultuous session. There may be. But even if there are, they won’t happen in a vacuum, and they could reverse later depending on how things develop.

Despite the readily observable mainstreaming of esoteric dynamics, it still feels like too many market participants haven’t fully internalized the fact that depending on the circumstances, it’s not some kind of “cop out” to write off a bout of selling as technical in nature.

Market participants are predisposed to interpreting analysis of systematic flows as somehow inherently bearish. That’s not an accurate appraisal. For example, vol control deleveraging took the blame for some of Monday’s losses, but as Nomura’s Charlie McElligott has emphasized over and over again, the subdued character of daily moves over the past few months served to tamp down realized vol, which in turn dictated an ongoing, “background” bid from the same investor cohort which may have been deleveraging on Monday.

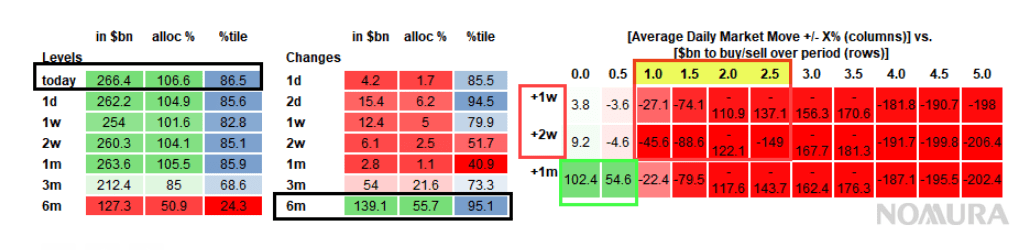

“We estimate that Vol Control added exposure last week [of] +$12.4 billion,” he said, noting that represented an 80th%ile one-week add and brought total exposure to $266.4 billion, in the 87th%ile (tables below, from Charlie).

Indeed, the whole concept of “stability breeding instability” hinges on the idea of a long period during which these flows help suppress volatility, keep trending markets trending and thereby lead to still more accumulated exposure and still lower volatility, until the proverbial “skier’s scream” starts an avalanche.

In the meantime (i.e., as the snow cover builds up), markets grind higher and higher, sometimes accompanied by the almost complete extinction of realized vol. That’s what we’ve seen for months, although lately, the calm was more eerie than usual due to extreme readings on various “crash” metrics, which made for a rather terrifying juxtaposition with the near complete absence of daily movement in spot.

Going forward, if markets calm down, vol sellers reengage and spot gets back to being a semblance of well-behaved, the resumption of small daily moves “would see Vol Control as a very large potential exposure add / buyer projecting out over the forward one-month period,” McElligott reiterated on Monday (see the table on the right, above).

I mention all of this not to trivialize Monday’s dramatics, but rather to remind folks that these flows can be bullish or bearish. And, yes, sometimes you can simply write the situation off.

In a note dated Monday, JPMorgan’s strategy team, led by Marko Kolanovic, called the selling technical and said the pullback “represents a buying opportunity.”

“The market selloff that escalated overnight we believe is primarily driven by technical selling flows (CTAs and option hedgers) in an environment of poor liquidity, and overreaction of discretionary traders to perceived risks,” the bank wrote, adding that “our fundamental thesis remains unchanged, and we see the selloff as an opportunity to buy the dip.”

It’s easy to make snide remarks, but the same snide remarks were pervasive in January of 2019 too, and on countless other occasions when market participants failed to appreciate that systematic flows and the various dynamics that make for great headlines during selloffs also contribute to markets that end up trending inexorably higher.

Again, the point isn’t to trivialize the pullback, and it’s certainly not to suggest that some miscalculation in Beijing couldn’t take us down dark roads. Rather, I just wanted to casually mention that sometimes, it is “just” technical selling flows.

We’ll see what happens.

You must be logged in to post a comment.