One of this month’s market obsessions is an apparent disconnect between economic momentum and positioning in equities.

This is showing up in, for example, BofA’s Global Fund Manager survey, where growth expectations have plunged against equity allocations that remain stubbornly high. Goldman noted a widening disparity between multi-asset funds’ equity allocation and investors’ short-term expectations. And so on.

Over the summer, the “peak growth” narrative gathered momentum as the world’s two largest economies lost it (momentum, I mean).

Narratives have a way of becoming self-fulfilling. If you hear “peak growth” enough, you might rotate away from reopening names and reflation expressions. If enough people do the same, the rotation becomes a story in itself, which is then cited as “evidence” in support of the original narrative.

To be clear (and yes, I use that phrase all the time), I’m not suggesting the peak growth story (or, more broadly, the “Triple Peaks” thesis) has no merit. It does. And I’m not saying that economic momentum hasn’t waned. It has. Or that the Delta variant hasn’t played a role in stymieing activity. Again, it has.

Rather, I’m merely saying that when it comes to markets, narratives can become self-perpetuating, especially when the price action is exacerbated by positioning unwinds (e.g., the bond rally that saw 10-year US yields dive more than 60bps from YTD highs), which in turn make the optics even worse.

One thing that makes the current conjuncture unique is that paradoxically, waning economic momentum is compatible with stretched positioning in equities and record highs on the benchmarks. There are several explanations for this phenomenon, not least of which are i) the perception that weaker economies mean prolonged monetary support, and thereby a prolongation of the “TINA” environment and abundant liquidity, and ii) the fact that many pandemic beneficiaries and secular growth favorites dominate benchmark equity indices.

The market is pricing a slowdown. It’s just that a tilt back in favor of tech and secular growth shares (as recovery concerns mount) can create the perception that stocks are oblivious. Earlier this year, many suggested the “broad” market might not be capable of making new highs if the tech titans fell out of favor as the recovery rolled along. What we’re seeing now is the opposite of that.

So, if you look under the surface or look at bond yields or just divide small-caps by the S&P (figure below), it’s fairly obvious that stocks are, in fact, aware of the slowdown story.

That simple chart is just one example. There are countless other visuals you could conjure.

It’s with all of that in mind that JPMorgan’s Dubravko Lakos-Bujas said Wednesday that the bank “doesn’t expect permanent demand destruction from the fourth COVID wave, but rather a delay in the global reopening and economic normalization.”

The bank acknowledged that “the rise in the Delta variant combined with government stimulus rolling off has coincided with a business cycle slowdown, delayed labor market recovery and lower consumer sentiment,” but said those suggesting this is all evidence of a truncated cycle entering its latter stages may be mistaken.

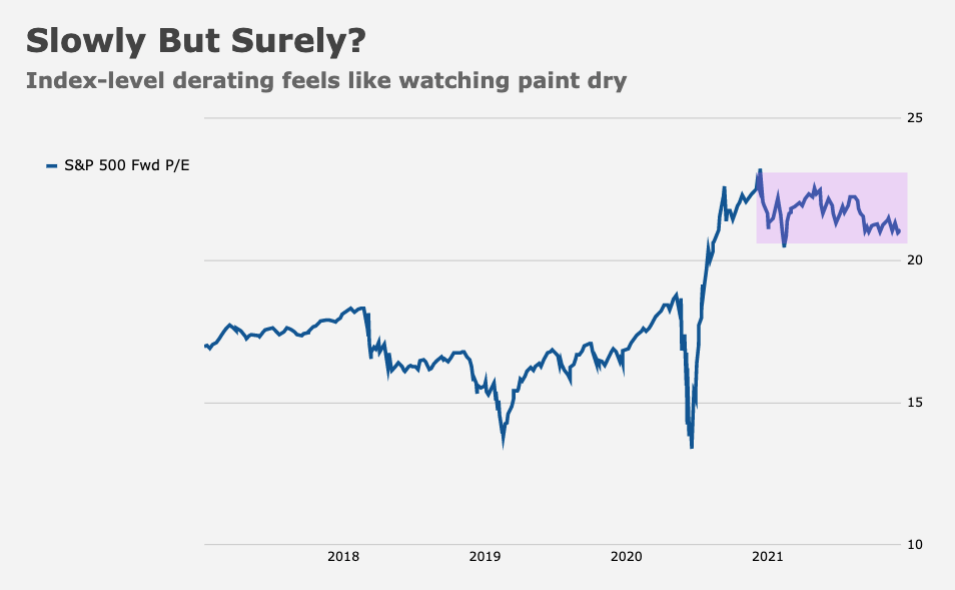

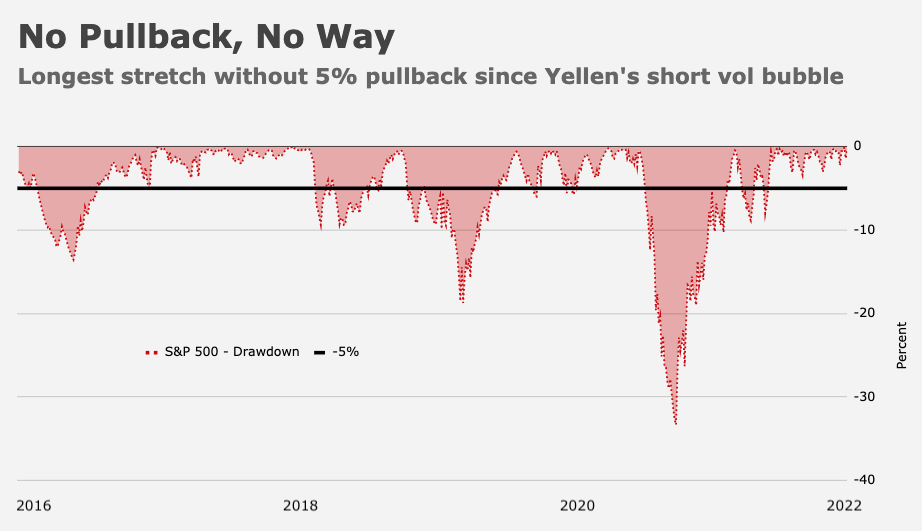

Consistent with the point made above about the market pricing in a slowdown despite stretched equity positioning, the lack of a material derating at the index level and, relatedly, the conspicuous absence of a 5% pullback, Lakos-Bujas noted that risks to growth are not only “well-flagged” but actually “overdone in some cases.”

For example, a JPMorgan COVID recovery basket has reversed its YTD outperformance, taking multiples back to post-pandemic lows (figure below, from JPMorgan).

Reiterating the bank’s constructive outlook, Lakos-Bujas said he “remain[s] confident that strong growth lies ahead and activity is bound to re-accelerate.”

You’re reminded that the bank raised its year-end S&P target back in July to 4,600. On Wednesday, they raised it again, alongside EPS estimates.

Lakos-Bujas called consensus estimates “too conservative… largely due to ongoing COVID fears and related inventory shortages.” In the bank’s view, those jitters will abate with the Delta wave “leading to a much stronger holiday season and a pick-up in cross-border activity from still depressed levels.”

The full note goes into considerable detail, but the bottom line (figuratively and literally) is that Lakos-Bujas lifted the bank’s EPS estimate to $210 from $205 for this year, $9 above consensus. At $240, the bank’s 2022 EPS forecast is now $20 above consensus.

JPMorgan’s new year-end S&P target is 4,700.

Notably, the bank’s Michael Feroli downgraded his estimate for US growth for Q3 to 5% from 7% on Wednesday. “Delta is weighing on consumer service spending, while sparse auto dealer lots are one important factor holding back consumer goods spending,” Feroli remarked.

{kind=link}

{kind=link}

You must be logged in to post a comment.