The disconnect between investors’ positioning in stocks and their outlook for the economy is growing.

That was the main takeaway from the September vintage of BofA’s Global Fund Manager survey.

Global growth expectations have plummeted from 75% in June to just 13% this month, likely reflecting data disappointments (relative to consensus anyway) in the US, slowing growth in China and the “peak growth” echo chamber.

The net 13% read from the poll was the lowest since April of last year, and represented an about face from March’s 91% reading.

And yet, the bank’s Michael Hartnett noted that a gauge of risk-taking suggests “investors are ignoring the macro.” A net 9% said they’re taking higher than normal risks. That’s lower than the 25% high in February, but consider that the two-decade average is -15% (that’s negative 15%).

Similarly, equity allocations remain generally overweight. The juxtaposition is illustrated in the figure (below, from the survey).

“Historically, growth expectations have led FMS investor equity allocation, but equity allocation has lagged this cycle,” Hartnett went on to say.

I assume most readers can venture a guess as to why that might be.

In all likelihood, the persistence of monetary accommodation and the accompanying “TINA” dynamic means investors have no choice but to keep buying stocks.

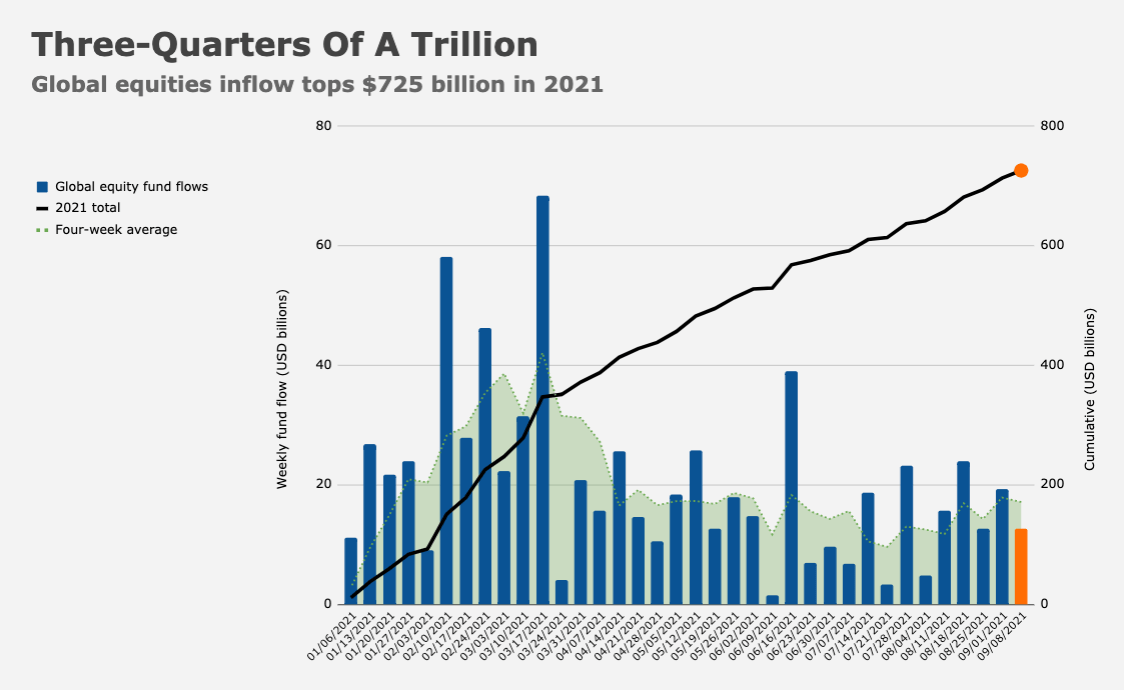

Global equity funds took in another $12.7 billion during the latest weekly reporting period, taking the YTD haul to an astounding $725 billion (figure below).

That, in turn, perpetuates “FOMO” (that other ubiquitous acronym), thus luring still more money into stocks.

Still, the connection between equity flows and the macro isn’t totally lost. “Cumulative inflows into global equity funds have been large YTD and have more than made up for the outflows since 2018,” Goldman’s Christian Mueller-Glissmann said, before noting that even so, “higher frequency data show that fund flow momentum peaked in Q2 [and] inflows have decelerated on a six-month basis in line with softening activity data as captured by the ISM.” The figures (below, from Goldman) illustrate the point.

Writing Tuesday, BofA’s Hartnett went on to say that in addition to plunging growth expectations, FMS investors’ outlook for rising profits fell, while net inflation expectations turned negative for the first time since May of 2020.

“All that said, just 6% of respondents expect recession,” Hartnett added.

My guess is this partly reflects investors’ expectations for seasonality.

In regard to the inflation topic, if infrastructure and the budget reconciliation process go as planned, it may well inspire additional uncertainty about inflation.

Fingers crossed, more impactful levels of inflation will not actually be realized in 2022. Recalling yesterday’s post (Failings and an Ungovernable Nation) as the Fed tap-dances with risk and the economy (hopefully) provides more hearty meat to sustain our people.

Any update on the BofA Bull/Bear indicator?

Basically “Neutral.” 5.8.