I suppose we’re witnessing a “selloff.” Maybe folks are front-running the pullback window.

The reason for the scare quotes around “selloff” should be obvious. Although US equities logged a sixth daily loss in seven sessions, record highs on the benchmarks are still within spitting distance. Barring something totally unforeseen, that’ll likely remain the case.

The acronyms (“TINA” and “FOMO”) have quite a bit of explanatory power, despite being unpalatably meme-ish. Virtually no one seems willing to countenance an overtly bearish view. Maybe that’s the biggest red flag of them all.

There’s a disconnect between equity allocations and macro expectations. The former are elevated, the latter are rolling over.

Read more: Stock Investors Are ‘Ignoring The Macro’

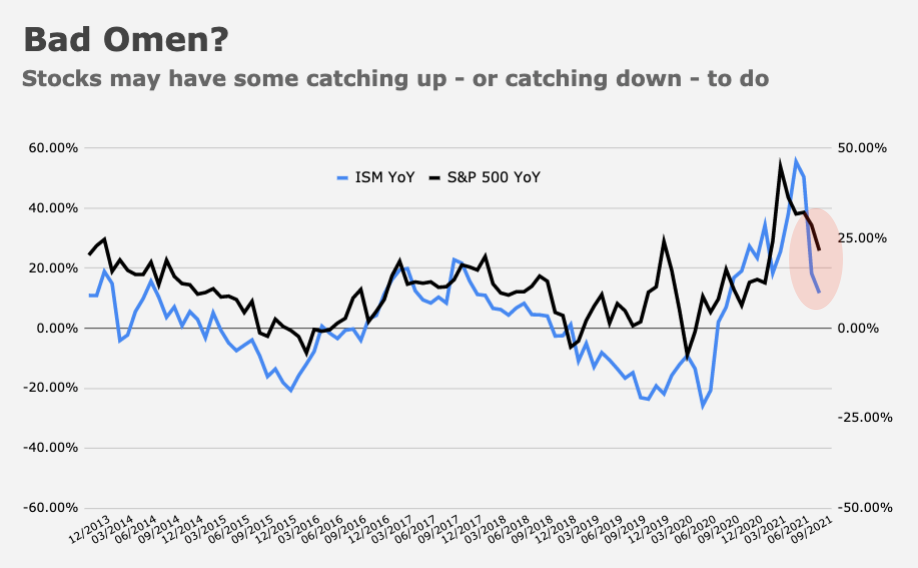

And it’s not just one survey (i.e., BofA’s monthly fund manager poll) where the disparity is showing up. Macro surprises have turned negative, likely presaging a downturn in earnings revisions. ISM is disconnected from the S&P on at least one tortured chart. And so on, and so forth.

While sorting through today’s digital pile, I ran across another such disconnect that’s pretty glaring. In a note dated September 13, Goldman said that around half of the multi-asset funds the bank tracks have an equity allocation in the top 10th%ile versus their own history. That looks very anomalous on a chart (left figure, below).

Meanwhile, the right figure (above) shows multi-asset funds’ equity allocation completely decoupling from investors’ short-term expectations.

Commenting, the bank’s Christian Mueller-Glissmann wrote that this “suggests there might be limited room for further re-risking from here.”

And yet, he added the obligatory caveat: “Should the activity data continue to reset gradually, we think TINA will mean multi-asset investors are likely to maintain their overweight allocations to equities.”

There it is again. Absent a severe slowdown not amenable to the “bad news is good news” spin, equities are simply the only game in town.

But there was nuance. Although Goldman’s research showed that, adjusted for AUM, multi-asset funds are running large equity allocations, the increase for US-based funds is entirely down to strong returns. In fact, Mueller-Glissmann observed that on net, equity demand from US-based funds is negative on a rolling 12-month basis.

Meanwhile, Goldman said the systematic crowd has likely increased their equity exposure over the summer, hardly a groundbreaking observation given the grind lower in realized vol. On the bank’s model, a simple risk parity strategy has an equity allocation of around 36%, consistent with levels seen during historical low volatility regimes.

“Similarly, with low volatility and strong equity performance, other systematic strategies such as CTAs have likely increased their equity exposure,” Mueller-Glissmann went on to write, on the way to cautioning that “the combination of high vol of vol and elevated macroeconomic uncertainty might be challenging for a sustained low vol regime [and] higher volatility might drive de-risking from these investors.”

That’s a kind of polite, less technical way of nodding to some of the dynamics detailed over the past several weeks (and months) by Nomura’s Charlie McElligott, who on Tuesday reiterated that “we STILL have the same broken vol market standoff, where metrics like skew, iVol vs rVol and term-structure continue pricing ‘crash,’ but juxtaposed against SPX 10-day realized vol cratering back to a five-handle.”

This isn’t lost on Goldman. “Investors have been discounting elevated left tail risk with equity protection very expensive [and] despite the recent low realized volatility, volatility risk premia have been close to the post-2000s highs with steep vol term structures,” the bank went on to say, in the same note cited above.

There are layers of irony vis-à-vis vol control. On one hand, the three-month realized window is set to lose some “down days,” which opens the door to more exposure adds. But, as Goldman alluded to (and as Charlie has been pounding the table on nearly every day), the problem is that the exposure add for vol control over six months already ranks near the 93rd%ile on Nomura’s model.

Very low realized vol suggests heightened sensitivity, making even a modest down day potentially perilous considering loaded positioning.

Or, as McElligott put it, “the potent mix of the recent rage allocation and extraordinarily low rVol means a one-day ‘outlier’ move even in the -1.5% / -2.0% area risks very substantial de-allocation from Vol Control over the next 1-2 weeks, per our estimates.”

{kind=link}

I am curious to see what happens to the market post- option expirations this week. A blip or a new trend?

Buying stocks right now, to me, feels like picking up pennies in front of a steamroller. The daily up-moves are tiny. Only a relatively few names have decent performance. The market is highly concentrated in just those few names. The usual suspects Google Apple etc. All of those have big buybacks.

So there’s at least one big buyer there that, both has access to huge capital, can issue bonds at any time at a near zero interest rate, has strong cash flows, and is not at all price sensitive. They will keep buying a certain number of billions per month, even if stock is priced at 2x or 3x or 10x it’s long-term multiple. It doesn’t matter. These buyers are not price sensitive. In a certain sense, the entire market is front running those big buybacks.

TINA is right. This is not a healthy market. This market has been engineered by the Fed, not unlike what’s happening in Japan over the last 20 years.

Everything is rosey until it’s not. The Fed could announce a change of policy, anytime.

If the Fed really intends to support markets indefinitely, they should make it official. Otherwise, they risk burning people seriously, when the Fed does finally change policy.

“The Fed could announce a change of policy, anytime.” That plus new taxes are the two biggest political risks facing us at this time, IMHO. The Fed may not want to make a change but they may have no choice, sooner rather than later.

New taxes are a risk? corporations may pay an extra few percentages and maybe are forced to pay above zero? From what I have seen and read, I won’t be affected by any of the proposals.