US consumer prices rose less than expected in August, bolstering the Fed’s “transitory” narrative and likely cementing the case against a taper unveil at the September FOMC meeting.

Core prices rose just 0.1% MoM, the BLS said Tuesday. That was far less than the 0.3% economists forecast (figure below).

The headline gauge rose 0.3% from July, also cooler than anticipated.

The monthly rise on the core gauge was the smallest since February. Indexes for household operations and shelter, new vehicles, recreation and medical care rose in August, while indexes for airline fares, used cars and trucks and car insurance all fell.

“The relevance of the core inflation figures not only has implications for the durability of the reflation trade, but it carries with it the ramifications for the Fed’s ability to retain policy flexibility without an implicit referendum on its new framework,” BMO’s Ian Lyngen and Ben Jeffery said Tuesday.

At 5.3%, the headline YoY print was inline with estimates. Core prices rose 4% YoY, less than the 4.2% consensus expected (figure below).

It does appear that inflation peaked over the summer, although that assessment comes with all the usual caveats. Indexes for gas, food and shelter all rose in August.

On Monday, the latest edition of the New York Fed’s consumer survey showed medium-term expectations accelerating to a series high.

The monthly increase in the government’s food at home gauge was smaller than July’s rise. The same was true of the food away from home index.

Still, the monthly gain on the broad gauge was the ninth straight (figure above).

User vehicle prices fell for the first time since February. Transportation services costs dropped 2.3%, the second consecutive large monthly decline.

The shelter index rose 0.2%. Owners’ equivalent rent posted a 0.3% gain from July. The familiar figure (below) continues to suggest that the surge in home prices will eventually work its way through, so to speak.

New home prices continue to hit records, while annual gains are the largest in data going back three decades (grey line in the figure above).

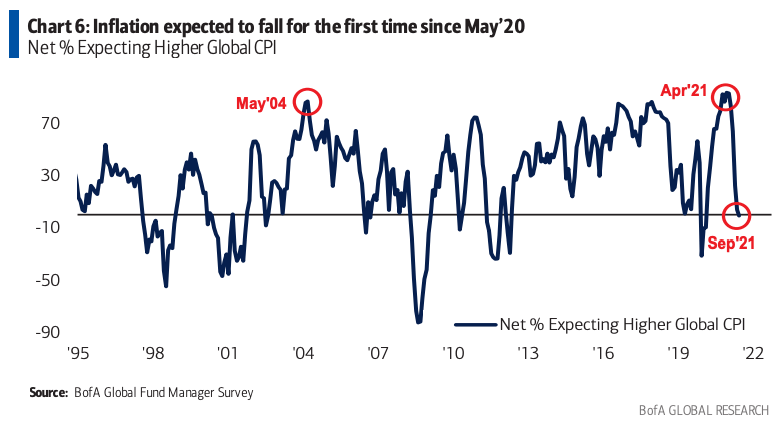

Tuesday’s data came as the latest edition of BofA’s closely-watched Global Fund Manager survey showed inflation expectations falling to a net -1% (figure below, from the poll).

As the bank’s Michael Hartnett wrote, it was the first time since May of last year that a net of participants expected inflation to fall.

“Overall, it… reinforce[s] the Fed’s transitory characterization,” BMO’s Lyngen said, shortly after Tuesday’s CPI data was released.

In the BofA poll, 69% of respondents said inflation is transitory. Just 28% said it’s permanent.

My take on inflation, is to look back to Q2 2020 and review the decimated GDP price deflator stuff, which collapsed from Covid-19 shock. That really, really wasn’t that long ago and the nonlinear explosion of economic shocks (up & down) are not really (fully) digested yet — so I’m 100% in the transitory mindset, versus the short-term nervous nelly panic mindset.