It’s “crunch time” for Morgan Stanley’s mid-cycle transition thesis, the bank’s Andrew Sheets said Tuesday.

Sheets’s colleague Mike Wilson pivoted away from early-cycle trades months ago in anticipation of a “period when markets contemplate the peak rate of change in growth and policy.”

Although he recently marked his profit forecasts to market to account for blockbuster Q2 earnings, Wilson expects the index to derate eventually, a contention that’s allowed him to stick with a less ebullient S&P target than many of his peers.

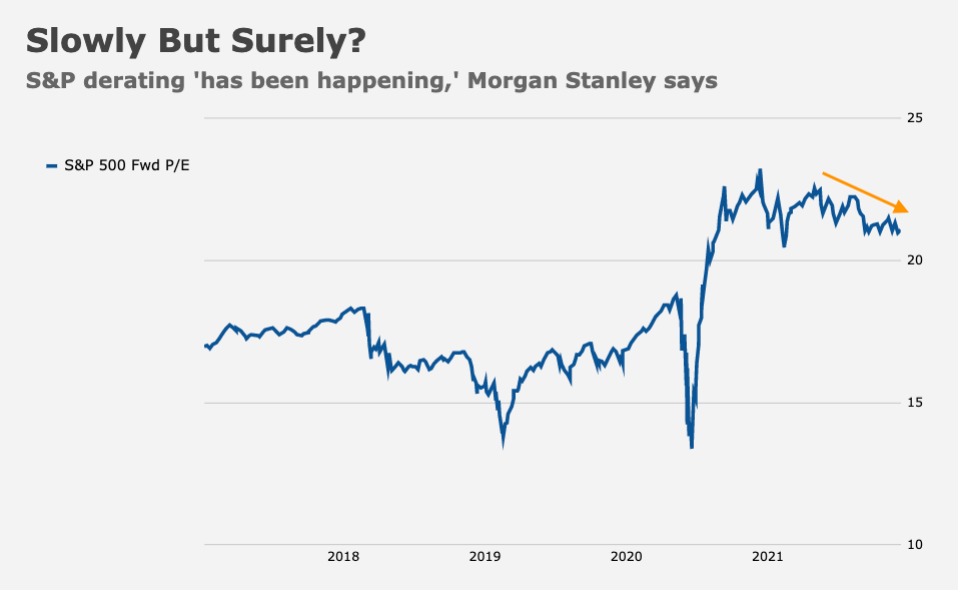

Some of the froth came out of the bubbliest corners of the market earlier this year, but the broader market generally refused to sell off, ironically because it’s not very “broad.” Simply put, a serious index-level derating hasn’t played out (figure above), even as multiples drifted a bit lower through mid-August.

In a Tuesday note, Sheets called the next two months critical. “We continue to think this is a ‘normal’ cycle, just hotter and faster, and our cycle model remains in ‘expansion,'” he said, referencing a July note in which he reminded market participants that “‘normal’ is a funny concept.”

Sheets continued. “The next two months carry an outsized risk to growth, policy and the legislative agenda,” he said, describing the “straightforward dilemma” as follows:

If global growth remains resilient, the US infrastructure bill passes and COVID-19 cases see a near-term peak (our base case), US yields need to adjust higher. That is especially challenging for more expensive ‘growth’ parts of the market, which are trading with a positive correlation to bond prices. Alternatively, if the economy does slow, many risk premiums look too low versus prior growth scares.

The bank recently slashed their tracking estimate for Q3 US growth to just 2.9% from 6.5%. Goldman, meanwhile, cut their own outlook for the US economy in 2021 this week, citing (among other things) a “harder path ahead” for the US consumer.

Although Morgan Stanley’s base case is that the cycle (and the attendant bull market) “have further to go,” getting through September and October could be a challenge.

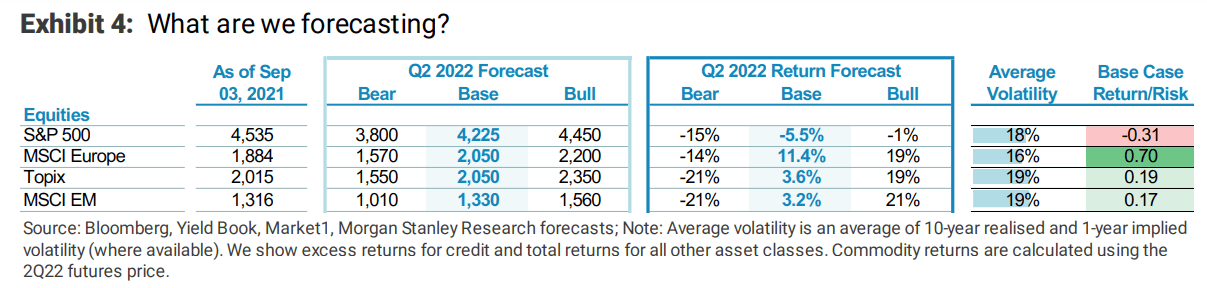

Sheets cited the bank’s cross-asset framework, which identifies (or tries to anyway) the most attractive risk-adjusted returns. That framework suggests the risk/reward for US equities is poor. The figure (below, from Morgan) is truncated — it only shows equities. The full table has FX, rates, credit and commodities.

Ultimately, Morgan sees returns for US equities (and credit and Treasurys) as poor versus cash. As such, Sheets downgraded US stocks to Underweight (and global equities to Equal Weight).

“With poor risk-adjusted returns elsewhere, cash, by definition, is more attractive to hold,” he said, “especially given the specific, time-sensitive nature of events over the next two months.”

I can already hear the catcalls. “Cash?! Who wants to hold cash?! Ray Dalio says it’s ‘trash.'” And Bill Gross (who, as it turns out, is still writing), derided cash last week, although he saved his harshest criticism for the asset class over which he once reigned.

Sheets is aware that the bank’s Overweight cash recommendation is likely to be met with jeers. “We expect an understandable level of eye-rolling,” he said Tuesday, before exclaiming that “cash returns, after all, are terrible!”

Does that not mean investors should “buy something, anything else?”, he asked, rhetorically.

The answer is maybe. But only if you know where to look. Although risk-adjusted returns are attractive versus cash in European and Japanese shares (and also in some stuff regular folks can’t trade), they aren’t in the US.

Specifically, Morgan’s strategists expect “cash to outperform US equities, government bonds and credit over the next 12 months,” Sheets said, adding that “our own top-down estimates agree on the last two.”

You must be logged in to post a comment.