A dramatically bad US jobs report barely moved the needle for US equities, which managed another weekly gain despite evidence of a sharp deceleration in hiring.

You could (very plausibly) argue that, in fact, stocks held up because of that sharp deceleration. After all, the rapidity of stimulus unwind depends on the evolution of the labor market, and particularly the hard-hit leisure and hospitality sector, where jobs growth flatlined in August.

In food services, 42,000 jobs were lost last month (figure below). It was the first decline since the winter COVID wave.

Opinions vary on what August’s disappointing jobs report means for the taper timeline, and it was difficult to get a good survey of views given the proximity of the holiday weekend.

While the Fed will doubtlessly take note of the hotter-than-expected read on wage growth (for example, the figure below suggests wages in leisure and hospitality are running at the briskest 12-month pace ever), it’s almost impossible to imagine a taper unveil later this month.

If the Fed committed to trimming asset purchases starting in October only to see September’s jobs report come in soft, the Committee would be in bind — they’d be tightening into a nascent slowdown, a fate to which they’re already doomed anyway, just not necessarily with respect to the labor market.

Worse, the November meeting comes prior to the release of October’s jobs report, putting Jerome Powell in a very awkward position were the Fed to start the taper next month. He’d need to explain, at the November press conference, why a Committee ostensibly more committed than ever to the jobs side of its mandate, started tightening just as the labor market rolled over. Whatever explanation he managed to conjure would then be juxtaposed with October payrolls less than 48 hours later. Powell hasn’t been the luckiest of Fed chairs, so it would hardly be surprising if the data made a fool of him.

“We don’t think the jobs report [was] weak enough for Fed officials to back away from their ‘this year’ tapering signal, especially given the continued strength in wages, but we believe it increases the probability of a formal announcement coming at the December rather than the November meeting,” TD’s Jim O’Sullivan said, adding that “we certainly don’t expect an announcement at this month’s meeting.”

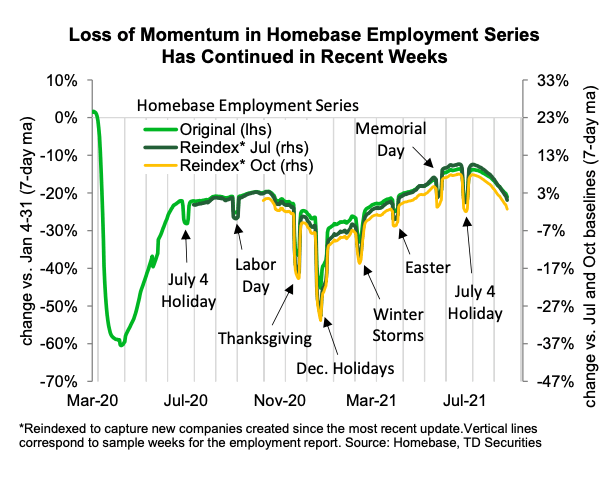

No, “certainly” not. Note the deceleration in “real-time” employment illustrated in the figure (above, from TD annotating Homebase’s data).

At the same time, stagflation murmurs are getting louder. Friday’s services sector PMIs didn’t help in that regard.

“[The] global macro is unambiguously stagflationary,” BofA’s Michael Hartnett remarked.

But, for now, markets are betting that any “pause” in growth during the second half will pass, as the Delta wave recedes, Hartnett went on to say, before noting that in addition to the assumption that the variant doesn’t permanently impair the recovery, traders and investors are betting that “poor macro = no taper = age of infinite central bank liquidity to continue despite [the] inflation surge.”

{kind=link}

The FOMC is headed into a horrendous whipsaw. The good news is it won’t kill them to wait until December to make an announcement. If they announce a “friendly” taper the market should be fine.

The main trouble with FOMC and QE policy, is that it’s mighty hard to raise rates while still buying stuff. The concept of tapering is like going on a diet while buying a few dozen donuts. If anything, the policy of jawboning is a way to buy as much time as can be bought, but at this point there’s structural systemic damage that basically is unfixable.