One way or another, a 10% correction is probably in the cards for US equities.

That’s one takeaway from the latest by Morgan Stanley’s Mike Wilson, who still enjoys some residual credibility when it comes to calling pullbacks thanks to his prescient prediction of a “proper rainstorm” just prior the mini-bear market that unfolded in late 2018, following Jerome Powell’s “long way from neutral” communications faux pas.

I probably identify Wilson with that episode too often — as if he’s never said anything else worth mentioning. In fact, he’s been (generally) correct on a number of occasions since. For the most part, he’s been on the right side the post-pandemic rally.

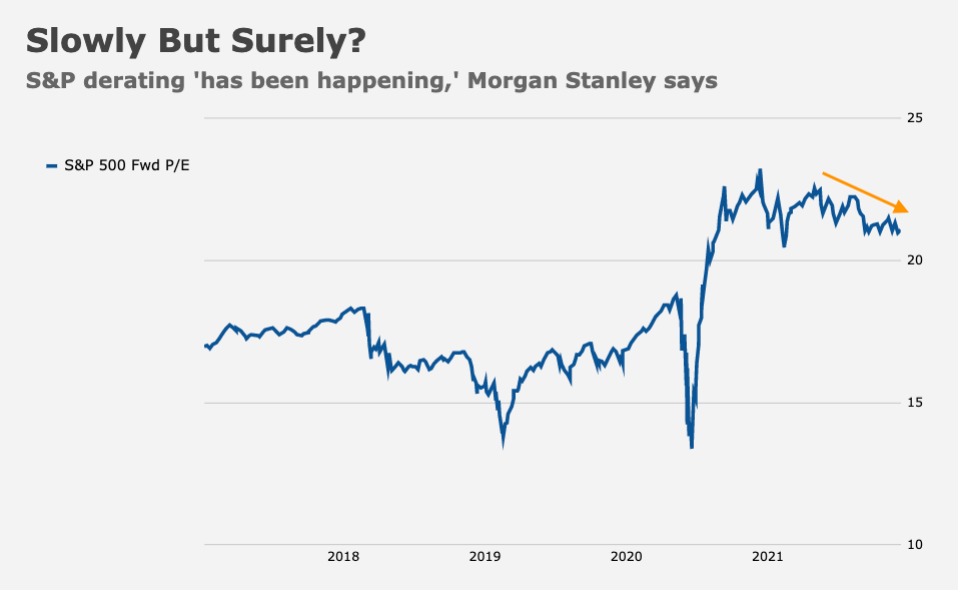

More recently, though, Wilson’s relatively bearish outlook for US equities is at risk as benchmarks simply refuse to correct (figure below). I’d add the customary disclaimer: Almost no one is properly “bearish” right now. It’s all extremely relative.

A couple of weeks back, Wilson’s profit outlook was “marked to market” (his words). In the simplest terms, Q2’s blockbuster results necessitated “adjustments,” but not necessarily to price targets, which he largely maintained simply by projecting lower multiples, consistent with the bank’s “mid-cycle derating” call, a fixture of Wilson’s outlook for US equities.

Fast forward to this week, and the S&P was poised to notch a 12th all-time high — in August alone. There’s plenty to worry about. But, as noted in “Remind Me About The Risks Again,” this is a market with a multitude of plunge protection failsafes, from $4.5 trillion in sideline cash to buybacks to the fact that, even if the Fed started tapering asset purchases by $20 billion in October and did so each month (as opposed to each meeting), they’d still be buying bonds in February. And there’s almost no chance of that timeline materializing, by the way. That’s simply the most hawkish taper schedule that’s not completely far-fetched.

Wilson alluded to the difficulty inherent in keeping up with a benchmark that never sells off without correctly anticipating the narrative shifts. “With the S&P 500 up another 20%+ so far this year, many active managers are finding it more difficult to keep up, as the market leadership has bounced around more than normal,” he wrote, adding that while “many of the internal rotations we expected during the mid-cycle transition have played out,” the usual 10% drawdown has been averted thanks to stubbornly high valuations at the benchmark level (figure below).

For Wilson, the correction “has simply been deferred as excess liquidity and retail and international inflows have kept the major US indices elevated.”

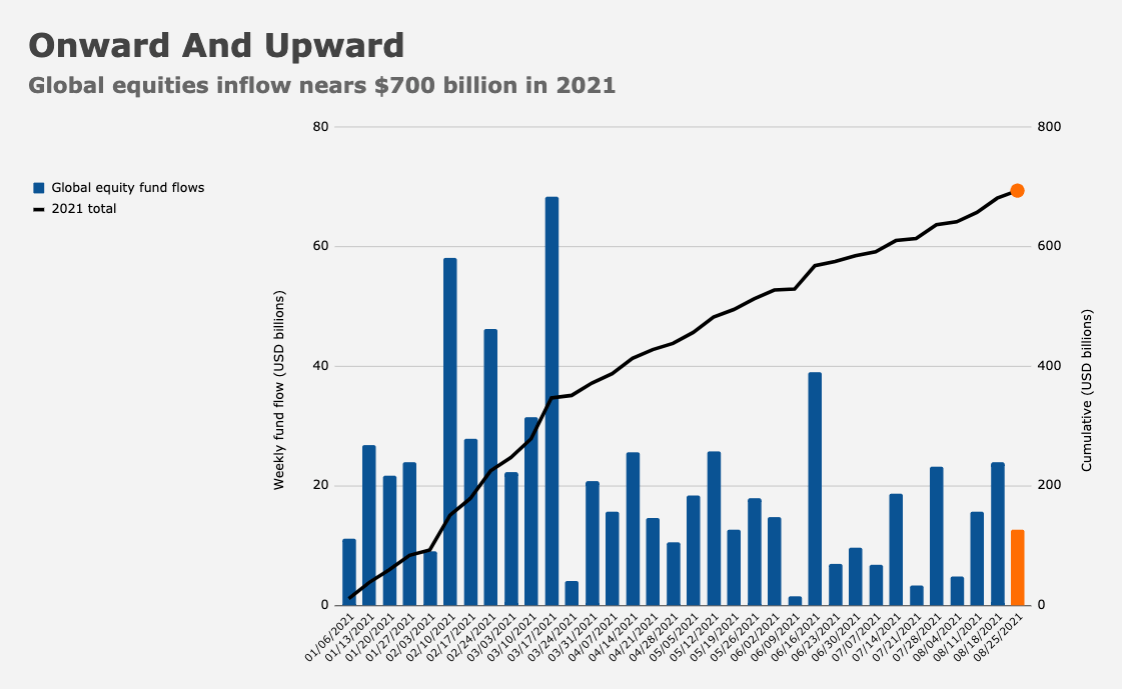

Indeed. One of the “failsafes” mentioned above is consistent inflows for equity funds. And by “consistent” I mean uninterrupted. Regular readers are tired of hearing this, but there hasn’t been a single week of outflows in 2021 (figure below).

Of course, there’s all kinds of nuance to be had by breaking down the flows into sectors and styles, but in terms of aggregate inflows, the total is approaching $700 billion.

In any event, there are two paths to a 10% correction, Wilson said Monday. One is “ice,” the other “fire.”

You can probably anticipate the arguments. Of the “fire” scenario, Wilson wrote that “we could see a continued strong economy and inflation drive the Fed to tighten policy, which would lead to higher interest rates and lower equity valuations.” In that case, “you want to own cyclicals and avoid expensive long-duration growth stocks.”

As for the “ice,” Wilson said “payback in demand and weakening consumer confidence [could] lead to a materially softer growth outcome than the consensus currently expects.” In that case, you’d prefer to own defensives. I talked a bit last week about the “payback” argument.

Wilson tempered his warnings. The “fire” scenario is relatively benign, characterized by a 10% drawdown as the benchmark finally derates to 19X.

Of the “ice” environment, he emphasized that “we aren’t looking for a recession or end of the cycle.” Rather, he cited the spread between University of Michigan sentiment and the Conference Board’s gauge (mentioned here) and noted that “it could be foreshadowing a much worse slowdown/payback than what most are expecting.”

You must be logged in to post a comment.