The standard, boilerplate copy on days when weakness across equities reverses during the cash session typically revolves around some version of this story: “Stocks trimmed losses as investors weighed robust earnings and ample stimulus against growth headwinds, geopolitical concerns and the threat of new lockdowns.”

That’s not an actual quote. But it could be. It would be right at home at the top of any standard market wrap.

The best part is, if you just reverse the order, it’s equally applicable to days when stocks rose early only to give back gains into the afternoon. So, this: “Stocks surrendered gains as investors weighed growth headwinds, geopolitical concerns and the threat of new lockdowns against robust earnings and ample stimulus.”

With apologies to whomever they’re due, if you’re a journalist for a mainstream financial media outlet, that’s your job. You write the same article every day, only with the words rearranged (God bless you). I couldn’t do it. The tedium would turn me into Jack Torrance within a week.

In addition to being tedious, those types of boilerplate assessments are very often wrong. Monday was a good example. I spilled a fair amount of digital ink last week (and over the weekend) documenting the flow dynamics keeping stocks pinned, and they were in full effect at the beginning of the new week, according to Nomura’s Charlie McElligott.

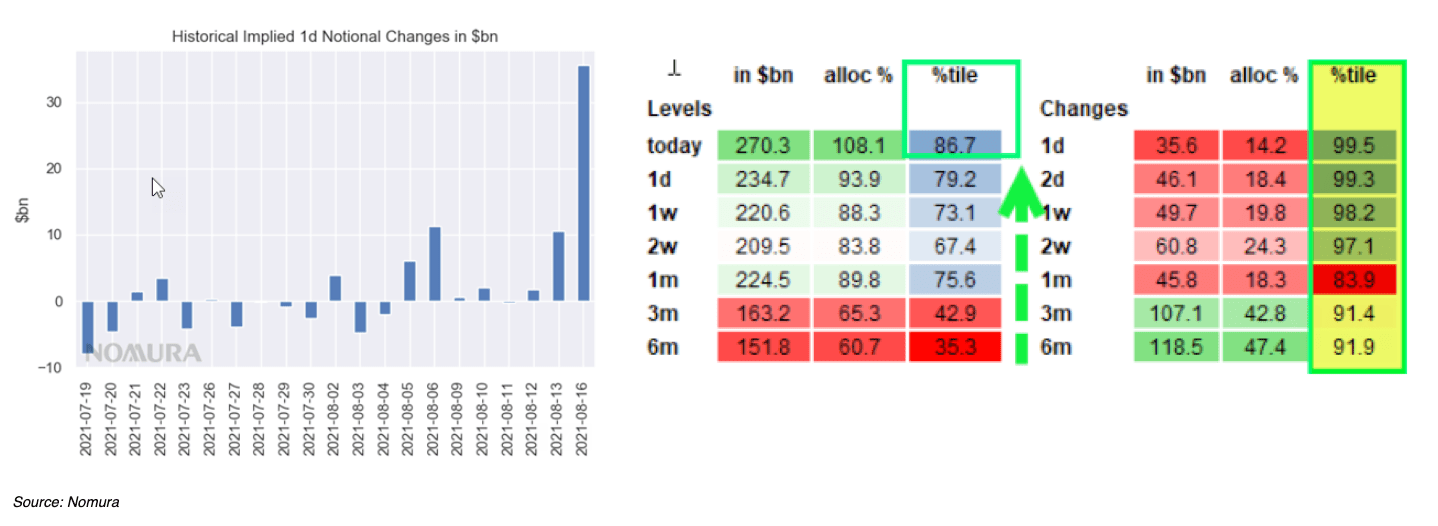

“In standard ‘tail wags the dog”’ fashion, two monster options-derived / vol-sensitive flows simply overwhelmed all macroeconomic and geopolitical narratives on the day,” he said, reiterating that dealers are “choking on prolific long ATM Gamma into Op-Ex,” creating a kind of automatic stabilizer, “crushing the daily distribution of outcomes into a narrow band.” This has been going on for a month (figure below), which in turn means realized vol has collapsed.

Realized vol compression dictates exposure adds from the vol control universe. “As of this morning, we see SPX five-day rVol = 0.9, last seen in September and October of 2017, while one-month rVol printed 8.3 / 3.5%ile rank and three-month realized registered 9.2 vols, a stunning 0.4%ile,” McElligott remarked, running through the numbers.

He also flagged eleven consecutive 30-minute green candles in S&P futs on Monday from 10 AM on (figure below, his annotations).

The automatic stabilizer dynamic (as I described it above), is attributable to two things currently. There’s the “Gamma Hammer” (as Charlie calls strangle selling) and a “pile on” from overwriters in index and single-name. The market’s “inability to move more than 20 to 50bps a day is totally unsurprising,” McElligott wrote. It’s also “excruciating for anybody bleeding Theta.”

The knock-on effect of the rangebound market and attendant collapse in realized vol is “‘outlier’ exposure adding in recent days / weeks / months,” from vol control, he went on to say, noting that on the bank’s vol control model, the overall allocation to equities now sits in the 87%ile. The one-day exposure change was estimated at $35.6 billion, a 99.5%ile event (figures below, from Nomura).

“So there you have it,” McElligott said, wrapping up his postmortem of Monday’s action before moving on to a lengthy discussion of supply/demand imbalances in the vol space and another sequencing exposition.

For our purposes (and coming full circle), the point is just that when you see what appear to be flow-driven reversals, you should probably trust your “if it quacks like a duck” instincts as opposed to some generic narrative about traders “weighing” various concerns throughout the day and gradually coming to a different conclusion than the one they reached just prior to the opening bell.

As Charlie put it Tuesday (describing Monday’s price action), it was “just massive ‘buy’ flows into [an] itsy-bitsy morning pullback, taking us right back in the peak ‘long gamma = rVol pinning’ strike zone, feeding [an] anticipated ‘melt-up-into-Op-Ex'” dynamic.

Read more:

‘Melt-Up, Crash Down, Crash Up’

Explaining The Calmest Market Since Yellen’s Short Vol Bubble

You must be logged in to post a comment.