I’ve used “mark to market” in tongue-in-cheek fashion on any number of occasions lately, mostly with regard to earnings and year-end targets for equity benchmarks.

There’s only so long you can hang on when stocks are running away from you and/or if today’s profits are such that your current projections for future profits begin to look unrealistically low. Goldman recently lifted their targets, in one such mark-to-market exercise.

On Monday, Morgan Stanley’s Mike Wilson raised some of his forecasts and estimates, in what he described as “marking to market on strong earnings.” He described Q2 reporting season as “exceptional,” an understatement to the extent “exceptional” can be an understatement (figure below).

Morgan raised their 2021 EPS estimate to $205 from $189, and 2022’s forecast to $209 from $200. The latter is below consensus, a shortfall Wilson noted is attributable to an assumed $9 headwind from higher taxes. Consensus doesn’t bake that in — yet, anyway. The change to this year’s outlook was “driven by a mark to market on exceptional first half results,” Wilson said.

This comes despite what Wilson previously identified as waning momentum for upward earnings revisions. He avoided any dramatic adjustments to the bank’s S&P targets by simply projecting lower multiples, consistent with the bank’s “mid-cycle derating” call, a fixture of Wilson’s outlook for US equities. “Offsetting higher earnings forecasts, we lower our multiple assumptions to 19x from 20x forward PE,” he wrote Monday, citing “greater evidence of our mid-cycle derating call playing out.” The table (below, from Morgan) shows mid-2022 targets. The bank’s year-end 2021 target is now 4,000. It was 3,900 previously.

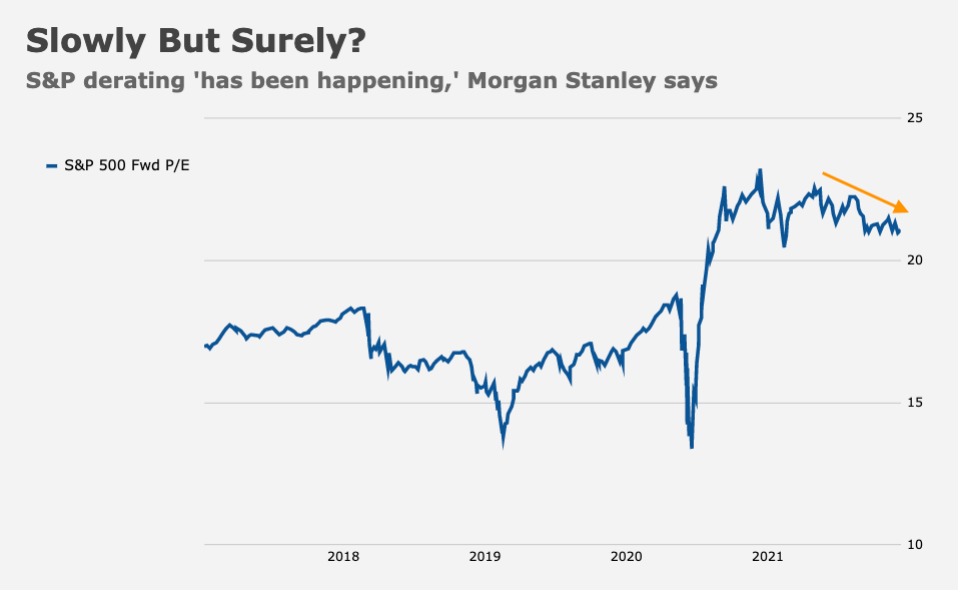

Multiples are contracting. It’s just a slow process. The high for the index’s forward multiple was 22.7X earlier this year. Wilson noted that the average for the first quarter was around 22X. That dropped to around 21.5X in the second quarter, and then fell a bit more during July and August.

Despite a bevy of steep corrections “under the surface” (so to speak), the index-level derating certainly hasn’t been any semblance of dramatic (figure below). But, if you squint and draw an orange arrow, you can make the case.

Morgan’s rationale is lengthy, although I wouldn’t call it laborious — that is, it’s worth a read. Ultimately, Wilson widens the band, so to speak. His bull case for mid-2022 was revised markedly higher to 4,800 from 4,450 (see the table, above). That assumes “strong top line and flow through and higher rates that are offset by equity risk premium overshooting to the low end of the post-GFC range.”

Wilson seems to think that’s unlikely, although he was polite about it. “We view this as a particularly optimistic set of assumptions,” he wrote, before noting that the bank’s June 2022 bear case is now 3,700, down from 3,800. That ensures the distribution “reflect[s] risks of growth shortfalls due to payback on demand and a looming fiscal cliff in Q122,” as well as a few other potential stumbling blocks.

Speaking of risks, JPMorgan’s Marko Kolanovic sees some for 2022, even as he remains constructive in the near- to medium-term. “We still believe there [may] be another leg lower in sectors that exhibited bubble-like behavior since the onset of the COVID-19 pandemic,” Kolanovic said, singling out renewable energy and EVs, crypto, hyper-growth and innovation stocks. Of course, those manifestations of “froth” slumped materially earlier this year, but Kolanovic thinks there may be “another leg lower” for them, even as they’re “not significant enough to destabilize the whole market.”

As far as the macro outlook and 2022 are concerned, Kolanovic “expect[s] an increase and amplification of geopolitical and political risks… related to various interdependent issues such as geopolitical relationships with China, Russia, Iran, issues around energy security, inflation, and US political developments.”

I should emphasize (again) that JPMorgan remains constructive. Kolanovic’s remarks on risks were an addendum to an otherwise upbeat note.

You must be logged in to post a comment.