Global equity funds took in just $4.8 billion over the latest weekly reporting period.

That’s notable for a few reasons. Most obviously, it marked yet another weekly inflow in an uninterrupted deluge that now sums to more than $640 billion for 2021 (figure below).

But it’s also notable for being the fourth-lowest weekly haul of the year. You might suggest that hints at risk aversion.

The breakdown did, in fact, betray a defensive bent. Tech enjoyed a sixth consecutive weekly inflow, for example, while emerging market equities suffered their biggest outflow in six weeks.

The latter could be short-lived, though. It was surely catalyzed (or at least exacerbated) by turmoil in Tencent. Prior to last week, the four-week moving average for EM equities flows had inflected for the better.

“EM [is] unambiguously where the secular value is,” BofA’s Michael Hartnett said, noting that EM bonds are now “the cheapest relative to US high yield in 20 years.” The figure (below) just shows the YTD underperformance for EM stocks.

If you pan out on that chart, you’ll discover that EM equities are actually sitting near a two-decade nadir relative to the S&P.

Coming quickly back to the notion that flows may have turned defensive, EPFR data showed nearly $25 billion going to cash over the reporting period ended August 4.

Apparently, at least some folks are concerned about a tough seasonal and liquidity vacuums, which can exacerbate swings and stoke volatility. EPFR described investors as “treading cautiously — if at all — in early August.”

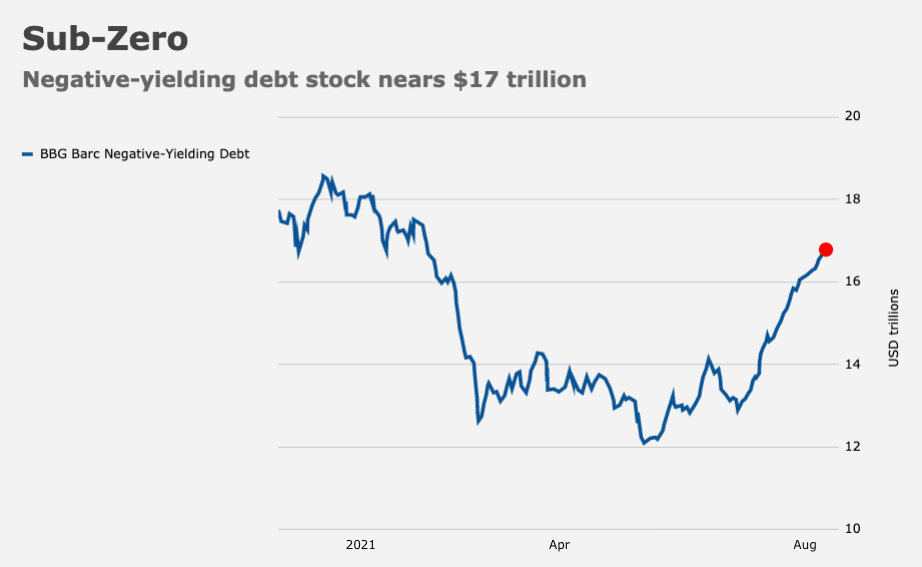

“What to make of a market where the response to fears of slowing global growth is a string of record highs in equity markets on both sides of the Atlantic?,” the report wondered, on the way to juxtaposing surging inflation in the US with nearly $17 trillion in global negative-yielding debt (figure below).

I suppose you’d be forgiven if you’re befuddled by what, on the surface anyway, are odd juxtapositions.

But, it does all make some measure of sense — in a nonsensical way. Investors are concerned about growth due to, among other things, Delta variant jitters, so there’s a bid for bonds. That bid, along with the bull flattening impulse, buoys secular growth shares, some of which dominate benchmark equity indices (e.g., the FAAMG cohort). Hence record highs on the S&P set against a fairly dramatic bond rally.

Meanwhile, central banks are determined to engineer a hunt for yield and push investors down the quality ladder and out the risk curve, so you buy stocks because… well, because acronyms, whether “TINA,” “FOMO” or something new the geniuses over on Reddit have come up with. Happily, stocks can serve as an inflation hedge.

As far as inflation itself, and whether it’s mispriced, the answer is “probably.” But it’s difficult to hedge that tail risk — this is risk management in a nonsense world after all.

Hmm. If I were a contrarian…

I’m not sure if EM means different things to different people and firms. But if China is included in the definition of EM (which strikes me as strange in that it is the second largest economy and growing faster than the largest economy), then isn’t much of the outflow story related to concern about the predictability of the regulatory environment in China? While Hartnett might be correct that there is value in the companies, investors are frightened that the value will not be realized by those who own shares. So perhaps the issue is that most investors think that risks like inflation and low growth are easier to quantify than what might seem, at least from a distance, the unpredictable whims of Chinese regulators.

Many (actually most) people, as they age, are unable and unwilling to adapt their view of and their interaction with the world – as the world continues to change.

They might have been really great and figuring out and understanding how to interact for a set time period when things were operating pretty much the same way. However, so much has changed (I won’t bore you with a list- but it goes way beyond the way the Fed/elected officials are acting – and you can make your own list), that I am actually not surprised at all that certain “titans” are passed their prime and can’t make sense of the changes.

For example, my dad was “on fire” making money during the 1970’s buying crap bungalows and using free child labor (my brother and me) to fix them up and maintain them. For that period in time, the world made sense to him and he was confident interacting in the world and he made some money. However, for the last 20 years, he has pretty much believed, said and acted as if the world, and especially the US, has gone to “hell in a handbag”. I used to give him the “facts” of an improving world (longer lives, healthier, wealthier, access to food/water etc) but it didn’t work. Now, I just settle in to listen, while periodically checking in on my portfolio and throwing in an “Uh huh”

Then I vow to never, ever be the type of person who gets “fixed” in yesterday. When my kids talk, I do more than listen- they are my “free” education about the world as it is today and tomorrow.

GLTA

H- can you move this to “Somebody has to be Wrong”?