The US economy added 943,000 jobs last month, the BLS said Friday.

That was more than expected, and came as welcome news on the heels of an ADP report which suggested hiring last month was far more subdued than economists anticipated.

By Friday, consensus was looking for 870,000 on the headline NFP print. The range, from six-dozen forecasters, was 350,000 to 1.2 million.

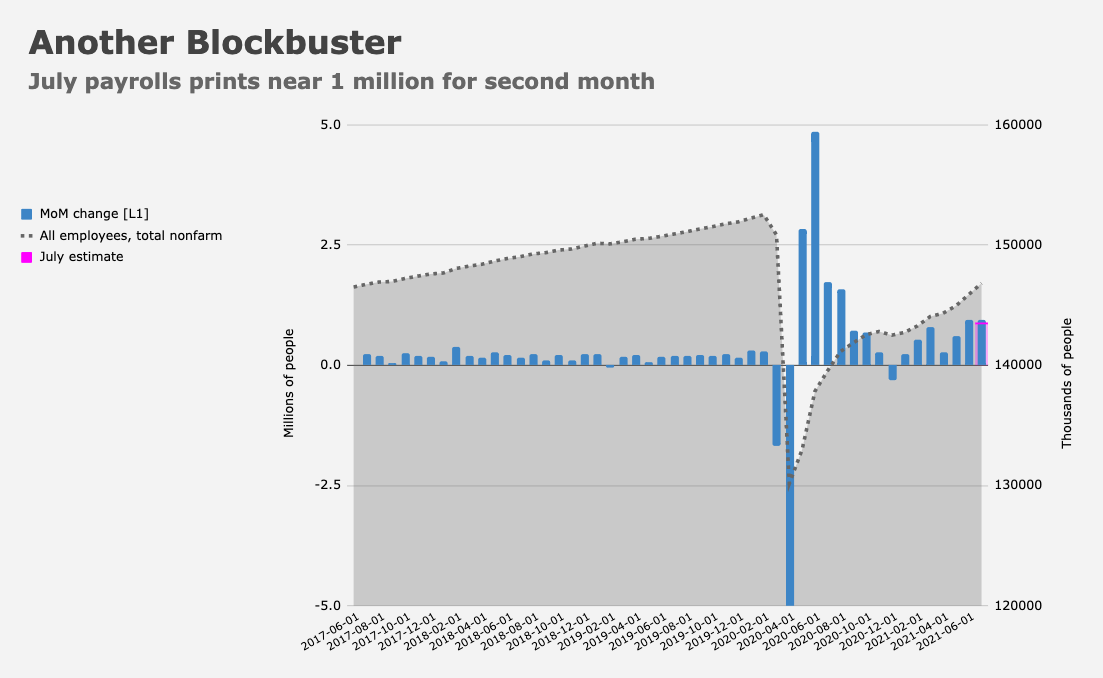

Notably, revisions added 88,000 to June’s headline (and 31,000 to May). That brought June’s total to 938,000. So, July made two consecutive months of payrolls above 900,000 (figure below).

Employment in leisure and hospitality jumped by 380,000, more than twice the number from the lackluster ADP report. Two-thirds of those jobs were concentrated in food services and drinking places.

Manufacturing payrolls rose 27,000, slightly more than expected. That, on the heels of a 39,000 gain in June.

Private payrolls rose 703,000, matching estimates and more than doubling what now appears as an incongruous ADP headline.

The unemployment rate sank sharply to a new pandemic-era low of 5.4% (figure below). That was much lower than the 5.7% economists expected and below the lowest estimate from 71 forecasters.

Employment rose by 221,000 in local government education and by 40,000 in private education. Those figures came with the usual caveats. “Staffing fluctuations in education due to the pandemic have distorted the normal seasonal buildup and layoff patterns, likely contributing to the job gains in July,” the BLS said, adding that “without the typical seasonal employment increases earlier, there were fewer layoffs at the end of the school year, resulting in job gains after seasonal adjustment.”

Average hourly earnings were stronger than expected, but on a quick read, there wasn’t much to suggest any “price spirals” are in the offing. Earnings rose 0.4% MoM, the same as June and more than the 0.3% the market expected. The YoY print was 4%. Consensus there was 3.9%.

The participation rate rose to 61.7%.

Generally speaking, it was a solid report. It certainly came as a relief in the context of ADP. But it’s doubtful to move the needle much when it comes to the macro zeitgeist, assuming you can discern an overarching narrative amid multitudinous crosscurrents and rampant uncertainty.

Updating the “MIA” chart to incorporate July’s headline print and revisions to May and June finds the US economy still down 5.7 million jobs from pre-pandemic levels (figure below).

“Overall a solid number, although not one that will shift the prevailing macro paradigm,” BMO’s Ian Lyngen remarked on Friday.

For markets, the immediately relevant question is how much further this gets the labor market towards meeting the Fed’s “substantial further progress” threshold. With Clarida now in the “hawk” camp, dovish holdouts are apparently diminishing.

“The US jobs market has posted a solid set of figures for July with employment gains exceeding expectations, unemployment falling, wages accelerating and the participation rate increasing,” ING wrote. “Momentum is building toward early Fed policy action.”

Like everything else these days, “early” is a relative term.

does anyone have conclusive take on ‘data freshness’ … is ADP or BLS ‘fresher’? Which or either could be considered the tip of spear? Or, are we the investment ecosystem just responding to most current data reported, regardless of its date of origin?

ADP report is a forecast of the coming BLS data. ADP uses their own proprietary data for about 1/5 of US labor force, adjusted for the difference between ADP’s client base and the national labor market and for seasonality, and historical relationship between their data and BLS data, to predict what the BLS data will be.

As such, I’d consider the BLS data fresher, or better anyway.

https://adpemploymentreport.com/common/docs/ADP-NER-Methodology-Full-Detail.pdf

It seems to me that another source of employment data would be the IRS, via payroll tax. I’ve not heard of that being used.

The job report I care about: Do I have a job?