One recurring theme over the first half of 2021 revolved around the notion that even if discretionary positioning in equities was stretched, systematic strats had ample scope to re-leverage in the event volatility normalized and remained well-behaved.

Discussions around systematic positioning come in a variety of flavors ranging from the exceptionally granular to the general. I prefer the former not because I love math or revel in what, for many market participants, still counts as “esoteric” terminology, but rather because if a thesis rests on assumptions about systematic positioning, it needs to be justified quantitatively. Qualitative assessments aren’t much use when it comes to predicting the behavior of emotionless algorithms.

As regular readers are acutely aware, it’s possible to predict, with some degree of accuracy, how systematic strategies will behave under certain assumptions about volatility. Those assumptions need not necessarily hold, but you can make a variety of educated guesses which can be helpful in determining, for example, whether the vol control universe is likely to support the market with a “background” bid for equities in the near-term.

In the latest edition of the bank’s weekly asset allocation series, Deutsche Bank’s Parag Thatte called equities a “notable exception” at a time when cross-asset positioning is moving back towards neutral.

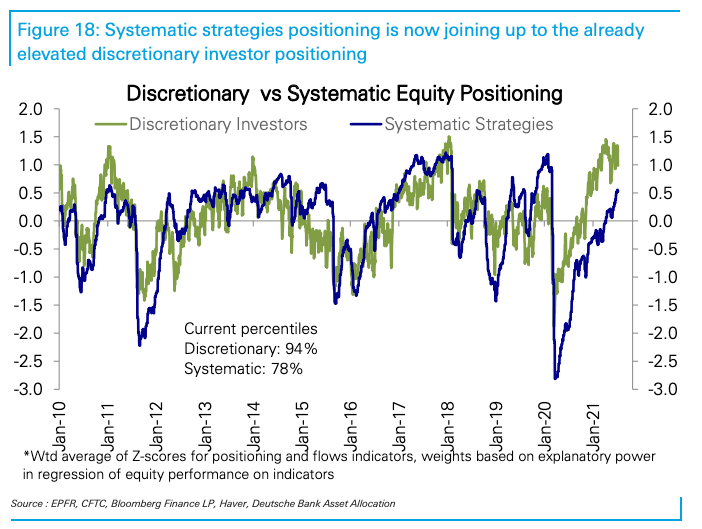

The bank’s overall equity positioning measure still sits at the top of the range, which isn’t surprising. What’s notable, though, is that systematic strategies are now “joining up to already elevated discretionary positioning,” the bank said (figure below).

Systematic positioning now sits in the 78th percentile on Deutsche’s measure, after climbing steadily. That, as discretionary positioning stalled, mostly because it couldn’t get much more stretched.

Re-leveraging from systematic strats comes courtesy of declining vol. To deploy Charlie McElligott’s catchphrase, “volatility is your exposure toggle.”

Deutsche flagged more aggressive positioning from vol control funds and CTAs (figures, below).

“Some market participants are worr[ied] that when earnings season kicks in, stocks could run low on willing buyers,” Bloomberg’s Elena Popina wrote Monday, referencing the same Deutsche Bank note. “While discretionary investors have long embraced equities, peers who rely on rules-based strategies were cautious during most of the post-pandemic advance, until lately, when they began loading up on stocks as price swings subsided to pre-pandemic levels.”

It would be (far) too hasty to cite this snapshot in declaring the equity rally “exhausted” because systematic strats are finally catching up to discretionary positioning, leaving a dearth of buyers. The above is more… well, it’s just what I called it. It’s a snapshot, and should be considered as such.

But it’s most assuredly worth mentioning. Again: Scope for additional systematic re-risking has underpinned many a bullish narrative at a time when valuations are stretched and discretionary investors are seen maxed out.

Of course, with so much money on the sidelines (i.e., sitting idle in money market funds), you’ll always have a “dry powder” argument if that’s your preferred crutch (figure below). Buybacks are poised to accelerate into year-end and then there’s the reality of ultra-low bond yields (i.e., “TINA”).

That said, bears and skeptics can also avail themselves of a veritable smorgasbord of confirmation bias. Multiples are at dot-com levels (they’re at 100-year highs on a trailing basis), growth is peaking and equities have already doubled from the pandemic lows.

For the bearish contingent, Deutsche Bank offered a bit of additional cautionary color. “The last two months have seen a break in the synchronized risk-on move across asset classes,” the bank said, in the same note cited above.

“Large cap US equities have continued to edge higher, but small caps and other regional equities have been moving sideways to down and US equity breadth has also been weakening as less than half of S&P 500 stocks are trading above their 50-DMA,” the bank went on to remark, citing falling bond yields, sideways credit spreads, drifting EM equities and wider EM spreads, in noting that a measure of cross-asset momentum breadth now sits “just below the middle of the band… a sharp contrast from the extremely positive levels earlier in the year when every asset class was firmly in strong risk-on territory.”