So, you want to be a contrarian?

Well, prepare yourself for the ultimate paradox. In the back half of 2021, being contrarian may mean embracing what, in many respects, remains the epitome of “consensus.”

In the June edition of BofA’s Global Fund Manager survey, respondents identified “Long Tech Stocks” as the third-most crowded on the planet, just behind “Long Bitcoin” and “Long Commodities.” It was a close race (figure below).

If you’re familiar with the survey, you’re aware that some manifestation of “Long Tech” topped the crowded trades list habitually dating back to mid-2017. Although other trades sporadically took the top spot, for most of the last four years, “Long Tech,” “Long Tech & Growth,” and “Long FAANG + BAT” were “crowded” mainstays.

And yet, in the current macro environment, characterized as it is by reflation obsession and a lingering sense that, despite powerful rallies for reflation-linked trades (commodities had their fifth-best start to a year in a century, for example), tech and growth shares more generally are out of favor.

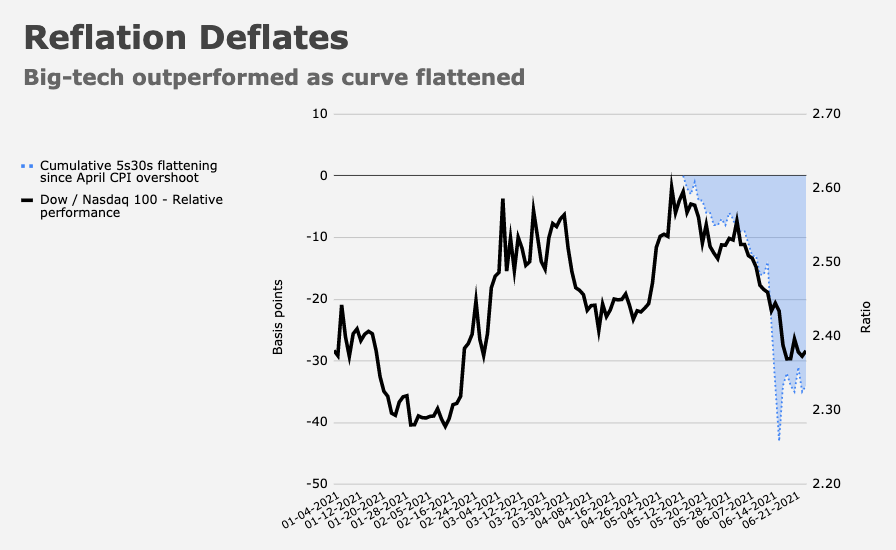

Or at least they were out of favor. The power-flattening in the curve since mid-May was accompanied by outperformance from growth shares, which bested their value counterparts by the widest margin in two decades in June. Similarly, big-tech has outperformed handily (figure below) since the April CPI “shocker” (on May 12)

The general sense among many market participants is that yields will move higher again into year-end, that the curve will probably re-steepen and that there’s more gas in the tank for the reflation trade in all its various manifestations.

In other words: A majority seem to believe the recent strength in duration-linked trades will prove fleeting. The assumption is that the rally in bonds and outperformance from growth shares was just a nostalgic interlude — a requiem for the old macro regime that will inevitably give way to more reflation obsession as re-openings continue and yields rise anew.

Given that assumption, “everyone’s favorite H2 ‘contrarian’ trade is ‘Long FAANG,'” BofA’s Michael Hartnett wrote, in his latest. He called that an “oxymoron,” underscoring my “ultimate paradox” characterization (here at the outset).

Note that for all the talk of a macro regime shift and the death of duration-linked equities trades, an admittedly simplistic look at the contribution to the S&P’s blockbuster first half shows that tech played an outsized role, albeit with banks and energy (reflation expressions) doing their part too.

The most poignant visual when it comes to underlining the oxymoronic nature of “FAANG as a contrarian trade” is, of course, the familiar SPX concentration chart (below).

The top-five stocks still comprise more than a fifth of the index.

Oh, and for good measure, H2’s “contrarian” trade is overbought (figure below).

So, if you want to be a “contrarian,” you’ll need to pile into the third-most crowded trade on Earth knowing it’s overbought, and somehow explain to yourself how you’re “going against the grain” by overweighting a handful of stocks that you’re already absurdly overweight in a simple S&P 500 index fund.

Happy trails.

It is 333 BC and once again we (Alexander knot so Great ) are facing the Gordian Knot Riddle. Great post made to order for the Day …

Last night I watched 60 Minutes take on recent cybercrime. The extensive infiltration of the global internet (most likely by Russians) may require massive hardware replacement. That would do something for tech stocks. As an aside, what mandates that P/E multiples have to ultimately revert to historical norms.

One thing I’ve noticed- some of these big scenarios are advancing quickly and then reversing quickly- this seems to be part of the last couple of years of cycles getting shorter. To me, that indicates some sort of underlying instability- which this reverse repo news may exacerbate. I recently heard Diego Parilla say We know where we are going, but we don’t know what the path looks like…