I joked Friday about “large numbers” and the irresistible urge to deploy them in the service of “wowing” the audience.

While I’m reasonably sure many market participants are as desensitized as I am to the words “billions” and “trillions” by now, I feel compelled to keep highlighting global equity flows. I suppose it’s the whole “irresistible” part.

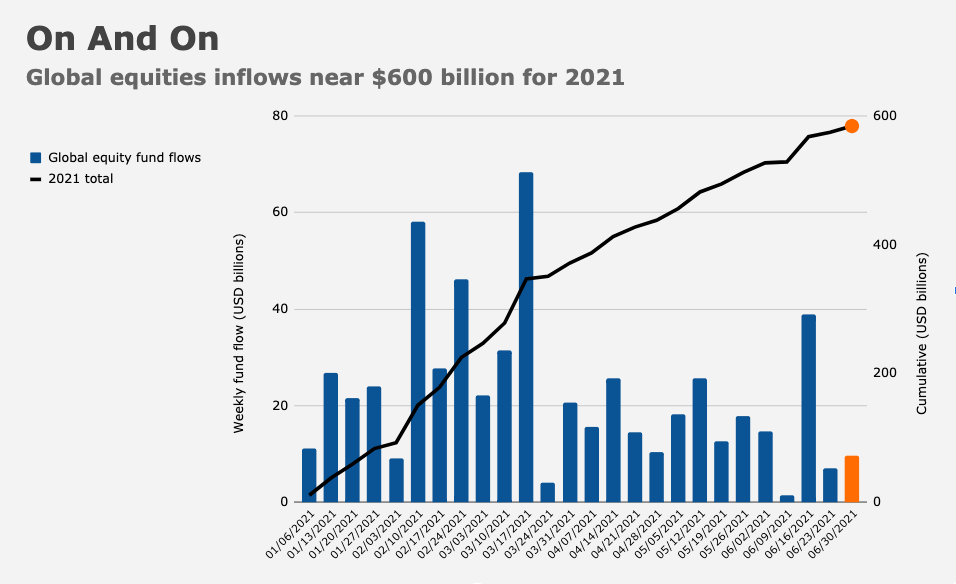

In the latest weekly reporting period, global equity funds took in another $9.6 billion, taking the YTD haul to — large number alert — $584 billion (figure below).

Large number jokes aside, this really is… well, a joke, for lack of a better way to put it.

For months, I cautioned against extrapolation, but with half of 2021 officially over, it’s no longer a stretch to make comparisons like BofA’s Michael Hartnett made in the latest edition of the bank’s weekly “Flow Show” series. “2001-2020 stock inflow was a cumulative $0.8 trillion,” he wrote. “In 2021, the inflow is annualizing $1.2 trillion.”

That’s another reliable pillar of support for equities and helps to explain the market’s resilience.

The first half was the seventh best for global equities in the past century, Hartnett went on to say, noting that the annualized return following the last six best first-half gains was -9% in six months. Somehow, I doubt that’s going to dissuade anyone afflicted with “FOMO” (or any other popular market acronym).

Notably, buybacks are — err — back. “In the first three months of 2021, companies in the S&P 500 spent $171.5 billion on stock repurchases,” Bloomberg wrote Saturday. Although that’s not back to pre-pandemic levels, it marked a big increase from the prior three quarters (figure below).

Recall that Goldman sees corporates as the largest source of net equity demand during the remainder of 2021. Last week, the country’s largest banks committed to doling out more money to shareholders after easily clearing the Fed’s stress test.

For all the shrill warnings about nosebleed valuations, there doesn’t seem to be a dearth of interested parties when it comes to equity demand, even as the pace of inflows to stock funds has slowed (figure below).

For his part, Hartnett sees no shortage of potential bearish catalysts among H2’s “known unknowns.” He mentioned inflation eroding margins and possible impediments to the Biden administration’s infrastructure deal, as well as the prospect that “inflation ends the Fed’s ‘strategic ambiguity’ on tightening.”

It’s also possible, he said, that we’ve seen “peak US consumption as artificial supports end” just as uncertainties around labor, taxes and health collide with demographics to keep the US savings rate elevated. He conjured Japan.

But those are tomorrow’s concerns. For now, it’s “kinda dull,” Hartnett wrote. And you “don’t sell a dull market.”

Yes, I believe the newfound wealth in the world is among the most understated reasons for prolonged asset chasing, with no end in sight

Not that dulll under the surface – sector swings as active as ever.