US manufacturing activity was robust in June, while price pressures continued unabated.

That was the general takeaway from the latest data, out Thursday.

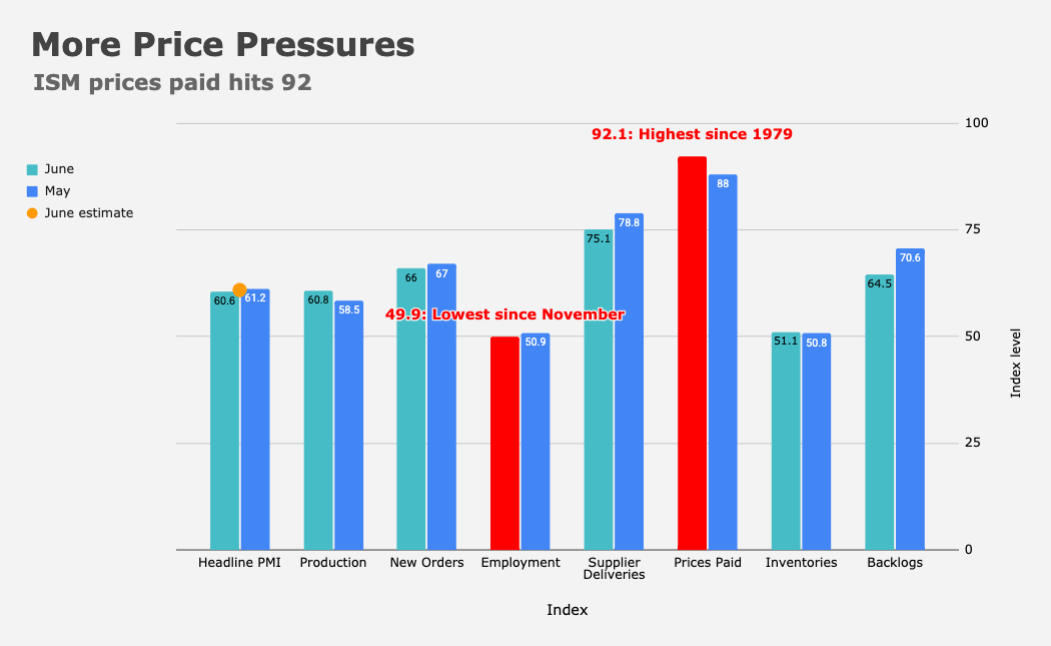

ISM manufacturing printed 60.6 (figure below), slightly below the 60.9 consensus, but still indicative of vigorous expansion. Of the five subindexes that comprise the headline PMI, four were in growth territory.

The gauge has printed 60 or above in five out of six months this year.

The breakdown showed the production index rising, the new orders gauge falling and, notably, the employment index dipping into contraction territory (figure below).

Meanwhile, the prices paid index printed 92.1. That was the highest in more than four decades.

“Record-long raw-material lead times, wide-scale shortages of critical basic materials, rising commodities prices and difficulties in transporting products are continuing to affect all segments of the manufacturing economy,” ISM’s Timothy Fiore said Thursday, adding that “worker absenteeism, short-term shutdowns due to parts shortages, and difficulties in filling open positions continue to be issues that limit manufacturing-growth potential.”

The accompanying anecdotes were — what’s the right word? — lively.

“Higher prices, inflation and lack of available labor are impacting all organizations in our supply chain,” someone in Electrical Equipment, Appliances & Components said. “Supply disruptions continue, with no end in sight!,” shrieked a respondent from Nonmetallic Mineral Products. “Lack of labor is killing us,” someone from Primary Metals lamented.

Meanwhile, the final read on IHS Markit’s US manufacturing gauge fell slightly from the flash print (to 62.1 from 62.6). The input prices gauge rose to 82.8, the highest in series history. The employment index dropped to a six-month low.

“June saw surging demand drive another sharp rise in manufacturing output, with both new orders and production growing at some of the fastest rates recorded since the survey began in 2007,” IHS Markit’s Chris Williamson said. “The strength of the upturn continued to be impeded by capacity constraints and shortages of both materials and labor, however, meaning concerns over prices have continued to build.”

This is a broken record. There’s nothing to add. The bottlenecks persist. The Fed says “transitory.” The Nonmetallic Mineral Products folks say “no end in sight.” But what do they know? They’re not PhDs.