Inflation is “The defining macro story of this decade,” Deutsche Bank declared, in a highly engaging note dated Monday.

Apparently, the bank intends to publish a new series of papers going forward in the interest of furthering what Chief Economist David Folkerts-Landau described as “intellectual diversity.”

The new series is called “What’s in the tails?” and aims to “stimulate debate” by presenting “reasonable alternatives” to the bank’s house views and central forecasts.

That sounds promising, or at least interesting, and the inaugural edition finds Folkerts-Landau joined by Peter Hooper and Jim Reid, who together explore a scenario in which post-pandemic policy shifts result in unmoored inflation outcomes.

While it’s decidedly difficult to differentiate between obligatory nods to the desirability of more equitable social developments and earnest praise for policies aimed at engendering them, Deutsche kicks things off by noting that in the post-pandemic reality, the fear of inflation is disappearing in advanced economies to make way for more noble objectives. “Replacing it is the perspective that economic policy should now concentrate on broader social goals,” the bank said, adding that,

Such goals are as necessary as they are admirable. They include greater social support for minority groups, greater equality in income, wealth, education, medical care, and more broad-based economic opportunity and inclusion. They should be front and center of the policies of any government in these times

Lofty rhetoric and soaring praise. To the extent it’s sincere, that’s great. I would note that I generally eschew normative statements in these pages, because although I’m just as confident as anyone else in my own assessment of what’s “right” and “wrong,” unlike most people, I also acknowledge that at the end of the day, there’s no such thing as “right” and “wrong.” Those are everywhere and always subjective assessments.

That said, some goals currently being pursued with increased vigor by policymakers are about as close to objectively “right” as it’s possible to get. Expanded access to medical care, for example, is “good” for everyone because even if you don’t believe in the principle of equality, you probably agree that mass pestilence is “bad.” Diseases don’t tend to respect any boundaries tied to wealth or social status. You may be able to better avoid communicable illnesses if you’re wealthy and it’s true you can afford better care for things like cancer, but ultimately, the rich would likely agree with the idea that a healthier society is an objectively “better” place for everyone, even if “better” just means “safer.”

In any event, these new goals (the objectives outlined by Deutsche in the excerpted passage above) are evident in all aspects of policymaking in advanced economies in 2021. There are, of course, lawmakers who question the desirability of pursuing them at all costs, but, as discussed here on too many occasions to count, the pandemic was the last straw. It laid bare myriad societal inequities which were already quite glaring, and concurrent racial tension in the US resulted in anarchic scenes in cities across the country last summer.

Folkerts-Landau, Hooper and Reid caution that as noble as the pursuit of equality and social justice are, monetary authorities shouldn’t lose track of their obligation to guard against price spirals.

“Despite the shift in priorities, central bankers must still prioritize inflation,” they wrote, adding that,

History has shown that the social costs of significantly higher inflation and greatly expanded debt servicing obligations make it hard, if not impossible, to reach the social goals that the new US administration (among others) is keen to achieve. We fear that the vulnerable and disadvantaged will be hit first and hardest by mistakes in policy.

It’s certainly true that spiraling inflation would hit some of the same demographic cohorts the current policy conjuncture aims to assist. Lower education levels are associated with lower incomes and thereby greater shares of disposable income spent on goods and services likely to experience price increases (e.g., groceries and gas).

I explored that dynamic at length in “The Word Is ‘Inflation.’ With A ‘K’.” At the time, inflation expectations were moving sharply higher for Americans with a high school education or less and for those earning under $50,000 per year, according to the New York Fed’s survey. Since then, inflation concerns appeared to infect the next rung on the ladder (figure below), as views from the “some college” cohort spiked.

Other surveys of consumer inflation expectations show broad-based concerns, with the University of Michigan’s poll garnering quite a bit of attention last month.

After noting the extent to which the pandemic “accelerated” the shift away from orthodox thinking, Deutsche fretted that “two of the biggest historic constraints on macroeconomic policy – inflation and debt sustainability – are increasingly perceived as not binding.”

With those constraints no longer tying policymakers’ hands, they’re free to expand the purview of macro policy, which is just another way of saying that both lawmakers and technocrats are getting more ambitious when it comes to tackling critical social issues.

Today’s policy goals “go far beyond simply stabilizing output across the business cycle,” Folkerts-Landau, Hooper and Reid wrote, on the way to citing the Fed’s tweaked operational guidelines and the extent to which other countries are following the US, even Germany, the bastion of budget rigor. Summing up, they wrote that,

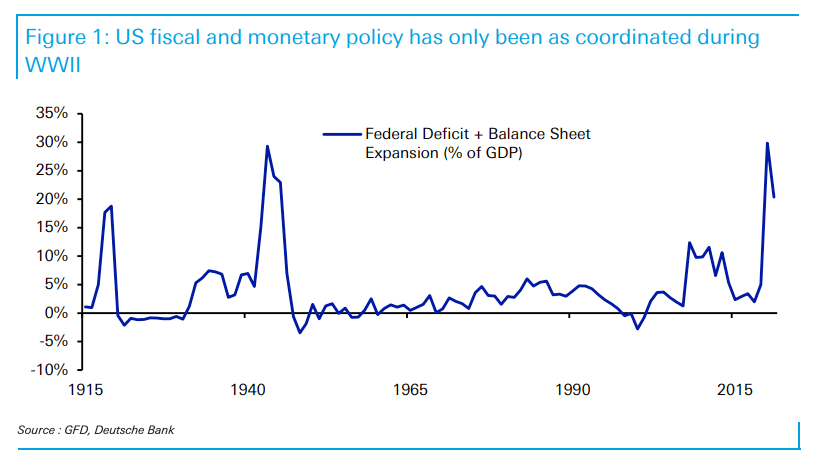

We are witnessing the most important shift in global macro policy since the Reagan/Volcker axis 40 years ago. Fiscal injections are now “off the charts” at the same time as the Fed’s modus operandi has shifted to tolerate higher inflation. Never before have we seen such coordinated expansionary fiscal and monetary policy. This will continue as output moves above potential. This is why this time is different for inflation.

Their concern is straightforward (and all too familiar). They worry that if the US economy overheats next year, the Fed won’t move fast enough to curtail inflation pressures.

If the Fed gets behind the curve (and remember, average inflation targeting essentially commits them to being behind the curve), “the consequence of delay will be greater disruption of economic and financial activity than would be otherwise be the case when the Fed does finally act,” Deutsche said, warning that such a scenario “could create a significant recession and set off a chain of financial distress around the world, particularly in emerging markets.”

Folkerts-Landau, Hooper and Reid went on to suggest that in an effort to make up for mistakes made after 2008, policymakers are in the process of overdoing it. “There is a striking difference between today’s response and that of prior financial crashes as today’s stimulus dwarfs the response to the crises in 2008 and the 1930s,” they remarked, referencing the self-explanatory figure (below).

Getting more granular, Deutsche noted the “explosive spike in money supply” in the US and the fact that stimulus has actually managed to engineer a record high in disposable personal income on the heels of what, briefly, was the worst economic downturn in a century. No small feat.

“Even the lowest savings rate during the pandemic, 13%, was still above any level seen since the early 1980s,” the bank observed.

From there, the argument was predictable. Consumers will spend as the economy reopens (Americans aren’t exactly known for being a society of scrupulous savers) and additional stimulus (e.g., Joe Biden’s American Families Plan) could drive output well above potential and push the unemployment rate to somewhere between 2% and 3%.

After declaring it “entirely possible, if not likely” that an overheating economy (e.g., the “high growth” scenario shown in the visual) triggers a “substantial and sustained” inflation impulse, Deutsche delved into expectations.

Essentially, the bank cautioned that just a few hot prints might be enough to instill an inflationary psychology that would prove difficult to reverse.

“Even if they are transitory on paper, they may feed into expectations just as they did in the 1970s,” the bank said. “The risk then, is that even if they are only embedded for a few months they may be difficult to contain, especially with stimulus so high.”

The media would doubtlessly play a role along the way. They already are.

Ultimately, Folkerts-Landau, Hooper and Reid closed with a flourish. After citing a series of global factors and structural forces that could exacerbate inflationary pressures (not least of which is the prospect that the dash to engineer greener economies could push up prices), they concluded with a series of somewhat bombastic passages including the following:

We worry that the painful lessons of an inflationary past are being ignored by central bankers, either because they really believe that this time is different, or they have bought into a new paradigm that low interest rates are here to stay, or they are protecting their institutions by not trying to hold back a political steam roller. Whatever the reason, we expect inflationary pressures to re-emerge as the Fed continues with its policy of patience and its stated belief that current pressures are largely transitory. It may take a year longer until 2023 but inflation will re-emerge. And while it is admirable that this patience is due to the fact that the Fed’s priorities are shifting towards social goals, neglecting inflation leaves global economies sitting on a time bomb.

Finally, they warned that by the time central banks are compelled to act, it could be politically impossible. At that juncture, the bank suggested, voters will be convinced of the idea that low unemployment and a more equitable society are worth the tradeoff.

That notion would have to be jettisoned if “inflation returns in earnest,” though, Deutsche warned, adding that “rising prices will touch everyone [and] the effects could be devastating, particularly for the most vulnerable in society.”

“Even if they are transitory on paper, they may feed into expectations just as they did in the 1970s,” the bank said.

Back then labor unions were still strong and many more payment streams were subject to COLA adjustments. Those are now distant memories.

German-trained economists …..

Indeed. In addition, the demographic situation was the complete opposite of now.

While the German psyche is understandably Jaundiced against inflation these are thoughts that are reasonable to air. Thank you very much.

This article feels appropriate.

https://www.theatlantic.com/magazine/archive/2020/12/can-history-predict-future/616993/

I refuse to accept the proposition that it would be “politically impossible” for the Fed to raise the prime rate, in. 25 or .50 point increments, to 3.0, 3.5, 4.0, or even higher if “out of control” inflation warranted. The Volker recession of 1981 was sharp and painful — I know, I had just graduated from college — but it crushed inflation like a bug and the economy, with a little Keynesian stimulus, was booming by ’83.

“I refuse to accept the proposition that it would be “politically impossible” for the Fed to raise the prime rate, in. 25 or .50 point increments, to 3.0, 3.5, 4.0, or even higher if “out of control” inflation warranted.”

It’s definitely a narrative I see and hear widely. I also disagree that it’s “politically impossible”.

Inflation – blah, blah, blah. Bottom line for something we think is crucial to economic health; we don’t have a clue. Once we figure out what it is and how it comes about, then we’ll have a chance to manage it within specified limits. It’s interesting that there are few articles on what inflation is (or might be) and lots on which direction it’s headed. For now we are left playing ‘crack the whip’ with inflation expectations.

To stimulate discussion, I would suggest that inflation is a way (and not the most efficient) to measure societal fear. Economists look at market indicators, maybe they need to move upstream and keep track of fear issues and levels – fear of a virus pandemic, nuclear war, climate change, government collapse, not earning a living wage, identity theft, no health care, random gun violence and a whole lot more. Add a time factor to the fear tracker and you might have something. Perhaps, if I believe my fears won’t manifest for at least 18 months then my inflation expectations are low.

I think as usual the real question is political will for policy. Inflation is a long term problem if we do nothing to enhance supply to meet demand. We are effectively seeing the results of supply being curtailed for 12+ months then exposing it to latent demand built up over 12+ months in a supply chain with no built in surge capacity or buffer stock due to poorly adopted “just in time” practices. If we do nothing but control interest rates there will be huge consequences to now using the tail to try to unwag the dog. There were many problems with using low interest rates and bond buying in place of policy solutions to the GFC and then to Covid. I’m not sure just reversing those works after backing yourself into a corning without rather extreme pain. In what way do we suppose a strong sustained tightening wave will impact the countless zombie enterprises and then the economy and financial institutions as waves of implosion rock assets of nearly ever type all while consumer debt interest rates rise on stagnant incomes and rising inflation?

Unfortunately policy responses seem as far away as they ever were. Even in a dire case where we see Trump back in office with full control of the government… we really are not likely to see policy that addresses the needs of the economy to stabilize and recover.

“In what way do we suppose a strong sustained tightening wave will impact the countless zombie enterprises and then the economy and financial institutions as waves of implosion rock assets of nearly ever type all while consumer debt interest rates rise on stagnant incomes and rising inflation?”

A sustained tightening wave would drive a stake through the heart of many zombie companies, curtail (if not crush) consumer demand, and cause a lot of junk to be written off. Also: end of inflationary impulse. Creative destruction, anyone?

Oh definitely, how much destruction though? What consequences? Especially if there is not a policy response. Sometimes a forest fire takes decades to regrow when it burns too hot, they also can take even fire adapted animals out of the picture.