The de-rating is upon us.

That’s one notable takeaway from some of this week’s earliest analyst color.

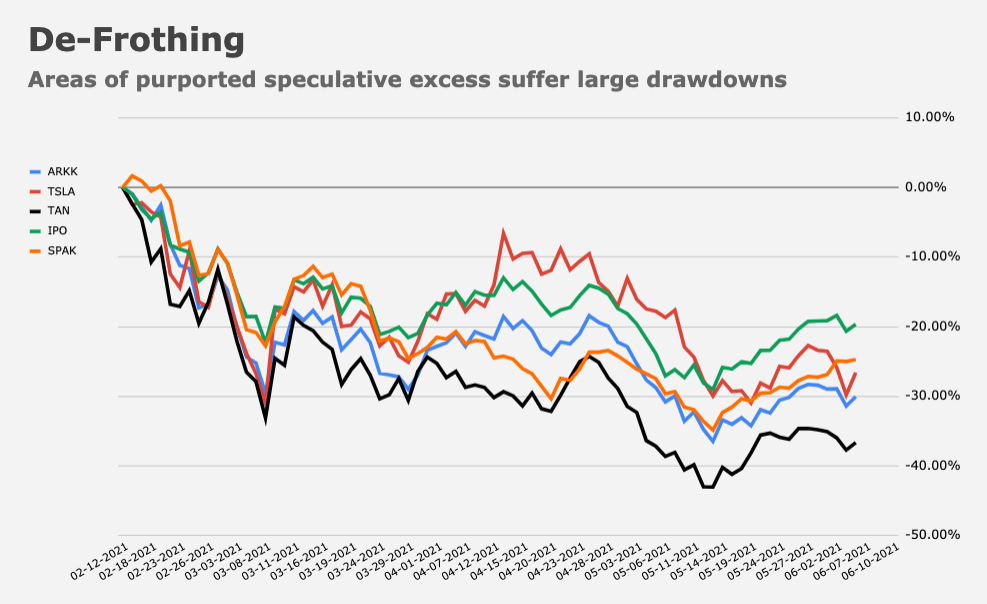

Late last week, I suggested that one “could make the case that the rates mini-tantrum (in Q1) did just enough damage in terms of catalyzing steep declines for so-called ‘hyper-growth’ shares and other corners of the market seen as woefully stretched, to put the broader market in a less perilous position headed into summer.” The updated figure (below) is simple enough.

Rising yields took the wind out of the sails for some of the frothiest corners of the market. That the drawdowns shown in the figure played out against a broader market that mostly held up is a positive development, I’ve generally argued.

For Morgan Stanley’s Mike Wilson, though, the de-rating observed in expensive areas of the market and in lower-quality names, will eventually manifest in multiple contraction for the broader US equities complex.

That’s part of the bank’s “mid-cycle transition” thesis, and Wilson reiterated it to kick off the new week.

“Many we speak with think this time is different because the Fed and other central banks are committed to staying dovish for longer than normal,” he said.

To be sure, Wilson doesn’t suggest the Fed will blink. Policymakers mean what they say when it comes to persisting in accommodation until the data actually “realizes” (as opposed to policymaking based merely on forecasts). Rather, Morgan’s contention is simply that a dovish Fed today means policy will need to catch up down the road.

Markets being forward-looking, Wilson said stocks “will discount [a faster Fed tightening later] by proactively taking valuations lower through the equity risk premium channel, rather than waiting for cues from the bond market.”

“It’s already happened in the most expensive and lower-quality parts of the equity market, and we think this de-rating will eventually reach the S&P 500,” Wilson cautioned. The figure (above) illustrates the point.

Writing last week, SocGen’s Andrew Lapthorne noted that although a Value factor is up nearly 20% in 2021, its forward multiple has actually declined “due in part to the large EPS upgrades, the forecast sharp rebound in earnings post last year’s slump, and the mechanical rotation towards whatever is cheapest in the market.”

Growth, meanwhile, is still “extremely expensive,” he said.

“As much as they may be underperforming, globally [Growth shares] are still up 8.7% YTD and at almost 33x forward EPS, almost three times more expensive than Value stocks,” Lapthorne remarked.

Rotation is healthy- it means assets are staying in stocks rather than fleeing. As long as participants are ok to invest, there is no reason for there to be contagion. As far as value shares and the market generally go, a lot of strategists musings are quite speculative. A great deal depends on the continued course of the virus and economic and political policies enacted both here and abroad. A correction can come at any time- but the cause will only be known (maybe) in hindsight. My own guess is for a P/E compression going forward- especially in growth plays. But that does not mean that stocks go down, even growth stocks.