Inflows to global equities continued apace over the last week, despite considerable “chop” across stocks tied to inflation jitters.

Investors plowed another $13 billion into global equities, bringing the total for 2021 to within $5 billion of the half-trillion mark — with seven months left in the year (figure below).

Just $1.2 billion of the most recent weekly haul went to US stocks. That was the least in nearly two months.

In the latest edition of the bank’s popular weekly “Flow Show” series, BofA’s Michael Hartnett pointed to two possible analogues, one for the pessimists and one for the optimists.

“Bulls can point to 2017/18, strong growth, range-bound yields, dithering Fed, and await the final melt-up,” he said. “Bears can point to 2007/8, as a sinister series of deleveraging ‘events’ ended with a ‘Minsky Moment.'”

On Thursday, in “It’s Amazing We Haven’t Had Another Crash,” I detailed some of 2021’s notable potholes (or land mines). The figure (below) illustrates the fallout from what many called the largest margin call of all time. The Archegos saga was a land mine that actually exploded and yet, somehow, the market didn’t lose its legs.

Similarly, in “The Thrill Is Gone,” I talked a bit about what might be described as “peak froth.” I think that’s ongoing.

Even after steep losses for the likes of Cathie Wood’s ETFs, one still gets the distinct impression that “hyper-growth” can deflate further assuming the macro zeitgeist continues to shift.

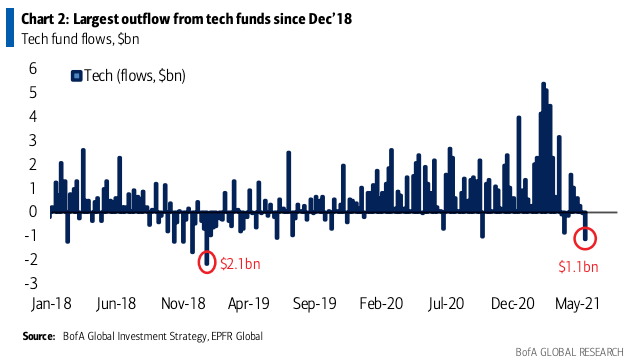

Apropos, tech funds just witnessed the largest outflow since December 2018 (figure, below, from BofA).

Notably, financials, energy and materials have taken in more (together) since January 2020 than tech, indicative of the evolving macro regime.

As for which of the two analogues mentioned above “rhymes” most with the conjuncture in 2021, BofA’s Hartnett says neither.

“We prefer the 1967-69 analogue of interest rates unanchored by large budget deficits attempting to pacify populist and polarized electorates, an excessively easy and complicit Fed [and] inflation rising to multi-year highs,” he said.

The value bull of 1968 is akin to the first half of 2021, Hartnett suggested, before noting it was “followed by the volatile bear of 1969.”

To alter one man’s catchphrase: “There’s always a dire narrative somewhere, and I’ll try to find it for you.”

Of course, every once in a while, the dire narratives prove prescient. “Bear Stearns is fine.”

“Of course, every once in a while, the dire narratives prove prescient. ‘Bear Stearns is fine’,” he said, speaking from the bridge tournament he didn’t want to come home from.