Inflation worries were back on the menu Friday, after data showed producer prices in China jumped the most in years amid higher commodity costs.

The 4.4% jump (figure below) was well ahead of consensus, which was looking for a 3.6% rise. Base effects mattered, but as SocGen’s Michelle Lam and Wei Yao wrote, PPI “still climbed a strong 1.6% MoM, owed mainly to the rise in energy and metal prices.”

China being the “producer to the world,” surging factory gate prices could presage higher consumer prices abroad. When you’re the world’s largest exporter, PPI is almost always amenable to some manner of semi-dour editorial spin. When China fell into factory gate deflation in August of 2019, it was seen as a coal mine canary. “The rest of the world could do without wholesale deflation in China at a time when the outlook for global growth and trade seems to get darker by the day,” I wrote, at the time. It also bode poorly for industrial profits. Fast forward to the present day, and sharply higher producer prices are again a canary, only this time they purportedly “threaten to stoke inflation around the world, adding to volatility in financial markets,” to quote Bloomberg’s pitch.

There are kernels of truth in any narrative. PPI deflation in China does have ramifications for the global macro cycle, and the corollary is that sharply higher producer prices could impact inflation (or at least expectations) abroad.

Domestically, consumer prices are tame. CPI did tick back positive in March after spending two consecutive months in negative territory. Cheaper pork has pushed consumer prices lower and a somewhat lackluster recovery in spending (the rebound in Chinese retail sales lagged the bounce in industrial output last year by several months) will probably drag on CPI, even as core perks up.

“Importantly, the rebound of core CPI indicates that the COVID-induced weakness in consumer demand and prices at the beginning of the year should be temporary, and we should see a recovery from here onwards,” SocGen’s Lam went on to say Friday. “Indeed, the latest holiday spending data support this view.”

Surging PPI isn’t all good news for producers, by the way. Margin pressure may begin to mount. “For Chinese businesses, rising factory prices mean higher profits and more capacity to repay debt [but] purchase prices for industrial companies rose even faster in March than the price of finished goods,” Bloomberg remarked Friday, in the same article linked above.

For markets, another worry is the read-through for a PBoC which is already inclined to tightening. “Markets may become increasingly concerned about pressures from rising inflation on Beijing’s policy stance,” Nomura’s Ting Lu said. “We expect Beijing will stick to its ‘no sharp policy shift’ commitment.”

Earlier this week, Bloomberg confirmed FT‘s previous reporting that the PBoC has instructed banks to keep lending stable at last year’s levels, potentially presaging the slowest credit growth in 15 years.

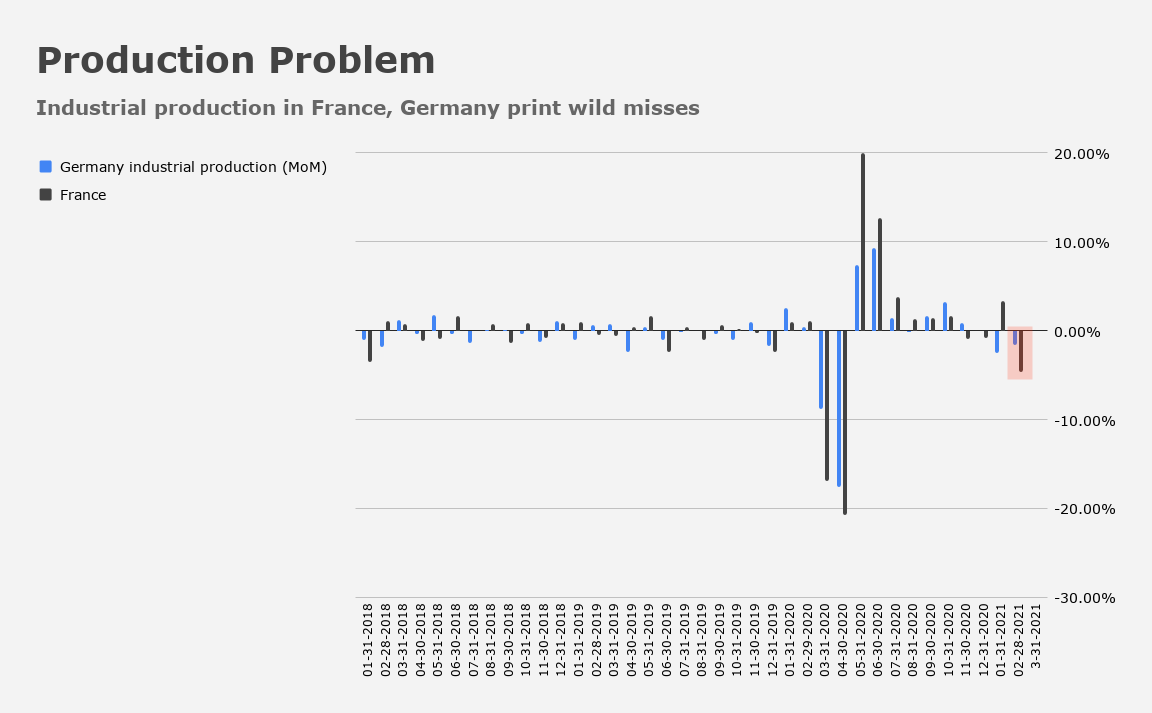

Meanwhile, in Europe, industrial production in Germany and France printed what looked, to the casual observer anyway, like wild misses for February. The MoM drop for Germany was 1.6%. The decline was 4.7% for France (figure below). Consensus was looking for gains of 1.5% and 0.5%, respectively.

This suggests that pandemic restrictions and ongoing stumbles along the road to vaccine rollout in Europe were hitting manufacturing, which has proven relatively resilient compared to the services sector.

The data is stale and you’re supposed to look through it. “The improvement in business confidence and positive trend in orders signal a positive outlook in industry,” Germany’s economy ministry assured markets, while acknowledging that “the future course of the pandemic poses uncertainties.”

“Timely indicators point to momentum building in the manufacturing sector,” Bloomberg’s Laura Cooper said Friday. It’s the services sector you should be concerned about in Europe. “That’s where eyebrows need to be raised,” she added.

Not everyone is sanguine. “French industrial production fell sharply in February, despite strong confidence indicators,” ING wrote, calling it an “unpleasant surprise” that “casts doubt on the hope that the industrial sector will be a driving force for the French economy in the first quarter and raises fears that GDP growth will be weaker than expected.”

The above underscores the futility in attempting to sort out any kind of coherent macro narrative a year on from the pandemic. Inflationary pressures are evident, but supply chain issues, surging commodity prices and base effects make for a difficult exercise in tasseography. In Europe, the vaccine debacle, rolling lockdowns and two-month delays on key data points, make for an equally ambiguous set of tea leaves.