Suddenly, there is an alternative.

Or at least that’s one way to look at the backup in bond yields.

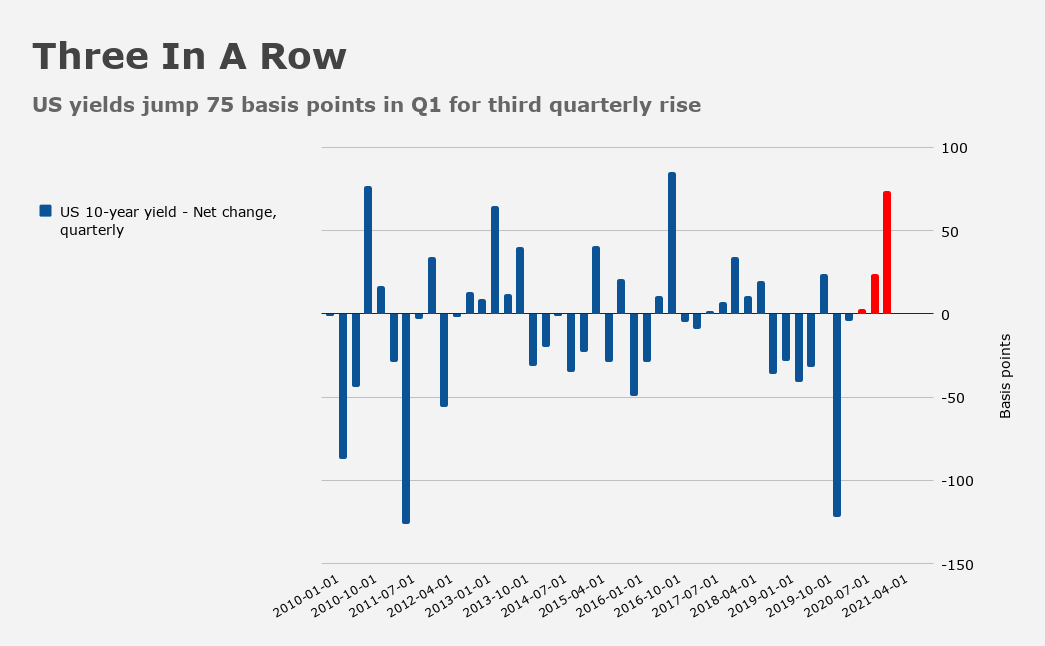

Treasurys’ performance in the first quarter was among the worst since 1980. 10-year yields rose some 80bps as the reflation trade kicked into high gear and growth expectations improved amid fresh stimulus and rapid vaccine rollout in the US. Indeed, Q1 was defined by what, on one benchmark, was the first bond bear market in four decades.

Although benchmark US yields ended the week around 1.72%, the 10-year reached 1.77% earlier in the week, as bonds reclaimed the spotlight after briefly yielding (get it?) the stage to the Archegos blow-up.

The last time 10-year US yields were higher than the S&P 500’s dividend yield, Donald Trump’s “phase one” trade deal with China was still making headlines and most people still thought of pandemics as plot fodder for Hollywood thrillers.

Speaking of Hollywood, the figure (below) features a classic American cinema reference which I fear younger readers might not fully appreciate. Fortunately, it’s a simple chart, so you needn’t have been alive and watching movies during the Reagan years to get the point.

There are now 100 fewer S&P 500 companies sporting a dividend yield higher than the 10-year Treasury rate compared to just three months ago.

Of course, when it comes to equities and bonds, the relative “attractiveness” argument is both frustrating and foundational. And nothing is more annoying than a foundational discussion that’s frustrating — you’re compelled to have the debate, but you don’t want to, because it’s notoriously bothersome and almost always ends inconclusively.

For example, someone at Baird called it a “tough balancing act,” telling Bloomberg that “I think if those yields rise, it becomes a more and more attractive place to park some money… but the price of those bonds is going to feel it.”

Ideally, you want to get it “just right,” where that means calling at least the near- to medium-term top in yields and, by extension, a pause in the first bond bear market many investors have ever seen. But this is complicated by concerns that bonds have the potential to be a source of volatility going forward, a contention that was underscored during Q1’s mini-tantrum episode.

And then there’s the nuance behind rate rise. It’s never as simple as saying “well, yields rose today.” Even parsing reals and breakevens isn’t straightforward. Rising real yields can be the archenemy of risk assets, but deeply negative reals don’t exactly send the “right” signal about growth. Breakevens can be a boon to the extent they’re synonymous with the reflation narrative, but inflation is becoming a source of consternation for quite a few folks.

We can look to history, if we want. “In the last 20 years equities have digested higher bond yields well and outperformed bonds,” Goldman wrote late last month. “Bond bear markets were short and shallow and falling equity risk premia buffered rising bond yields, which generally came alongside better growth but anchored inflation,” the bank’s Christian Mueller-Glissmann said, before cautioning that “before that, there were several bond bear markets when equities and bonds fell together and 60/40 portfolios had poor real returns for prolonged periods of time.”

The uncomfortable reality is that this notoriously vexing “relative attractiveness” discussion is even more exasperating now than ever. There are no “right” answers and everyone has their own model. Beauty truly is in the eye of the beholder. One man’s “opportunity” is another’s falling knife.

Toss in the fact that nobody knows what the current policy conjuncture will ultimately entail for the economy and thereby for asset prices (we’re in a “brave” new world characterized by monetary-fiscal “partnerships”) and the entire discussion becomes an exercise in abject futility.

The Biden admin is floating a total infrastructure package of $4 trillion. If it manges to get even a third of that, I’d bet the yield on the 10yr is going to break 2.0 before it falls back below 1.5. But I’ve been saying that for a while. Trade accordingly.

Good comment- and to the point. But also keep in mind, that the infrastructure part of the spending is going to be paid with higher taxes, and that the proposed infrastructure spending is mooted to take place over 8-10 years.