A quick look at the schedule for this week suggests it’ll be a noisy affair, even if the narrative is unlikely to change.

Arguably, the marquee event is Thursday’s seven-year sale. The first quarter of 2021 will be remembered for a lot of things, some of them wholly dubious. While February’s disastrous seven-year auction hardly ranks with the Capitol riots when it comes to regrettable moments in US history, it did punctuate a memorable session for rates. February 25 was the day when the global bond selloff metamorphosed into a proper tantrum. What started with fireworks in Kiwi and Aussie bonds culminated in a harrowing, chaotic day for Treasurys. The seven-year debacle was the exclamation point.

Since then, the market has digested supply relatively well, all things considered, but with SLR exclusions poised to expire and traders still on edge, this week’s $62 billion offering will be scrutinized. “Next week’s auctions will remain closely watched even as the long-duration supply has gone off relatively well in recent weeks,” TD’s Priya Misra wrote late last week, adding that traders will be keen on “any signs of market instability” even as “recent cheapening in the belly… could create some investor interest.”

Essentially, the market wants to know whether what happened last month was more a function of the circumstances that prevailed that day or whether auctions will be a source of consternation for the foreseeable future. “Since the February 2s/5s/7s supply series and specifically the weakest seven-year auction on record, much has been made about primary market sponsorship for Treasurys in the newly redefined rate environment,” BMO’s Ian Lyngen and Ben Jeffery said, noting that “at this juncture, the performance of the belly offers critical insight on the collective expectation for the path of normalization.”

That’s the context for this week’s auction slate and it’ll play out against the musings of a veritable procession of Fed speakers lined up from Monday through Thursday. On Tuesday and Wednesday, Jerome Powell and Janet Yellen will appear before the House Financial Services Committee and the Senate Banking, Housing, and Urban Affairs panel to chat about the CARES Act and pandemic relief.

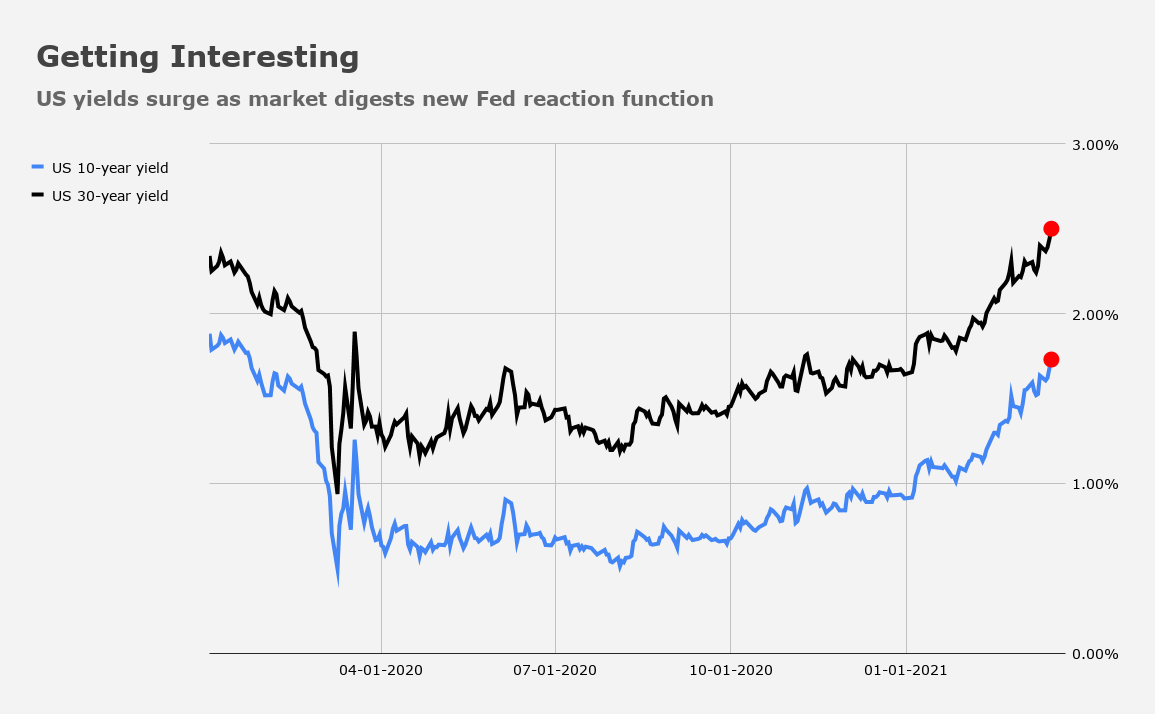

All of this as markets struggle to accept the Fed’s new reaction function, which, as Powell made clear last week, does in fact entail waiting on actual, realized inflation to manifest prior to having any substantive discussions about tightening policy.

“While Powell’s joint testimony with Yellen is related to requirements of the CARES Act, we would not be surprised if Congress were to touch on Powell’s and Yellen’s views on recent moves in Treasury yields, especially within the context of the latest decision to not extend the SLR exemption,” Deutsche Bank’s Brett Ryan and Matthew Luzzetti remarked.

The expiration of SLR relief is likely to take the blame (deservedly or not) for a portion of any addition tumult in rates. Analysts generally aren’t satisfied that the issue can be so easily dismissed as irrelevant for bonds, and everyone (including the Fed) acknowledges that reserve growth may necessitate permanent changes at some point.

Read more: ‘We Could See Volatility’: Expiration Of SLR Relief Haunts Strategists

Angst at the long-end isn’t difficult to perceive. The Bloomberg Barclays US Long Treasury Total Return Index fell into a bear market last week, its first in 40 years.

Not helping is the cacophony of pundits, legends (read: Ray Dalio) and former officials (read: Larry Summers) pounding the table on the dour outlook for bonds and the prospect of spiraling inflation.

“The combined takeaway after the FOMC is: dimensionality of uncertainty is lower – we know the Fed reaction function now – but inflation remains a hard unknown at this point,” Deutsche Bank’s Aleksandar Kocic said, adding that,

While this is a somewhat unexpected turn of events, it should not be too much of a surprise given the current difficulty in assessing the inflation path in the long run. The following chart illustrates the underlying dilemma. It shows the history of the University of Michigan inflation expectations. It clearly outlines two inflation regimes: moderate inflation during 1998–2014 with an average of around 2.9% and a lower bound at 2.7%, followed by low inflation averaging around 2.5% and an upper bound at 2.7%. We currently appear to be at the inflection point between the two inflation regimes and it is not clear whether we are probing the upper boundary of the low-inflation range or transitioning to the moderate, but higher, regime. This configuration potentially erodes confidence in any inflation forecast.

It’s hard to make predictions, folks. Especially about the future.

“Either the market is not hearing the Fed, or it believes that the Fed is wrong to dismiss the move higher in inflation but the swift movement in yields post-FOMC clearly showed the Fed’s complacency around upcoming inflation may have unintended consequences,” AxiCorp’s Stephen Innes remarked, over the weekend. “The problem for risk markets is inflation will be an ongoing debate for another six to 12 months, if not longer.”

Meanwhile, in Turkey, Recep Tayyip Erdogan’s extraordinarily ill-advised (and I cannot emphasize “ill-advised” enough) decision to fire Naci Agbal resulted in a predicable collapse in the lira. It fell more than 16% in early Asian trading.

10 yr is below break even in both the low and moderate inflation case…. to me the big driver here is supply/demand. If you’re going to lose money holding to maturity the only way to win is to sell to a bigger fool. The fed has typically been that buyer but has signaled it is not going to buy most of what’s coming down the pipe. Who’s left to be the bigger fool?