The Fed was poised to be the only game in town Wednesday, with traders and investors looking for (demanding?) answers to a bevy of questions.

It seemed unlikely all of those inquires (many of which have found expression in the bond market) would be addressed. But maybe it’s what the statement, projections, dots and Jerome Powell don’t say that’s more important.

He’s been mercilessly lampooned for the 2019 policy pivot, which critics contend showed Powell is “no different” from his predecessors when it comes to having little appetite for an equity market rout. But the circumstances were exigent. Working for Donald Trump is about as “good and easy” as a trade war. Powell hiked and let the balance sheet run off until he broke something. When you think about it, that’s as hawkish a policy bent as you can realistically ask for in the post-financial crisis world.

Read more: Until Something Breaks

Upgrades to the growth outlook were inevitable but all eyes were on the inflation projections and, of course, the dots. Powell would surely rather just let the market push yields up than intervene at this juncture, but it hangs on any extension of the bond selloff being “orderly.”

“While markets [were] quiet ahead of the event risk with US yields trading within recent ranges, the Fed will move bond markets [Wednesday], whether it wants to or not,” Bloomberg’s Laura Cooper wrote. “Which direction isn’t clear, but that green light for higher yields is unlikely to turn yellow just yet.”

“Market pricing is much more aggressive than the dots imply. Will the March version of the SEP run counter to Chair Powell’s assertion that the Fed is ‘not even thinking about thinking about raising rates?’,” BNY Mellon’s John Velis wondered. “Even if they see a much brighter economic scenario now than they did in September, Powell will be walking a fine line between acknowledging the rosier outlook and reiterating that policy will stay loose.”

That’s always the balancing act. Even in better (i.e., less pestilent) times. The key is to express optimism without being hawkish. And to express enough pessimism to give yourself plausible deniability when it comes to retaining an accommodative policy stance without being so pessimistic that anyone gets spooked. That latter proposition isn’t as much of an issue in 2021. It was difficult to imagine a scenario where Powell expressed “too much” caution.

“The most excitement might be driven by what Powell doesn’t say; off limit topics will include accelerating liftoff, worries about losing grip on inflation, and any need to taper prior to 2022,” BMO’s Ian Lyngen and Ben Jeffery said, adding that “while the Chair’s reluctance to directly express these concerns won’t prevent the press from asking and the market from parsing the response, it’s simply far too early for policymakers to signal that the improving economic prospects will translate through to a less accommodative stance in the near term.”

The table, below, from TD is a handy decision day guide.

Central bankers have spent the last decade begging for help from fiscal policy. Now they have it. And then some in the US. That’s a relief to the extent it takes some pressure off monetary policy for sustaining the recovery, but it gives critics ammunition when it comes to insisting that the combination of big spending and a Fed that’s openly countenancing an inflation overshoot is a recipe for… well, for an inflation overshoot.

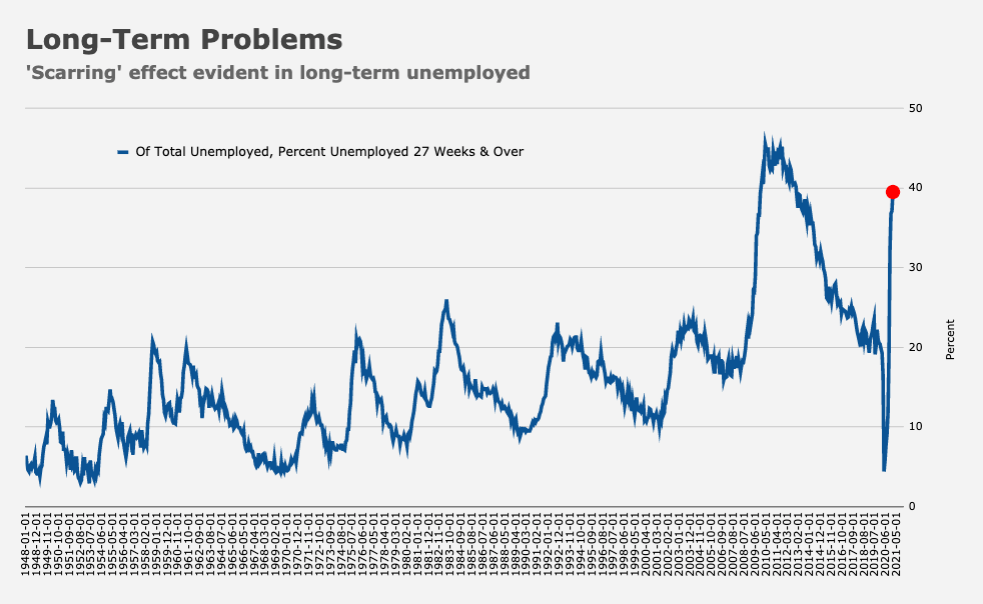

Powell will surely follow Janet Yellen’s lead (in her role as Treasury Secretary I mean) in reiterating that the biggest risk to the US economy isn’t hyperinflation, or even uncomfortable inflation, but rather the structural damage from a labor market that’s still almost 10 million jobs short of pre-pandemic levels. The dreaded “scarring” effect is already visible (figure below).

Price pressures are evident in PMIs and base effects mean the data will start to get noisy soon. At the same time, the arrival of new “stimmy” in bank accounts across the country likely presages at least a few more inflated retail sales prints, even as February’s report underwhelmed.

In my mind, too many people assume things work like they used to work or, perhaps more aptly, that things used to work the way people assumed they did. Those assumptions are faulty. No one knows much about economics. It’s a soft science and hinges on human behavior which, in turn, means the “rules” can change depending on how people act.

If you’ve ever had to teach from a soft sciences textbook, you know it’s often preferable to just scrap those $250 paperweights in favor of an eclectic mix of paperbacks. Students don’t buy the latest (i.e., “updated”) edition of the textbooks anyway, and even if they did, what hope does any economics textbook have of staying current in today’s world? With few exceptions, everything we’ve ever thought we’ve known about economics with something like certainty has turned out to be some semblance of spurious. Being wrong more often than right when it comes to economics is not the sole purview of central bankers, nor is it a phenomenon that’s confined to economists. How many traders do you know who are right more often than they’re wrong? If you find one who makes that claim, let me know and I’ll point you to a lier.

“It’s all about the Fed, and if they display any sign at all of shifting the dot plot… especially given the possibility [2023] will be a period following not just the $1.9 trillion stimulus package, but a $2.0-2.5 trillion infrastructure bill too, in which case one would suppose the underlying pressure for higher rates would be strong,” Rabobank’s Michael Every wrote Wednesday, before adding a caveat: “If things still work the way the textbook says they are supposed to re: liquidity > investment > wages > inflation. Which they clearly don’t right now.”

If by some miracle we see the Dem’s take out the filibuster and pass voting rights then perhaps there is a chance… a very small chance that we see them move on to a huge infrastructure bill and after that maybe… just maybe they take action against corporate wage fixing. Until then wages will basically never go up meaningfully except at the minimum level occasionally and the maximum levels regularly.

The dovish case in td’s table has no mention of SLR, WAM, twist, or any other form of ycc. Would it be a red light or even yellow for rate rises without Powell putting his money where his mouth is?

Maybe I’ll eat my words, who knows.

Because WAM and twist aren’t on the table right now. There was zero chance of those being announced at the March meeting. Powell will obviously allude to WAM but an official announcement on Wednesday would be a massive dovish surprise — effectively that’s just a right tail risk.

On SLR, Zoltan effectively said it doesn’t matter on Tuesday evening. So, apparently, that’s a non-issue regardless if you take his word as gospel, which it kinda is considering where he’s probably getting his information.

Understood. My point is that i’m skeptical that fed jawboning will be considered dovish enough for a bull flattener if all we’re talking about is withholding hawkish moves without mention of fresh dovish ones.

Work from home is here to stay (deflationary).

Going out to a restaurant that has tight, indoor only seating sounds unappetizing.

I do not know anyone making big travel plans, especially outside the US, because “Yeh! Covid is over!”

Most resumed travel plans seem to be “low-key” catching up on visiting friends and family, not “let’s go to Europe or to a big US city, stay in a crowded hotel, go out to over-eat in packed, but charming, restaurants, go to museums and/or sit in other crowded indoor venues with unknown homo sapiens who are potentially carrying a variant of covid that my (still hoping to get soon) vaccine may or may not protect me from.

How effective is the regular flu vaccine, again?

On top of that, some people, who did not lose their jobs during covid, got to experience what it is like not to spend everything they make and have some savings/cushion. Definitely, stress reducing – so unlikely that spending fully ramps up and credit cards are “ re-loaded”….at least for awhile.