Markets started the week in “what now?” mode, as traders nervously eyed bond yields for signs that the storm has passed or else that the worst may be yet to come.

The earliest action hinted at some respite, as Australian yields plunged after last week’s harrowing (and I do mean harrowing) surge. You’re reminded that Thursday’s dramatics stateside were presaged by similarly erratic moves in Aussie and Kiwi bonds.

“The Fed has largely shrugged off the recent moves in yields, viewing the rise in rates as reflecting a more positive growth outlook [and] this week will be the last opportunity for officials to shift their tone, given the upcoming blackout period ahead of the March FOMC,” AxiCorp’s Stephen Innes said over the weekend. “So it’s a big week on the pushback front.”

It is indeed. The Fed is the odd one out. Officials abroad have already pushed back. The RBA stepped in with unscheduled bond-buying (which met with mixed results), there were rumblings out of Japanese officials, and Isabel Schnabel effectively threatened to execute (figuratively) overzealous “vigilantes.”

“We can expect all the usual suspects to have to put their mouths where their money is: That is verbally (for sure) and financially (quite likely?) show the longer end of the curve that they are still in control,” Rabobank’s Michael Every remarked.

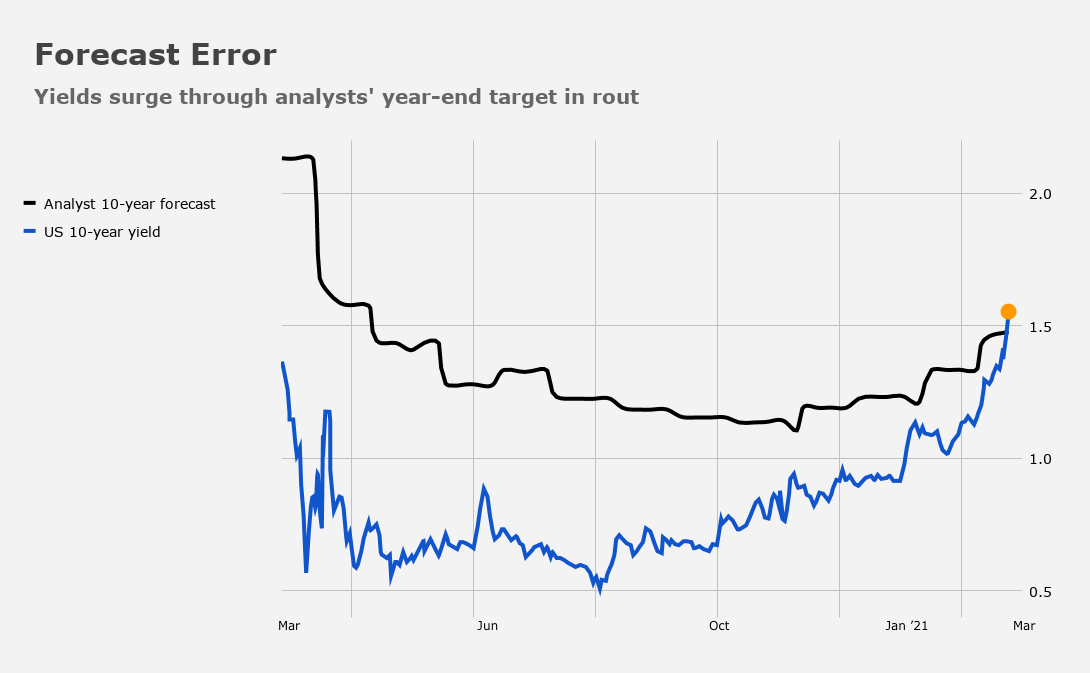

US yields pushed through analysts’ year-end target last week during the worst of the selloff. Even after Friday’s rally, yields were still perched right around where strategists’ projections stood coming into the week. The orange dot in the figure (below) denotes last week’s peak.

More good news on the vaccine front presumably means the US can reach something like herd immunity faster. Anthony Fauci on Sunday cautioned Americans against the tendency to eschew the newly approved Johnson & Johnson shot in favor of waiting on an ostensibly more efficacious dose from Pfizer or Moderna.

“If I were not vaccinated now and I had a choice of getting a J&J vaccine now or waiting for another vaccine, I would take whatever vaccine would be available to me quickly,” Fauci said. “We want to get as many people vaccinated as quickly and expeditiously as possible.”

Total global cases are near 114 million. Some 230 million shots have been administered.

I suppose it’s at least encouraging that Americans’ views towards vaccination have shifted from widespread skepticism (last year) to vaccine shopping. It also says something about the perks of living in a rich nation — eventually, one assumes Americans will be able to choose among vaccines like they can among cereals or ice cream flavors.

Anyway, data out of China over the weekend showed activity decelerated in February, but analysts cautioned that investors shouldn’t read too much into the numbers, which were subject to seasonal distortions and affected by localized virus outbreaks earlier in the year. The official manufacturing PMI fell to a nine-month low, while the non-manufacturing gauge missed estimates, printing just 51.4, down markedly from post-pandemic highs. Caixin manufacturing missed too.

“The declines in the past two months, in particular, indicated that the series of local outbreaks at the turn of the year did dampen the overall economic momentum, in particular on the service sector,” SocGen’s Wei Yao and Michelle Lam remarked Sunday. “However, the expectation readings for both rebounded [while] several other business surveys and a few high-frequency data also suggest that corporates started to restore confidence and economic activity began to pick up again in late February, as all the local outbreaks were quickly contained,” they added.

Oh, and it’s probably worth keeping an eye on your emerging market equities. Last week was the worst week since the onset of the pandemic for developing nation shares.

Clearly, further rate rise in the US and especially any accompanying dollar strength would be an unwelcome development.

Jerome Powell hasn’t always been what one might call “attentive” to the risks for emerging markets of rising US yields and expectations of tighter policy. Of course, the Fed insists it has no plans to tighten whereas, in 2018, when tone deaf remarks from Powell during the early days of his tenure as Chair exacerbated a burgeoning EM meltdown, the Fed was actively turning the screws.

Who is the marginal buyer of the long end? Issuance is set to drastically outpace fed purchases this year. And with inflation expectations high, and likely increasing it would seem suicidal to buy and hold…

Will the fed institute a harder ycc or step up their purchases if they aren’t forced into it?

TGA has $1.5T (WTREGEN) and the (potential) stimulus will cost $1.9T, spread over time. Taxes should start coming in over the next two months. The Fed is still buying bonds. Why will “Issuance … drastically outpace fed purchases” in Q1 and Q2? High inflation by 2024? Doubtful IMHO.

You mentioned q1/q2 not me.

Cbo has a 2.3 T deficit for the year before the stimulus to say nothing of a potential infrastructure bill (or student loans). Fed purchasing an annualized 1T give or take. In my opinion, participants looking for the door aren’t going to wait for things to get truly dicey.