A while back — and I endeavored to find the relevant articles Friday morning, but gave up after spending an inordinate amount of my espresso/cigar time rifling through my own digital archives — I flagged some commentary from Nomura’s Charlie McElligott, who suggested that if you were looking for canaries (the ones consigned to coal mines), one candidate was tail hedgers moving into bear flatteners.

Why would one do that? Well, it’s not complicated. If you were in bear steepeners, you were playing some combination of the reflation narrative, reopening optimism, vaccine rollout, and/or the “blue wave,” with the latter presaging more stimulus. All of those macro themes argued for higher long-end yields and, with the Fed pinning the short-end, a steeper curve.

Those themes ended up playing out, with the Georgia runoffs serving as the final piece of the puzzle. Breakevens eventually pushed to multi-year wides, the curve erased years of flattening, small-caps staged an epic rally, commodities exploded higher, and so on.

Of course, all of that is inflationary, and when considered in conjunction with the Fed’s explicit pledge to countenance overshoots in order to make up for past shortfalls (and simultaneous adoption of a tweaked labor market mandate that suggested the traditional concept of “full employment” had been relegated to the dustbin of history in favor of a more literal definition of “full”), some argued that policymakers would find themselves behind the curve rather quickly.

That view — that the Fed is underestimating the chances of a sharp rise in realized inflation — is now almost mainstream, if you count Larry Summers and Paul Singer as “mainstream.”

But before Singer was fretting about it on podcasts and prior to Summers dedicating seemingly all of his spare time to maligning Joe Biden’s stimulus plan, some folks were anticipating an early Fed shift via bets on bear flattening.

McElligott reminded folks about this in a Friday note which doubled as a kind of postmortem re: Thursday’s rates drama.

“Since late last year/start 2021, what were tail funds moving into?,” he asked. It was a rhetorical question.

“They had more recently been loading into bear flatteners, with the front-end/intermediate space the most likely repricing points and coming unpinned from policy adjustment,” he added, noting that these tail hedgers were simply “playing for a scenario where the market anticipated the Fed needing to tighten far ahead of schedule, and they would do that via tapering of QE, which would disproportionately impact the belly of the UST curve.”

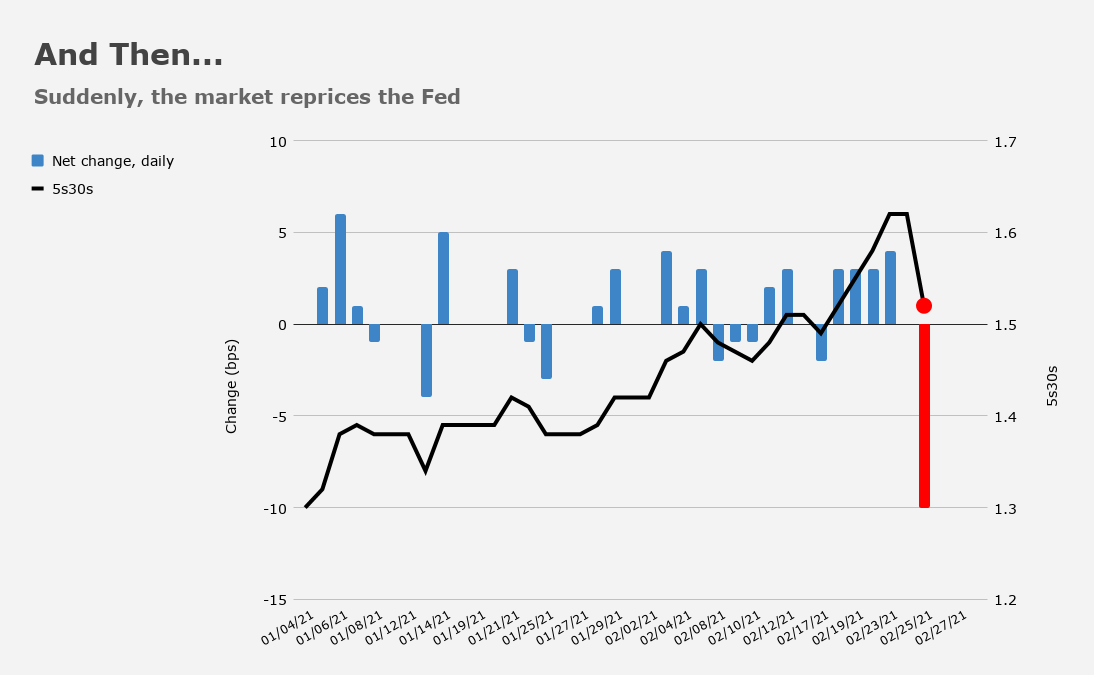

That pivot — tail hedgers moving from bear steepeners to bear flatteners — looked pretty prescient on Thursday. I won’t spend time trying to offer anything like precision when it comes to illustration. Rather, I’d just note the obvious — the 5s30s bear flattened dramatically amid the chaos.

But it wasn’t just tail hedges in bear flatteners that tipped a reckoning. On Friday, McElligott ran through a list of canaries.

There was “the massive jump in Green ED$ (2023) open interest to a level that incredibly surpassed the OI of Reds (2022), and all into a down move, meaning highly indicative of new short positions being established,” he said, adding that “even more incredible is the March ’23 contract which sits as the highest open interest contract across the entire Eurodollar futures board,” a development he called “stunning.” “One would almost always assume that highest OI would be in Whites or at worst, Reds,” he added.

Charlie also mentioned some lackluster metrics from the most recent five-year sale which he said presaged Thursday’s seven-year disaster. If you were asked to use the word “debacle” in a sentence and the sentence had to be market-related, you could scarcely conjure a more apt example than this week’s seven-year auction.

In addition, McElligott noted that CTA signals had flipped short in global bond futures recently. The figure (below) is a somewhat crude way to visualize things, but it’s amenable to a wide audience, so it’ll work.

The knock-on effect for equities was predictable. Duration risk is embedded across markets, and it’s safe to say the vast majority of investors don’t understand the link between their holdings of tech shares/secular growth favorites and bonds/the curve.

“We still [have] so much legacy positioning crowded into equities with heavy interest-rate sensitivity,” McElligott remarked on Friday.

Whether this week’s fireworks are enough to compel the Fed to be more forceful in the messaging or otherwise echo the ECB’s Schnabel in explicitly stating that past a certain point, the risk from rapidly rising yields is more important than whether or not the backup is tied to expectations of better economic outcomes, remains to be seen.

“We’ve long maintained that the Fed will be content with an orderly backup in yields unless and until ‘something breaks,'” BMO’s Ian Lyngen and Ben Jeffery said. “The debate is now whether or not the -3.5% Nasdaq drop and -2.5% S&P 500 retracement will be sufficient to leave Powell concerned the worst is yet to come.”

You must be logged in to post a comment.