The “memes” are back.

GameStop and other manifestations of last month’s Reddit mania started grabbing headlines again late Wednesday, and it looks as though market participants may be subjected to another several days of distraction, courtesy of erratic (and wholly ridiculous) moves in some of the names associated with the WallStreetBets crowd.

Hopefully, this doesn’t get so far afield that it sucks the energy out of the room. The new narrative in GameStop (on the off chance you aren’t apprised) is that the company’s decision to force out its CFO bodes well for a presumptive turnaround. One possibility — and this is just as real as it is ridiculous — is that activist investor Ryan Cohen, a board member, sparked the latest surge by tweeting a picture of a McDonald’s ice cream cone with a frog emoji. “Does it signal Cohen will fix the company the way McDonald’s finally fixed its ice cream machines?,” someone wondered.

The figure (above) includes both after hours trading from Wednesday and pre-market action Thursday. I suppose one congressional hearing wasn’t enough. Obviously, this kind of thing isn’t desirable. There is no sense in which one can make a fundamental case for GameStop at $200, and the price action clearly indicates a collective effort to push it higher. Other names associated with the Reddit universe were similarly charged up.

How this plays out in regular trading and in subsequent days really isn’t the point. I wanted to capture this moment for posterity, because what you see in the visual (above) shouldn’t be happening. It’s not about exercising some kind of ostensibly benign, but overtly condescending, paternalism in order to “save retail investors from themselves.” It’s about market integrity.

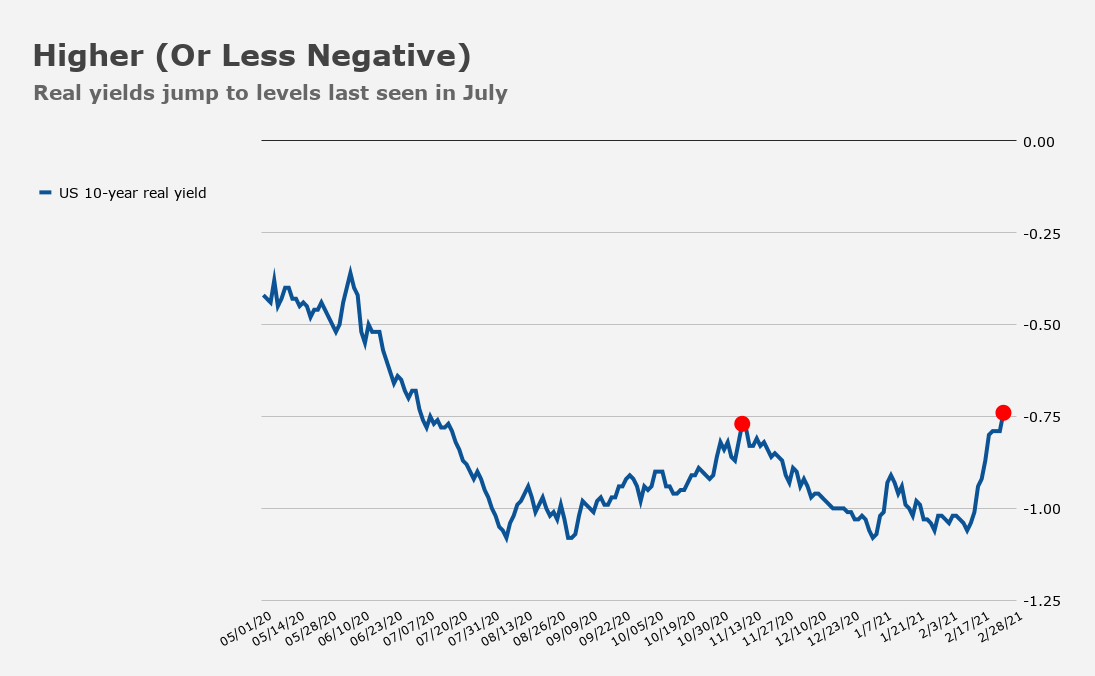

Moving swiftly to things that matter, 10-year US real yields rose to -0.7352% on Thursday. That’s notable, as it’s a breach of the “highs” hit just after the election (the scare quotes are there to acknowledge that -74bps is still deeply negative and indicative of the kind of accommodation that’s supported dot-com-era multiples for US equities, among other distortions).

If you plot real yields with the S&P’s forward multiple (chart below), you quickly understand why this is potentially concerning. On one hand, optimists will continue to suggest that rising yields (whatever the composition) are indicative of a market that sees a brighter economic future. And that’s true. But they can tighten financial conditions and if higher yields feed through to a stronger dollar, sand gets tossed into the gears of global trade and commerce which are trying to recover from the pandemic shock.

Clearly, the Fed will be keen to tamp down any rate rise that threatens to choke off the recovery (both at home and abroad) and the dollar is still back-footed, so this isn’t anything to get bent out of shape about — yet. But as US reals rise, so too does the opportunity cost of doing something other than investing in risk-free US Treasurys. In the case of negative real rates, that opportunity cost becomes less punitive.

This comes amid a global bond selloff that saw the Aussie 10-year slide Thursday. Yields rose as much as 12bps as traders nitpicked the composition of the RBA’s yield-curve control purchases. Yields were up sharply in New Zealand too. “RBNZ-dated OIS swap rates priced in a hike by July 2022,” Bloomberg’s Stephen Spratt wrote, recapping Thursday’s action. “Markets dialed up expectations that the RBNZ may be forced to tighten more aggressively to cool housing markets, following the government’s decision to add that to its remit on March 1.” A lackluster bond sale exacerbated the situation.

“Admittedly, Australian monetary policy doesn’t typically define the global rates complex, so we’re reluctant to conclude this was more than the latest evidence of bearish investor sentiment toward sovereign bonds as optimism runs high that the post-pandemic world will soon be a reality,” BMO’s Ian Lyngen remarked.

That likely comes across as terribly dry or otherwise esoteric for US investors who would rather be watching… I don’t know, GameStop, but the regional rout described by Spratt had ramifications for Treasurys, which in turn feeds into stretched valuations stateside. It’s all connected, folks. Or didn’t you hear? The Aussie, meanwhile, rose through 80 cents.

SocGen’s Kit Juckes tied this all together rather nicely. “In the last month, US 10-year yields have risen by 40bp, but the Australian and New Zealand dollars, and sterling, have still gained more than 3% against the dollar and most major equity indices are higher,” he wrote Thursday.

“Other markets, in short, can live with a move higher in US yields from very low to slightly less low,” he added, noting that “we will continue to navigate the way yields rise, with big lurches upwards hurting risk sentiment; but until they’re a lot higher than this, I still think the dollar will sell off more when yields have found a new temporary range than it rallies when yields are rising sharply.”

There’s your bull case for risk assets (risk-sensitive FX inclusive) in a world where US yields keep grinding higher.

Should we not hold short sellers to account for taking on a bad position to begin with. One that may end up being exposed to the hoards who have identified the lack of DD or gross negligence of the short seller. Should we not protect the market from this action at it’s origin, the improper short. That would eliminate the GME type action.

It has been my fear that short sellers are a big influence behind pump and dump schemes. Where they short a company beyond what they know is unreasonable from a DD perspective, and do so in order to buy the cheap shares in what is then considered a value asset. That is until they rinse and repeat.

I learned my lessons long ago in biotech where the short action included false and misleading “hit pieces” that had a dramatic affect on the price. The short scheme predates on the long and arduous process of getting medicines approved when combined with the high fail rates of potential products. Some of these companies have made it through and produced viable beneficial products for their fellow man, but not before enriching unscrupulous shorts lining the valley along the with the big guns mowing down “weak” investors on the journey. Drug development takes a long time and is a very risky for small cap companies. In many cases the short position is valid, in others it is mostly contrived and detrimental.

Shorts deserve their place as scrutinizers of publicly traded companies, however some of them need scrutiny and perhaps prison in their own right.

I do not willingly participate in retail trading. A large social media presence is a large negative for a stock under my consideration and I own very few individual stocks to begin with. Just my perspective.