What can we say about the week that was?

Well, we can say yields rose. In fact, they rose quite a bit. 10s were near 1.35% on Friday afternoon, with yields cheaper by nearly 6bps out the curve.

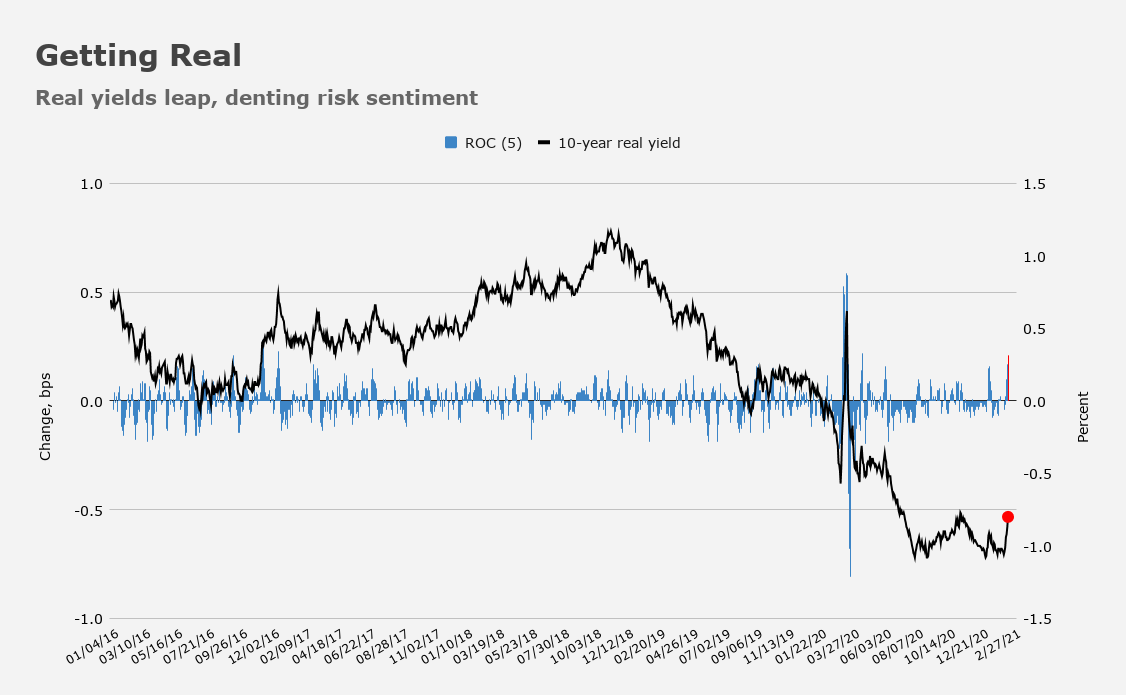

This was the week when rate rise seemed to give equities pause. Character matters. In this case, the character of the bond selloff. 10-year reals jumped ~20bps over just a handful of sessions. That’s the most since the manic days of last March and before that, the most since the 2016 election.

“One troubling characteristic of the last several days of selling in the Treasury market is the divergence with market-based inflation expectations,” BMO’s Ian Lyngen said Friday. “10-year breakevens fell 11bp over the week, while 10-year nominal yields increased 14bp,” he added. “For context, that’s effectively a quarter point hike in real rates.”

Indeed it is. And that’s why risk assets are starting to notice. Shiny yellow paperweights noticed too. If you’re interested to know why gold is having such a rough time lately, real yields are a good place to start. As Bloomberg’s Cameron Crise observed Friday, “30-year TIPS are above zero for the first time since early June.” He offered a sarcastic note of congratulations. “Fixed-income investors of the world, rejoice! You can now beat (reported) inflation!,” he exclaimed. I’m not a big fan of Crise, but he’s smart. And he can write. Those are admirable qualities.

Again, this is part and parcel of gold’s lackluster performance. Whether investors increasingly prefer Bitcoin as an “alternative” is a good question to ask, but during weeks like this one, it’s probably secondary. You’re not likely to get much in the way of performance out of gold if real yields are rising rapidly, with the possible exception of periods during which rising real rates trigger enough in the way of risk-off sentiment to catalyze a safe-haven bid for gold. That clearly wasn’t the case this week.

We’ve yet to see any kind of dramatic selloff in stocks that would indicate equities have truly “had it” (so to speak) with higher yields. It wasn’t the greatest four days, but it hardly counted as a rout. Small-caps had a rousing Friday, but it wasn’t enough to save the holiday-shortened week. The Russell still posted a small decline.

“The ramifications of [rising real rates] on risk assets have yet to follow the traditional pattern of constraining optimism and upside,” BMO’s Lyngen went on to say, noting that “this can partially be attributed to growing expectations that a fresh injection of fiscal stimulus is just around the corner.”

For what it’s worth — which isn’t much considering it’s just an exercise in marking-to-policy-reality — JPMorgan upped their estimate for US stimulus. The bank’s Michael Feroli now sees $1.7 trillion as the likely price tag for the next fiscal package, up from $900 billion previously.

“After a soft end to 2020, the economy appears to have shrugged off the latest wave of COVID-19 case counts which are now rapidly declining,” Feroli wrote. “This week’s upside surprise on January retail sales leaves real consumer spending tracking around 5.0% annualized growth this quarter,” he went on to say. Spending “may stumble in February,” JPMorgan reckons, “partly due to weather conditions across the country,” but thereafter, the bank “expect[s] the stimulus package will support a rebound as early as March.”

Some have suggested that the blockbuster retail sales print which greeted markets on Wednesday presaged a sharp uptick in inflation once the next stimulus package is signed, sealed, and delivered. We’ll see.

Read more: Markets Just Witnessed An ‘Absolute Game-Changer,’ One Bank Says

Meanwhile, earnings have generally come in better than expected. I talked about that at length last weekend, but another interesting factoid comes from Bespoke Partners, whose data showed that some 14% of S&P 500 companies beat on the top and bottom lines, and raised guidance.

I suppose I’d be remiss not to mention Bitcoin (again). Its “market value” hit $1 trillion this week.

That’s $1 trillion worth of… I don’t know. $1 trillion worth of something. It’s up to you to decide what. And also whether you want to spend ~$55,000 on one of whatever you decide it is.

I’ll give the last word to SocGen’s Subadra Rajappa. “Ultimately, the ups and downs of COVID should dictate where we end up, and the risks may be more symmetrical than they look,” she said, in the bank’s weekly fixed income wrap, adding that if “risky assets react negatively to the rise in real yields, the feedback loop from any selloff in equities or credit will likely bring investors back to the safety of Treasurys, acting as an equalizer.

The question- what level of rates causes the $ to rally and cracks the financial markets- and how fast does the move have to be?

Re: 2013

Which broke this camel’s back; and firmed the resolve to find greener pastures that were not in the USA anymore.

Jawboning the 10 year yield is fine, but looking back at any 10-year spread for the last 50 years — it seems like this recent pop back to normalization in the rate curve is a knee-jerk covid response which will fade away in a matter of months. With the way all markets are freaking out, Treasury yields obviously may have sustained madness and not fall into a previous or prior normal range — but a huge upward spike from here seems unrealistic.

With that said, the lower range will apparently head to zero and widen the spreads to historic levels in a few months. Apparently the debt plumbing will encounter a Fed deficit ceiling issue soon, related to servicing debt — but, apparently that won’t be a long lasting trend, but more of a mini shock or wobble. In any case, lower end rates will most likely remain low and stagnate. However, as collateral becomes more expensive with short term stuff, that could get weird.

From what I can tell, servicing the debt isn’t going to be a problem (anywhere) and all the Fed balance sheet fears also don’t matter and it’s doubtful hyper inflation will ever be an issue or realistic concern.

Thus, there is drama on the horizon but it actually looks like growth ahead, so any slight uptick in yields may actually be a tap on the brakes during this winter storm. The pandemic will also cool things off a bit, because in case anyone isn’t paying attention, it’s still very active and very deadly — and the vaccine race isn’t really going that well. It also isn’t helpful to have a a more virulent virus spreading while tens of millions ignore it and the vaccine — that’s not a smart combination!

Here’s a weird FRED chart, basically playing with the 10-yr 2-yr spread and 3 month yield. This suggests to me that things are not great but more than likely going to be fine:

https://fred.stlouisfed.org/graph/?g=Bfdp