In a Bloomberg Opinion piece this week, Nir Kaissar wrote that “GameStop’s stock [isn’t] unusually disconnected from the company’s underlying business, as many people wringing their hands about market efficiency have suggested.”

I’m not “wringing my hands” about market efficiency. Markets aren’t always efficient. Everyone knows that. You shouldn’t wring your hands about it. It’s what creates opportunity. Arguably, we don’t want 100% efficient markets. We want markets that are almost always efficient. That way, we can capitalize off rare inefficiencies which we can safely assume will correct themselves once enough people become aware of them. Sometimes, they (the inefficiencies) can persist for months or even years, which can be annoying (and quite costly), but the assumption is that they can’t persist forever.

In many respects, GameStop fits that description. There was an inefficiency (short interest was more than 100% of the float, which is rare), and a group of people exploited it for huge profits (assuming those gains were booked). They were helped along in the effort by social media and the collective realization that dealers could be forcibly enlisted in the Reddit-fueled offensive.

The subsequent rally was nothing short of ridiculous. So ridiculous, in fact, that congressional hearings into the matter are in the offing.

That rally created a huge asymmetric opportunity on the downside, which was itself quickly exploited, bringing the shares crashing back to Earth. In my opinion, there’s probably still another 50% downside (at least) from Friday’s closing levels, before this fiasco finally settles at some kind of sustainable “equilibrium.”

The stock fell 80% last week. At the height of the insanity, GameStop was valued at $33.7 billion. By Friday afternoon, that beer-goggles figure was around $4.5 billion.

In the opinion piece referenced above, Kaissar attempted to solder what he claimed are concerns about market efficiency to a contention that GameStop’s price isn’t “disconnected from the company’s underlying business.”

There are a couple of problems with that. First, the fact that a lot of listed companies lose money (which appeared to be Kaissar’s primary justification for the claim that GameStop’s shares weren’t “unusually disconnected” from GameStop the underlying business) is an exercise in question-begging. Essentially, Kaissar said that GameStop isn’t “unusually disconnected” from the fundamentals, because lots of stocks are similarly disconnected, including GameStop.

“GameStop hasn’t turned a profit since 2018, but it’s hardly alone,” he wrote. “About a third of the companies in the Russell 3000 lose money.”

By that logic, a female corporate executive making 75% of what a man doing the same job makes, isn’t “underpaid,” because she’s “hardly alone” — most women doing the same jobs as men aren’t paid commensurately.

Kaissar brought along some math to make his point. He wrote that,

Of the roughly 2,300 companies in the [Russell 3000] for which a price-to-cash flow ratio can be calculated, 386 of them have a higher ratio than GameStop. And of the roughly 2,800 companies for which a price-to-sales ratio is available, more than 2,100 have a higher ratio than GameStop.

One obvious question is this: What price was Kaissar using? The opinion piece was dated February 5. Did he use $483 (GameStop’s high)? Or did he use the previous day’s close, around $53?

I don’t know. And I don’t care. That argument is just another manifestation of “it’s all relative.” But even in a market where such arguments are heard frequently (e.g., citing low bond yields to justify sky-high multiples on some US equities), it stretches the limits of what rational people can process in the context Kaissar used it.

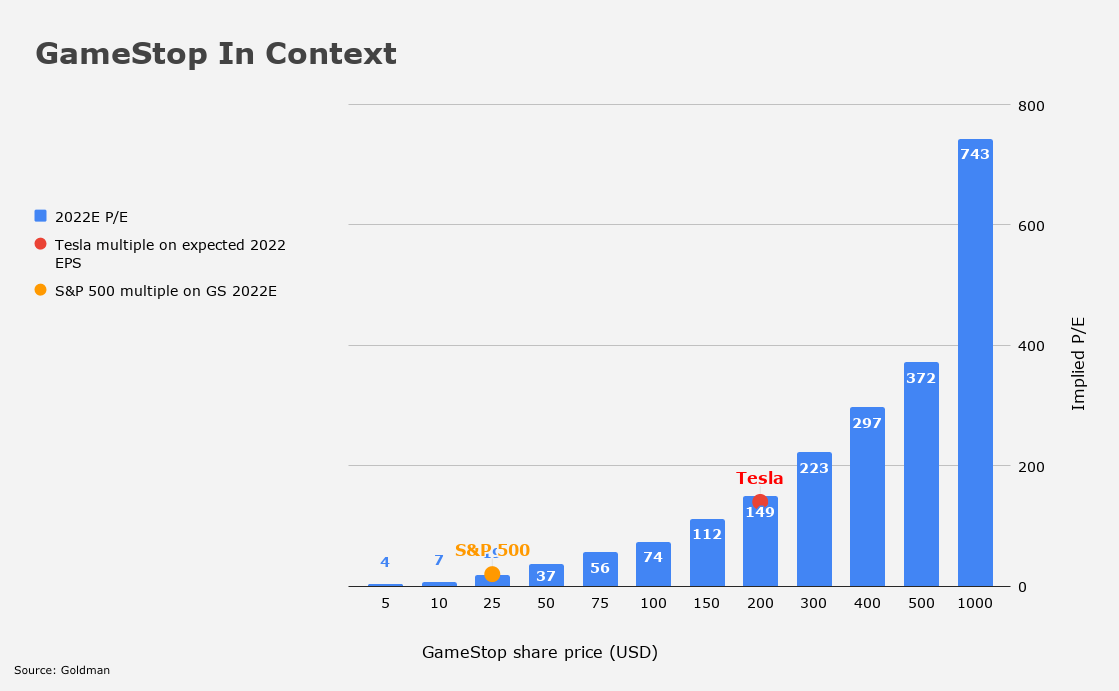

For example, Goldman’s David Kostin did some quick math on this in a Friday evening note. “The absurdity of the January spike in GME share price becomes readily apparent when viewed through the lens of implied valuation,” he said, adding that “the implied P/E on projected 2022 EPS two years into the future soared from 14X at year-end 2020 to more than 250X at the peak on January 27, before retreating to the current P/E of 42X.”

So, to reiterate, GameStop was trading at 250X projected 2022 earnings on January 27. At its peak, the following morning, GameStop traded at nearly 370X, based on data presented in a table attached to the same cited Goldman note. Had it gone to 1,000, the forward multiple would have been more than 700.

“For context, shares of Tesla, a stock that has both skeptics and cheerleaders around its valuation, but is widely viewed to have strong growth prospects trades at 140X expected 2022 EPS following its stunning 780% rise last year,” Kostin went on to remark.

Goldman channels Oscar Wilde. “We could be wrong and in Wilde’s terminology be sentimentalists clinging to a nostalgic belief that valuation always matters,” Kostin said, before delivering the following assessment of the situation:

Stated alternatively, perhaps we are only seeing the absurd recent valuation and not recognizing the potential future market price of the shares. While some investors argue a bull case for GME shares through a re-positioning of the company for the digital era, the stock’s 1,600% gain in January appears to imply such a transformation would be seamless and immediate. Management could achieve its goal of accelerating sales and earnings and the shares could respond accordingly. However, experience suggests firm makeovers typically take time and most investors are cynics until convinced otherwise.

A cynic famously “knows the price of everything, and the value of nothing.” For now, the P/E column for GameStop contains this placeholder: “NM.”

To date- this craziness really does seem to be the intersection of where gambling and investing intersect. Also, those who were traditionally classified as “investors” might have been acting more as “gamblers” and vice versa.

However, right now GME’s greatest asset is its stock price and if that could be used as currency ( such as Henry Singleton did with Teledyne) there could be a path that makes sense from an investment standpoint.

For what it is worth, this is not my type of investing.

Also, I think the story of Teledyne- both during the time period that they issued stock for purchase of companies and that they retired their stock is one of the more interesting stories about capital allocation.

I’m somewhat curious as to why there would be a congressional hearing into the Gamestop craziness. Since some of these congressmen have sold their souls to the big money interests would they be trying to figure out how to profit from future craziness?