I’m not sure I’d call it a “dip,” but everything is relative in a world where, barring pandemics and self-inflicted wounds (e.g., pushing US real rates beyond 1% and then saying the words “long,” “way,” “from,” and “neutral” in that order, out loud, around people with working ears), benchmarks only go up.

But proper “dip” or not, consider it bought. Whatever “it” was.

US equities had their best week since November, just a week on from their worst week since October.

To say small-caps had a “good” week would be an understatement. But almost everything was generally buoyant. Last week everyone held their breath. This week was the exhale.

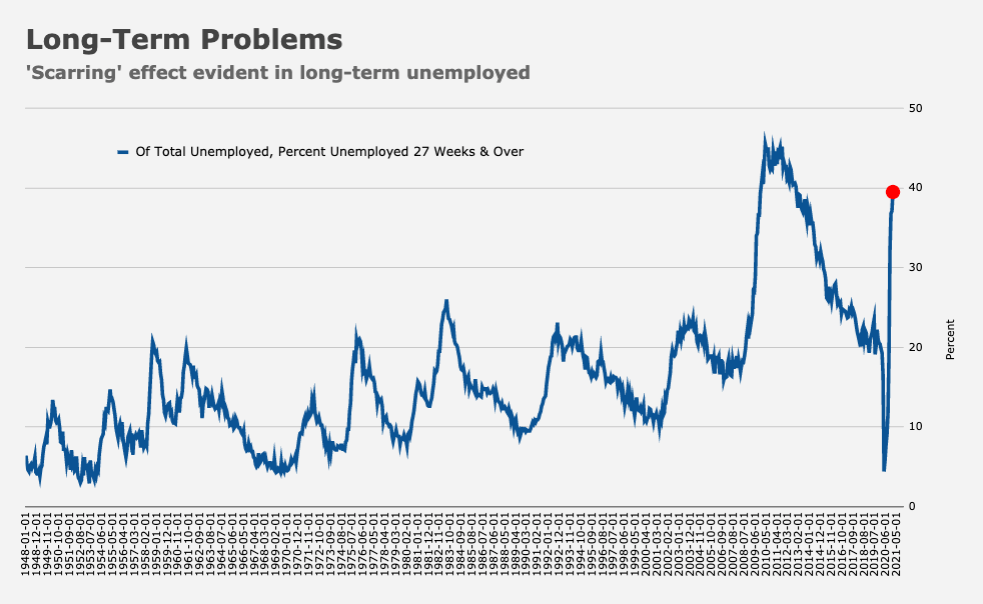

Friday brought bad news on the labor market front. The January jobs report was a disappointment. The headline missed. Revisions were negative. Leisure and hospitality didn’t recover. The percentage of those unemployed for 27 weeks or longer rose to near 40% (visual below). And so on. Take a few minutes to look under the hood.

But, as circumstances would have it, the lackluster payrolls report lined up with Democrats moving ahead without Republicans on stimulus. Kamala Harris was the star on Friday.

The GOP’s case for doing less was undercut by the disappointing jobs report. Joe Biden took the opportunity to insist that going big now is paramount.

That, in turn, effectively muted any bid Treasurys might have otherwise enjoyed from a dour read on the labor market. Yields were cheaper by 4bps out the curve, which steepened. 10-year yields rose as high as 1.19% before retreating a bit. Note that Brent climbed near $60 on Friday. Consider that with 10-year breakevens at ~2.17% and the 5s30s the steepest since 2015.

Commenting Friday on their rangebound thesis for 10-year yields, BMO’s Ian Lyngen and Ben Jeffery wrote that any call for 10s to center “closer to 1.0% than 1.25%” implicitly assumes there’s scope for yields to “spend at least a portion of 2021 with a 0-handle.”

Not implausible, to be sure. After all, the pandemic effects on the economy are still evident and vaccine rollout still poses a monumental logistical challenge, recent progress (figure below) notwithstanding.

And yet, Lyngen and Jeffery went on to say that “the largest contributor to our sleepless nights is the risk that 1.0% functions as a floor for 10-year yields rather than a midpoint.” They argue that without the concession that invariably accompanies expectations for massive issuance, yields would be biased towards falling to 1% on data like Friday’s NFP report.

But there’s still some concern out there that between supply and upside risks to inflation, the scope for yields to rise more quickly than many market participants expect is perhaps larger than assumed. In any event, the weekly chart (below) gives you the 30,000-foot view.

“Markets are looking for reasons to take more risk,” SocGen’s rates team remarked, in their weekly piece. “The GameStop saga came to an end and hopes that vaccines will work resurfaced,” the bank’s Adam Kurpiel and Subadra Rajappa said. “In the meantime, more relief money could feed the supply frenzy on both sides of the Atlantic, adding to the long-end steepening trend.”

That’s a pretty concise summary. The dollar rose a second week, but Friday’s slide made the weekly move look fairly pedestrian. It was not a good week for gold, which dropped nearly 2%.

“February equals US fiscal easing month, vaccine > virus and reopening > lockdown plays,” BofA said Thursday, adding that volatility may return in March.

It was an interesting week. The Russell 2K Growth did a little better than the R2K Growth, R2K did much better than SP500. Obvious “pandemic recovery” names (the ones often cited in media, e.g. airlines) did very well, less obvious pandemic recovery names (equally direct fundamental exposure to pandemic ending, but seldom mentioned in media) were mixed, while “economic recovery” names (exposure to broad economic recovery beyond the short term pandemic) were just okay. Nasdaq (NDX) and tech were strong, with good earnings were treated like good earnings (over-generalizing, “tech” and “good earnings” are sort of synonymous right now.)

I guess this is what it looks like when you get oversold chart rebound, hedge fund re-grossing, short squeeze prospecting, vol target fund increasing equity, positive news on Covid/vaccines, “reflation” talk, earnings reports and fiscal stimulus progress ALL IN ONE WEEK.

Hot damn – wait, shouldn’t all that set up a positive market environment for more than just one week?

The easiest way to sound smart, wise, and insightful about the markets is to be some flavor of bearish. That’s natural, I think, because all the bullish broker blather that gets shoved down investors’ collective throats begets a contrarian reaction among critical thinkers.

All that said, I have a hard time not being bullish right now. Not so much on the broad indices (the SP500 type), but it feels like there are so many opportunities for stockpickers that, if that’s what you like doing, you’re going to be having fun.

2020 and 2021 are going to be the most opportunity-rich environment for stockpicking that we’ve had since, well, 2009 and 2010.

I fear that in 2022 we will revert to the numbing correlated large cap-led markets of much of the twenty-teens. Maybe that would be a blessing, because the likely alternative is a soul sapping generational bear market. I just added that last sentence to sound smart, wise, and insightful.

Great comment John L! You are a scholar and a gentleman, and indubitably smart, wise, and insightful!

Russell at start of Friday RTH ws up 14% YTD- That’s pretty good for one whole year! Wait, it ended higher on the day. Taking YTD total ~16%. Pain trade been short bonds, long small caps. If you pairs traded that since Nov election, you could be up handsomely.