The dollar firmed and risk appetite dissipated Friday as fresh virus concerns dented sentiment.

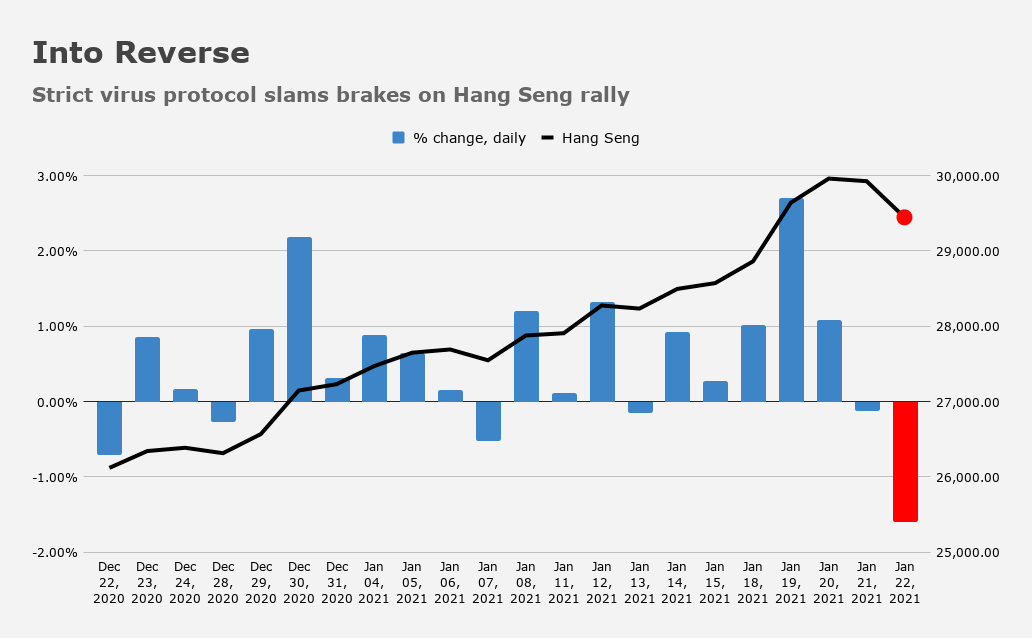

Hong Kong is locking down dozens of residential buildings in what’s been variously billed as the strictest measure yet in the city, which logged dozens of new cases Friday, almost all of which were locally transmitted. The lockdown was described as “drastic” by SCMP, which said the city would “deploy more than 1,700 disciplined services officers” to facilitate the effort in Yau Tsim Mong district “in an unprecedented bid to contain an outbreak in neighborhoods filled with aging, subdivided flats.” As many as 9,000 residents could be affected.

That put the brakes on a scorching rally in the Hang Seng, which had run up sharply in the new year thanks in part to flows from the mainland as investors show a preference for H-shares.

SCMP’s coverage described a draconian approach to the new lockdown in affected areas. “Only residents who showed negative COVID-19 test results would be allowed to leave their buildings,” a source said. Another remarked that “the purpose is to identify those hiding who have not received COVID-19 tests.” Apparently, half of recent infections were traced to the Yau Tsim Mong district.

Meanwhile, Boris Johnson refused to rule out the possibility that the UK’s lockdown could last into the summer. Retail sales in the nation were a bitter disappointment. ONS said sales rose just 0.3% in December. The market was looking for 1.3%.

The underwhelming print may have “surprised” consensus, but it’s hardly a surprise considering the circumstances.

Meanwhile, IHS Markit’s January PMIs for the virus-stricken country (which is, of course, attempting to orchestrate a complex divorce from the EU while fighting off an aggressive mutation of the pathogen), showed decelerating activity. Output sank at the briskest pace since May. The composite PMI printed 40.6, an eight-month low in the flash read for this month.

“UK private sector companies signaled a renewed downturn in business activity during January, which largely reflected national lockdown restrictions due to the coronavirus pandemic,” the color that accompanied the survey read. “The service economy was hard-hit by restrictions on trade and reduced consumer spending at the start of the year.” The flash read on the UK services PMI was 38.8.

Optimism about the future was the highest since 2014, so at least “hope floats,” so to speak.

Still, the current situation is dire. “This is a sudden blow to the UK economy as recovery in the two sectors lost its momentum after some improvement at the end of last year,” Duncan Brock, Group Director at CIPS, remarked. “Affected by consumer caution and dried-up pipelines of new work from domestic and export customers, new orders dropped to an extent not seen since May, underlining the continuing instability in a marketplace no longer propped up by pre-Brexit stockpiling or reduced restrictions on business conditions.”

In a testament to the shock caused by Brexit-related logistical issues, IHS Markit noted that the “latest data pointed to the largest increase in suppliers’ delivery times since the UK Manufacturing PMI survey began almost 30 years ago.”

And it just goes on and on. “Consumer confidence declined this month as Britons became more pessimistic about their own financial outlook,” Bloomberg wrote, referencing a GfK survey, and adding that “on Thursday, ONS said purchases made by credit and debit cards fell 35% below pre-pandemic levels in the second week of January [while] footfall in stores last week was one-third of where it was a year ago.”

All of this underlines the extent to which vaccine rollout notwithstanding, the “here and now” reality for the global economy is still perilous — both for locales that have had success in containing the virus and, naturally, for those which haven’t.