Joe Biden’s stimulus proposal “is a big package,” the Boston Fed’s Eric Rosengren said Friday. “But I think it’s appropriate.”

I’d venture the nearly 10 million people who had a job this time last year but don’t have one now probably agree. “The economy is in a lull, we’ve had a series of pretty weak data,” Rosengren went on to say, during remarks to CNBC.

This is a good time to step back and recall that Fed officials spent the better part of the last six months imploring lawmakers to deliver more fiscal stimulus. Long story short, the FOMC wasn’t particularly keen on the prospect of spending the next five years trying to rescue the world’s largest economy without a sufficiently robust and sustainable fiscal impulse.

Larry Summers, speaking to Bloomberg Friday, said Biden’s plan will overheat the economy.

“We’re going to have to watch this very carefully, and I think the conventional wisdom is underestimating the risks of hitting capacity,” Summers, who Bloomberg now identifies as a “paid contributor,” remarked.

Larry found himself on the receiving end of criticism late last month, when he derided more stimulus checks, citing similar concerns about “overheating.”

Read more: Somebody Help Larry Summers. He’s Stuck In A Textbook

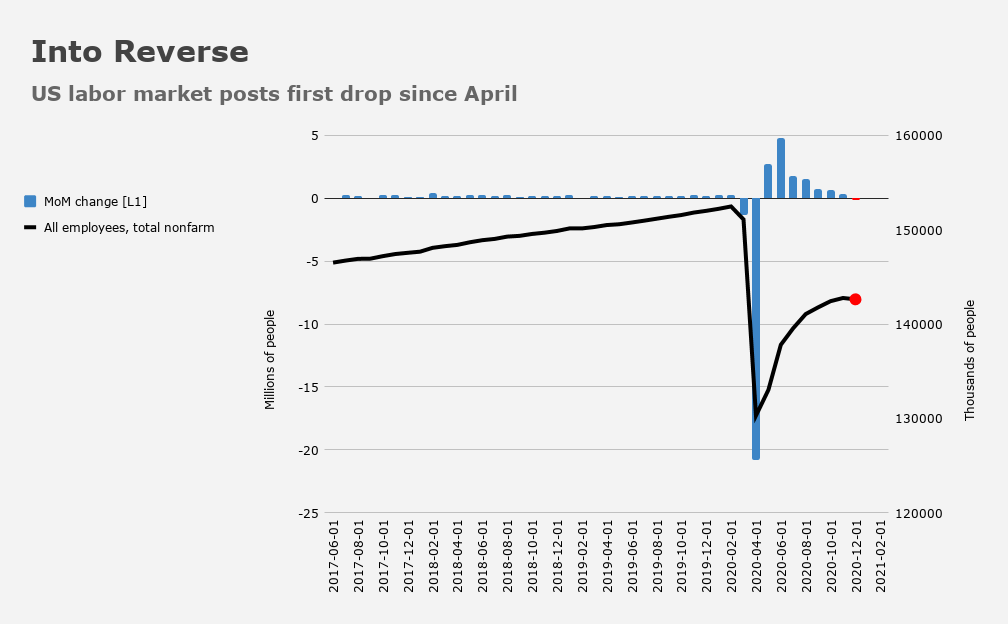

If it seems ludicrous (or at least potentially spurious) to you that anyone would suggest that an economy which is still 10 million jobs short of pre-recession levels and still spitting out weekly claims prints close to 1 million, might soon “overheat,” you’re not alone.

Of course, if you’re with Summers on the notion that direct payments aren’t a good idea or that they should be more narrowly construed, you’re not alone there either.

Bloomberg has a habit of accidentally employing dry humor, and their Friday piece on Summers was no exception. “Summers didn’t elaborate on what the overheating would look like,” Julia Fanzeres wrote.

That’s probably because it’s difficult to picture right now. Does the figure (below) look “hot” to you?

“We need to do more to support the economy,” Rosengren went on to tell CNBC.

For his part, Neel Kashkari struck familiar chords — for Neel, I mean.

“The end of the pandemic is further away than maybe we thought it was,” he said, during a virtual chat. He fretted over the sluggish pace of vaccine rollout and also a reluctance on the part of some Americans to get vaccinated. In his estimation, Kashkari said the pandemic is “probably going to be all of 2021.”

“Global vaccine rollout thus far [is] below expectations,” BofA’s Michael Hartnett wrote Thursday, in the latest edition of the bank’s popular “Flow Show” series, noting that vaccinations are “significantly behind” the bank’s projections.

Documenting the ongoing struggle, The New York Times cited “logistical confusion, shortages of doses, unequal distribution and bureaucratic hurdles” as factors “that have slowed the process of getting shots into people’s arms.”

The CDC warned Friday that the more contagious UK variant could become dominant in the US. “As of January 13, 2021, approximately 76 cases of B.1.1.7 have been detected in 10 U.S states,” the CDC said, adding that,

Multiple lines of evidence indicate that B.1.1.7 is more efficiently transmitted than are other SARS CoV-2 variants (1—3). The modeled trajectory of this variant in the U.S. exhibits rapid growth in early 2021, becoming the predominant variant in March. Increased SARS-CoV-2 transmission might threaten strained health care resources, require extended and more rigorous implementation of public health strategies (4), and increase the percentage of population immunity required for pandemic control.

Meanwhile, Pfizer is reducing vaccine deliveries to Europe due to upgrades necessary to boost production capacity. Those upgrades “presuppose adaptation of facilities and processes at the factory which requires new quality tests and approvals from the authorities,” Line Fedders, a spokeswoman, told the AP. “As a consequence, fewer doses will be available for European countries at the end of January and the beginning of February.”

Oh, and the UK is closing all travel corridors starting Monday in order to “protect against the risk of as yet unidentified new [COVID] strains,” Boris Johnson explained. “It comes as a ban on travelers from South America and Portugal came into force on Friday over concerns about a new variant identified in Brazil,” the BBC noted.

This is the backdrop against which some folks believe more fiscal stimulus risks “overheating” economies.

And who knows. They may be right. “Overheat” has no set definition, after all. Moreover, the pandemic does have an inflationary side, most notably via supply chain disruptions.

Still, it’s hard to escape the notion that the economic damage will linger and that we’re surely closer to double-dip recessions across western economies than we are to any broad-based “overheating.”

“I don’t see much risk of inflation shooting way above 2%,” Kashkari mused. The US labor market is “still as bad as the worst job market in the financial crisis,” he added.

Lukewarm and cooling.

I understand inflation becoming too hot but using that term in a general sense implies you do do not care for an expanding GDP above consensus.

Summers is the moron who nearly bankrupted Harvard University. The trumpian level of incompetence required to “achieve” this should render anyone with the permanent label of “unqualified”. He should be ridiculed as a Robber Baron puppet in any forum for financial discourse. Any point he makes should be taken as the opposite of true/valid.

I have been worried/expect “overheating” 2-5 years from now as the Republican hate cult obstructs meaningful conversation on how to best administer a de facto UBI program. This obstruction forces all the decent human beings in Congress to defend the programs existence when we should be focused on optimization. It’s a wash rinse repeat of the strategy employed to obstruction the ACA which resulted in sub optimal healthcare legislation.

As such I expect the de facto UBI to create some overheating because of a sub optimal rollout far into the future.

None of this addresses the absolute need to address the current human tragedy of severe financial hardship for millions of Americans. Any propagandist belittling that tragedy needs to be mocked, ridiculed, and run out of town.

I don’t use ad hominem attacks on anybody, preferring instead to frame an individual as prone to bloviate. Or, to politely refer to a “thought leader” as someone whose influence peaked in the 1990s and should think of themselves as an influencer any longer. Or, politely refer to a personality as an out of touch, Ivy League elitist. I hope that Summers is not invited onto the Sunday morning politics circuit. Further, I hope reporters have the good sense to ignore him.

I put Summers into the same camp as Grantham and Buffett…it’s a place called the dinosaur park, those who made it fat, had the good life, maybe become billionaires, but no longer have positive, intellectual value add in realm of public discourse…when this occurs, it’s time to retire from the public eye.

Maybe things end up being worse this year (for both the virus and the economy) than was anticipated as recently as 16 days ago. Obviously, we are starting with a bias given this terrible January. Maybe the H2 estimates for when we get back to the good times get revised to H1 22. Plus, some horrible things politically in 2021 have be expected that could further crush our nation’s spirit …not that the general mental health, the sentiment of the soul of our nation, has anything to do with asset prices.

Seems like a good time to take some profits.

Too right, sir. Economists like Summers and Laffer all have one thing in common. They have a very nice job, Michelin food on the table, some kind of tenure protection and an occasional public audience. Trouble is, as runamok points out, they are mostly past their sell-by date. Enough already with these guys — the 60 some panelsists who never get it right every month. The damage some of them do with their erroneous theories is incalculable. My cleaning lady hasn’t had a regular job or health insurance since May. What she has had in the last year is stage three cancer and surgery to remove her gall bladder, all while she provides the care for her bi-polar and aging brother, and supports three other family members. These are the real people Summers and Laffer and their ilk never see. And we still steadfastly consider ourselves a “Christian” nation. Shame on us.

Larry has become a cartoon. I single him out often because I have no patience for him, and because he, maybe more than anyone, blocked the few open routes by which progress was politically possible. There was political mandate and political will after the GFC. But in an act of self-censorship, he forced a philosophical error in refusing to engage and debate with less orthodox ideas and larger numbers that might have actually “worked”. He insisted 1T$ back then was bad optics. How scientific of him. He forced us down a certain path, and as such we have been in a form of depression for 12 years because of this arrogant, know-it-all attitude that does things like base critical generational economic decisions around “optics”. And in recognizing the attitudinal component to his actions, I can’t help but wonder whether his ongoing commentary is just an effort to obfuscate his own past mistakes. We must learn from mistakes, not endlessly repeat them because a self-appointed high priest of economic “science” with a giant ego says we must.

I thought Roemer was the one that was overly optimistic back then. I do remember the optics quote though from someone back then. I remember thinking at the time that the optics of a 1t deficit might be bad but 15% U-6 unemployment and a depression would be infinitely worse. At this point, just like during the financial crisis, one may have a bone to pick with certain policies but on a simple level- it is better to go overboard with stimulus than fall short. While I agree, there are better ways to stimulute than to send checks to couples making 150k (I would suggest lowering that limit and being more generous elsewhere), if that is what it takes to get proper state and local aid, vaccine and treatment aid, higher and longer unemployment benefits, an increased minimum wage, and eviction protection then I am all for it.

Romer was actually pushing for more by got shut down by Larry. Regardless, the right voices were never even allowed in the room. They were all far too timid in the face of a historic crisis, but Larry is/was particularly domineering, even when dealing with the president. There are plenty of paraphrased quotes out there of him saying things like ‘now that the adults are in the room…’ after Obama had just walked out.

There are plenty of paraphrased quotes out there of him saying things like ‘now that the adults are in the room…’ after Obama had just walked out.

I always disliked Summers and now I know why. But then why did Obama fight for him to be the head of the Fed instead of Yellen?

I see us as being in a twenty year recovery from the 2008 implosion of the financicl system couple with the create of a ferocious bubble in various assets- stocks, bonds, real estate, college etc. I also see a new cycle- a recovery from the destruction of small business, the public gathering sector(bars, restaurants, vacations, travel etc.}brought about by the response to the pandemic and a speeding up of the cycle replacing human capital with intellectual property. This is all global. We also have exceptionalism in that we are the world’s currency and we have used that to exacerbate our balance of payments issues. I don’t judge anyone who is unsure what the best response to this is. See you in 2040….

I also think you should interview Peter Turchin