Is the move in breakevens overdone?

One bank thinks the answer is “maybe.”

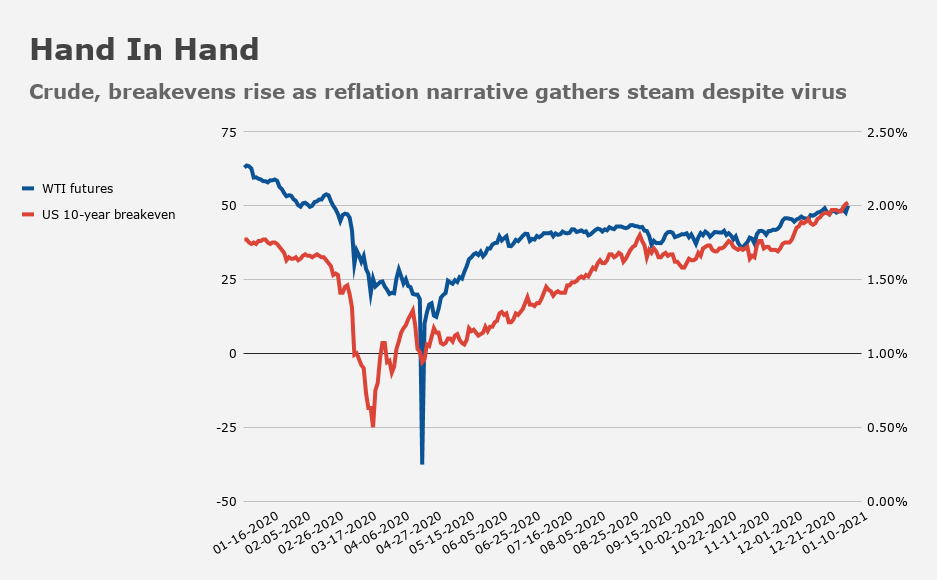

If you don’t know the context (and perhaps even if you do) this isn’t the most exciting debate in the world. But it is important to the overall market narrative. Breakevens breached 2% for the first time since 2018 recently, as the reflation trade gathered steam.

Since the March 2020 collapse, breakevens have risen pretty much in lockstep with equities, and, in turn, real rates in the US were driven deeply negative. That conjuncture is part and parcel of the rally in risk assets.

What’s particularly notable is that it’s proceeded virtually uninterrupted despite a vicious winter COVID wave, associated lockdowns, and the obvious loss of momentum in the US labor market.

Of course, the approval of multiple vaccines and the assumption that inoculation rollout, while slow, will ultimately proceed (and succeed), gives the market something like carte blanche to keep pricing in the reflation narrative.

The Saudis added figurative fuel to the fire last week by promising to refrain from adding literal fuel to an oil market that is still extremely fragile.

But if you ask Deutsche Bank, things may have overshot in the near-term. “Although we concur with the general thesis behind the reflation trade assuming the new administration can deliver persistent fiscal support, the ‘slow moving’ economic drivers have yet to move in the direction that would substantiate this view, which calls for caution on breakeven potentially running too hot,” the bank’s Jiefu Luo and Jose Gonzalez wrote, in a note dated late last week.

On the bank’s model, fair value for 10-year breakevens is 1.89, essentially unchanged from last month. For what it’s worth, the model residual shows BKEs are one-standard deviation wide.

Long story short, we may not be out of the deflationary woods yet.

“Disinflation probability, a key model driver, has seen minimal variation due to the lackluster recovery in consumer prices,” Deutsche Bank’s analysts said, adding that “labor market woes manifested in the slowing decline of claims exacerbate disinflationary impulses in our model.”

What about the impact of the Saudis’ unilateral decision to cut output to support crude and the prospect of more stimulus under Democrats? Don’t those factors matter?

Yes. But it’s probably priced in — at least for now, according to Deutsche. “Saudi production cut and the Democratic victory in the Georgia Senate runoff have largely been priced in at this point,” the bank wrote.

If this is correct, it has implications for real yields (which rose last week) and that, in turn, has implications for the dollar and risk assets.

Commenting last week, Morgan Stanley’s Guneet Dhingra said that yields will probably keep “grinding higher,” and that the “template” from the last six months wherein breakevens lead thanks in part to upbeat economic data, is a “good one.” However, Dhingra also said that Morgan “expect[s] a higher participation of real yields… from here.”

I’m just a nut in the peanut gallery who don’t know squat. For me, the relentless march higher in real rates is my biggest surprise since the summer.

I suspect the playbook will be…real rates go up to some threshold…algos kick in and do what they do…equities tank 20%…Fed quells markets with words or promises to purchase…equities pursue relentless move higher. Or, the Fed might pre-empt the whole thing and make purchases to put a lid on it before something breaks. Or, there is a spasm of disinflationary pressure with all the upcoming bankruptcies in commercial real estate and whatever other bad news is sure to emerge, the whole reflation trade unwinds in a week, the world looks like it’s coming to an end to mark the 1-year anniversary of March 2020, real rates end up back at 0.6%, and by June, equities and the reflation trade begin afresh.

…jeez, that TLT chart. Or, maybe just embrace the new world of higher yield. I’m going to call my S&L and buy some CDs to lock in the killer yield on my cash.

Worth noting that the US breakeven curve is inverted, with 2yr inflation expectations now well above 5s and 10s. This potentially suggests to me that much of the move is driven by base effects, WTI crude and other commodities rather than long term demand side inflation pressures. I’m also not sure if historically (in the post TIPS era) the inversion has ever been resolved by forward breakevens catching up to short end breakevens (rather the entire breakeven curve has tended to roll over).