At a time when too many market participants are seemingly terrified of hyperinflation (or at least if you attribute part of gold’s summer surge and recent record highs in Bitcoin to debasement concerns), there sure seems to be a lot of disinflation going around.

While it’s undoubtedly true that the pandemic was a supply shock and thus could add to inflationary pressures down the road, COVID-19 was first and foremost a demand shock of epic proportions. Just ask the oil industry. Or the services sector.

That means that whatever happens over the medium- to longer-term, we’re still not done working through the deflationary effects. Given that, it should come as no surprise that consumer prices dropped again in Europe last month. CPI was -0.3% on the flash read, more sluggish than the expected -0.2%.

So, that’s four straight months of negative prints on the headline gauge. Core remained stuck at a record low of 0.2% last month.

To be sure, this was expected. ECB officials have said that inflation is likely to remain negative for at least a few more months, as the oil price shock and tax cuts work their way through.

Still, new lockdown measures instituted last month across Europe’s largest economies imperil the outlook further. In Germany, for example, CPI slipped at the swiftest pace in more than 10 years.

This will make it even more difficult for the ECB to hit its ever elusive target, which is now so far away that Christine Lagarde can’t even see it through the clouds (but you can see it on the red line in the figures above).

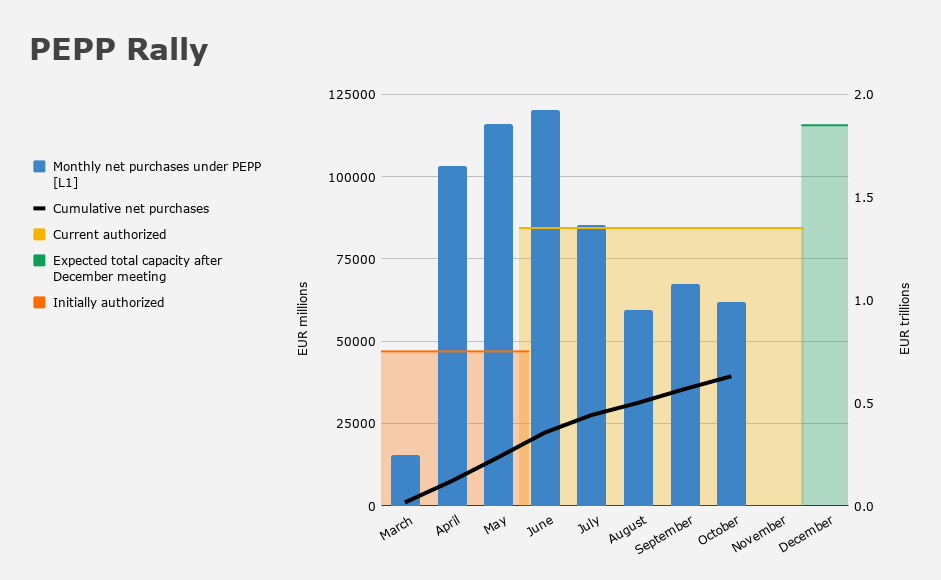

The ECB will almost surely top up its pandemic emergency QE program this month, bringing the facility’s firepower to nearly €1.9 trillion.

Some might be inclined to call that an example of “Einstein insanity” — that is, doing the same thing over and over again and expecting different results. Asset purchases and negative rates have failed to bring inflation sustainably to target in the post-financial crisis era, so why should they work any better in that regard now?

I’d note two things. First, Einstein never actually said that about insanity. Second, and more germane, if it’s insane for central banks to keep buying assets and cutting rates with the expectation that inflation will eventually rise even though that’s never worked before, what does that say about all the pundits who insist that “money printing” will eventually lead to hyperinflation? They must be insane squared.

Given that stock markets have a an essentially infinite capacity for capital absorption and that financial elites have an essentially infinite capacity for saving, what is supposed to stimulate hyperinflation? Us rank-and-file types certainly can’t be accused of possessing too much money and chasing too few goods.

I said the same thing but yours is the better/snappier expression… 🙂

Bingo! Maybe if wages were tied to stock prices/dividends it might work but all I’ve seen post GFC is get more done with less people, less raises, less promotions. Almost all the consumption demand is at the bottom 90% of the population and all the new money creation is going to the top 10% and primarily the top 1%.

They are equally insane inasmuch as we know why these policies will NOT bring about inflation. B/C the money isn’t being funnelled to The People.

But, if they were to really drop money from helicopters onto the masses, the only thing that would maybe prevent inflation is the degree of openness of a given economy i.e. how much initial spending goes straight out of the country. But even within very open economies, I wouldn’t bet on that being enough to stop inflation from rising.

Maybe not to hyperinflation levels but at least to 2%… 🙂

Point taken. In a country with out characteristics, a share of the money would end up flowing south into the hands of Mexican drug cartels. Through the laundering of the funds that I presume has been happening for decades now, it would end up back in Wall Street banks. The application of the funds would go into businesses but also into financial assets.

I’m being silly. But, there is a percentage of Main Street targeted money that would escape Main Street and go into illicit channels. What, eight to 12% maybe?

I mean you would have to drop enough to cover the debts/savings demand before it would make much of an impact. That means you could drop like a couple trillion on the general populous before they would do anything but hand it back to banks.

A casual observation of Americana leads me to believe you guys aren’t into savings… If money is dropped on you, a goodly chunk will be spent on goods and services, not neutralized in a saving account…

Money printing will generate inflation given normal or the right circumstances. In the face of a demand shock, zero interest rate bound/liquidity trap, that is not the case presently. It is bizarre that there are some that will parrot the line about inflation whenever central banks ease in the face of dire circumstances. It will take years and probably some real demographic and political changes for money printing to generate significant inflation down the road.

And the real question is, how much money would you have to print and put in Warren Buffett’s bank account before the average McDonald’s employee flipping burgers gets a dollar raise? I am not sure that amount is in the realm of conception. A Trillion? A Quadrillion? A Googolplex?

We’re also seeing deflation throughout Asia right now, and not just in Japan. Even in China, y/y CPI has fallen to 0.5% while PPI is still in deeply negative y/y territory.

I think part of the reason politics in Europe and the United States are so healthy right now is because people are so contented by all of their enhanced purchasing power. Wages don’t even need to rise because consumer prices keep falling, which is why savings rates are through the roof and households carry so little debt.

It can’t be as simple as supply-demand?? A huge over-supply and dwindling demand = deflation.