Last week, Riccardo Fraccaro, cabinet undersecretary to Italian Premier Giuseppe Conte, suggested the ECB should considering canceling some of the sovereign debt bought during the course of the pandemic.

“Monetary policy must support member states’ expansionary fiscal policies in every possible way,” Fraccaro, speaking during an interview in Rome, said. “Canceling sovereign bonds bought during the pandemic or perpetually extending their maturity” would be one way to achieve that, he added.

Frankly, the suggestion wasn’t met with the kind of derisive cacophony I would have expected, although perhaps I just wasn’t paying enough attention to the peanut gallery on finance-focused social media (I’ve all but tuned out of that channel in the interest of preserving the kind of tranquility I’ve become accustomed to).

Read more: Italian Official Has An Idea For The ECB: Just Cancel The Bonds You Bought

I bring this up again because as I was perusing Bloomberg’s weekend coverage, I noticed a piece dedicated to the collapse in periphery yields, which were, of course, the locus of pain during the bloc’s sovereign debt crisis.

Specifically, Portugal nearly saw its 10-year yield fall below zero last week, which would have made the country the first periphery borrower with sub-zero yields on government debt due in a decade. The figure (below) is simple, but it never seems to lose its capacity to “wow,” so to speak.

Essentially, the market is pricing no risk at all for this debt, and it’s no secret why. The ECB, under Mario Draghi, explicitly dedicated itself to stamping out fragmentation risk at any cost, and the pandemic renewed the sense of urgency.

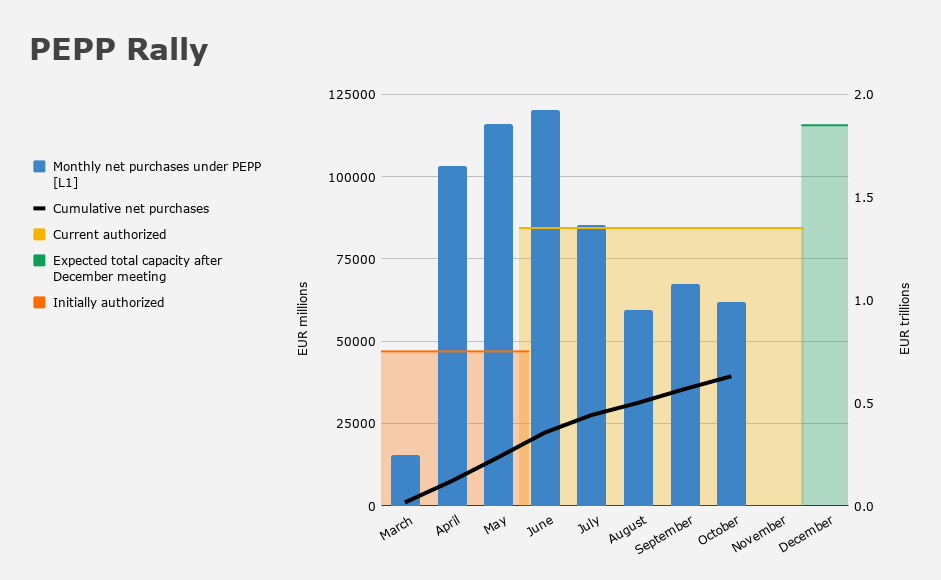

In addition to expanding “regular” QE, Christine Lagarde has, of course, spent hundreds of billions of euros buying assets as part of the bank’s emergency pandemic purchase program, first announced in March with initial firepower of €750 billion. It was expanded in June to €1.35 trillion.

The facility, PEPP, hasn’t reached capacity yet, but the market widely expects the ECB to top it up next month anyway. Authorizing an additional €500 billion in purchases (which, generally speaking, is what consensus expects) would bring the total envelope to nearly €1.9 trillion.

While there’s nothing “new” in any of the above (well, aside from Fraccaro’s explicit call for the ECB to cancel debt), it’s always worth stepping back to ponder the world created by central bank asset purchases.

The first figure above (the chart showing the inexorable decline in yields) has very little to do with any fundamentals, or at least not the headline debt-to-GDP ratios you’d normally cite if you wanted to make a generic case for lower sovereign borrowing costs.

Debt burdens for Italy, Spain, and Portugal are higher now than they were during the debt crisis, and yet thanks to the hunt for yield engendered by the ECB, that’s no obstacle to borrowing.

As Bloomberg noted in their coverage, Italy sold “over 100 billion euros of medium-to-long term bonds more than planned this year, and Portugal [raised] 50% more than forecast,” but neither faced any signs of investor pushback, as Italy “racked up 108 billion euros of orders for a 14-billion-euro debt sale in June, while Portugal set its own record for a syndication the following month.”

Remember: ECB support is key when it comes to market confidence in these sovereign borrowers precisely because they aren’t really “sovereign” in a monetary sense. Theoretically, they can all involuntarily default because they are effectively borrowing in a foreign currency. They cannot print euros. They are not like the US, the UK, Australia, Canada, and so on.

Anyway, I suppose it doesn’t matter. Because when the global stock of negative-yielding debt is approaching $18 trillion, 0% looks “juicy” indeed. And besides, the fixed income rally just never stops.