No, Donny, these men are nihilists. There’s nothing to be afraid of.

“Nothing matters but liquidity”, BofA’s Michael Hartnett writes, describing what he calls “The Nihilistic Bull of 2020”.

Much has been made of the disconnect between Main Street and Wall Street in the post-financial crisis world, but the pandemic threw the already dramatic divide into even starker relief.

There are any number of ways to visualize the disparity, but second quarter earnings results from Wall Street provided a particularly poignant juxtaposition. JPMorgan, Wells Fargo, Citi, and Bank of America set aside some $33 billion for losses tied to the deteriorating economic outlook which drove millions of Americans to the brink of financial oblivion. At the same time, Goldman, Morgan Stanley, Citi, and JPMorgan generated some $25 billion between them in FICC trading revenue and debt underwriting fees, bolstered by the Fed’s intervention in the corporate bond market.

Read more: Wall Street-Main Street Divide Laid Bare During US Economy’s Worst-Ever Quarter

I (strongly) encourage readers who may have missed the linked article (above) to peruse it at your leisure, as it speaks loudly to the unintended (and, depending on your penchant for cynicism, intended) consequences of accommodative monetary policy in a crisis.

BofA’s Hartnett offers another way to visualize the divide.

“[The] value of US financial assets (Wall Street) is now 6.2X size of GDP (Main Street)”, he writes, describing his “Nihilistic Bull”.

He goes on to say that a GDP loss of $10 trillion and total US jobless claims of 53 million have been “numbed” by more than $21 trillion in policy stimulus. Hartnett also marvels at “$2 billion per hour in central bank asset purchases”.

Similar sentiments (and more) were voiced recently by Cornerstone Macro’s Michael Kantrowitz, who argued that stocks have become “too big to fail”. Among other statistics, he cited the US market cap to GDP, the correlation between the S&P and consumer confidence, and stock values relative to employee compensation.

(Cornerstone Macro)

“One could argue that falling stock prices have never had the potential to be such a drag as they are now”, Kantrowitz said, in a note, adding that “stocks are too big to fail here because a big drop in the stock market could leave the US government an enormous bill”.

In other words, policymakers (whether that means Congress or the Fed) can’t risk a serious decline in stocks. Everyone is generally familiar with the “wealth effect” whereby rising equity prices are imagined to manifest in the real economy as consumer confidence is bolstered by inflated 401(k) balances and the like.

When that wealth effect slams into reverse, it has the potential to derail consumer spending.

In an interview with Bloomberg, Kantrowitz suggested policymakers will be tempted to bail out the stock market in a pinch given that, as he put it, “the ‘cost’ of lower equity prices has never been greater”.

Read more: The Final Leap – America’s Overlapping Crises May Make Fed Stock Buying Inevitable

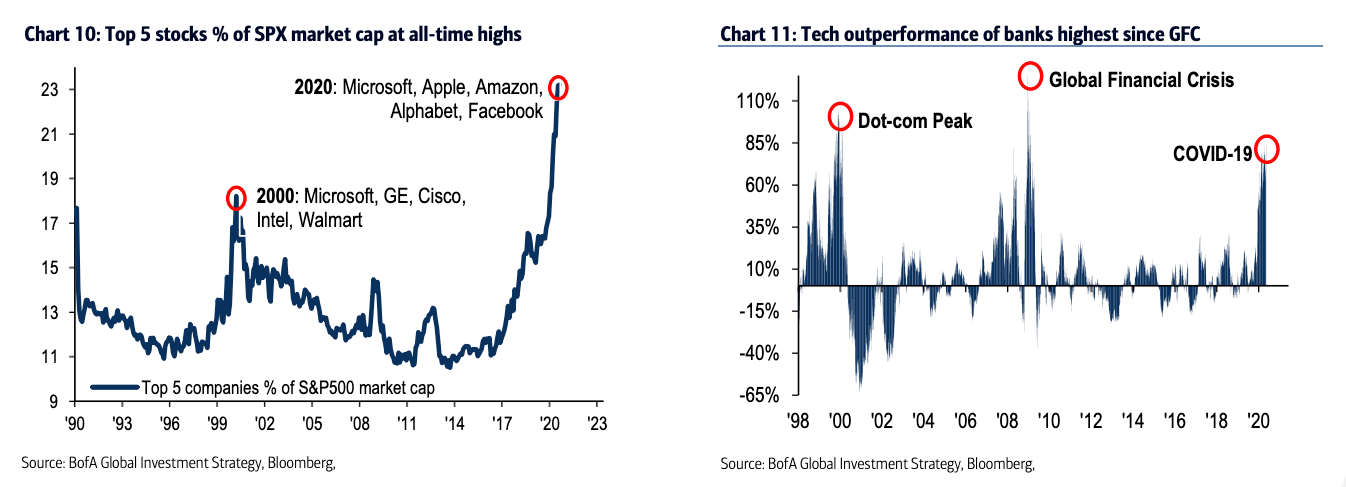

In the past, I’ve suggested that Congress (and The White House) may want to consider the ramifications of anti-trust probes and other aggressive actions against mega-cap tech considering how large a role they play in propping up the broad market.

Apple’s share in the S&P ballooned to 6.5% this week, surpassing IBM’s decades-old record for influence on the benchmark. The concentration for Microsoft, Amazon, Apple, Google, and Facebook is now in excess of 23% following blockbuster tech earnings delivered late last month.

All of this suggests that “letting stocks go”, as it were, in the event they fall precipitously will be a non-starter for policymakers.

“If you don’t think that the mechanical processes that have been worked out over the course of the past [few] months with the Fed now being a top-five holder in many credit ETFs was a test drive for equities purchases, you’re wrong”, Nomura’s Charlie McElligott said in July, during a lengthy podcast interview.

Of course, all of the above largely ignores the fact that equity ownership is concentrated in the hands of a relative few. The fact is, the vast majority of Americans don’t care much about stocks precisely because they don’t own many shares. The bottom 50% likely doesn’t care at all. What stocks do or don’t do is irrelevant for them (figure below) unless the proximate cause of a given rally or selloff has broader ramifications for the economy and thereby for their own economic well-being.

While voters may indeed believe that a healthy stock market is indicative of American economic prowess and thereby be prone to expressing higher levels of optimism when headlines tout records on Wall Street, comparisons between, for example, employee compensation and the market cap of US stocks, can be misleading.

If a large share of workers don’t own any stocks (to speak of) and thereby don’t receive any dividends, then ratios like those shown in the figures above from Cornerstone are meaningless unless the reversal of the wealth effect for those who do own shares means those people consume less of the services provided by lower- and middle-income Americans. In other words, those ratios could well be characterized as proving the exact opposite of what they purport to show. That is, if I’m a worker, and I own very little in the way of stocks, then a stock market crash means nothing to me as long as my compensation isn’t affected.

Still, the general message from BofA’s Hartnett and Cornerstone’s Kantrowitz is duly noted. It’s entirely possible that US stocks are now “too big to fail”, or at least as long as the economy is still struggling to cope with the fallout from the pandemic. Even if most regular people aren’t all that concerned about equities, another steep selloff would represent insult to injury even if you only held a few thousand dollars worth of shares in an index fund, for instance.

Seen in that light, I suppose it makes sense that the March nadir for the S&P represented the “big low”, to adopt Hartnett’s cadence (he often speaks of “big lows” and “big tops”).

A re-test of those levels simply wasn’t a tenable outcome and still isn’t. It can’t be allowed to happen. So, it won’t. Or at least not if policymakers can help it.

Nihilists, f*** me. I mean say what you will about the tenets of MMT, Walt, at least it’s an ethos.

Maybe this time really is different but even entertaining these thoughts let alone discussing rings a bell in my head. Sure there may be a blow off top and maybe Fed buying at some point but ultimately people will require a real return (divdends) financed by free cash flow rather than debt. Sure that may be a ways away but if everyone believes there is only one way to rock they are probably over invested and the marginal transaction may just not be supportive.

Good luck everyone, be smart.

Surely I am an idiot to say this, but if the vast majority don’t own stocks, and stocks are not the economy. why would it matter if stocks got crushed?

Well, there’s the looming public sector pension crisis. It’s already bad, but would be outlandish if stocks crash as most pension funds have a lot invested in stocks. And from the Fed’s perspective, they have relatively few policy levers to pull. If manipulating the stock market is one of them, then they’re going to use it.

Vlad,

The theory is the weath effect influence of stock owners pulling back on spending that support non stock owner’s jobs.

I think the other influence rarely discussed is the corp actions due to lower stock prices. Restructuring a that result in job cuts. Less capital spending. A pullback in advertising. Even a reduction in innovation/R&D. In order to “beat” lowered estimates and get stock options back in the money and cash bonus targets being reached.

Of course those corp actions have a negative impac on the economy but often enrich executives (which is all many or most really care about).

The hollowing out of the middle class will continue and be particularly severe in the next downturn which we are near and may last years.

BTW as a retired HF manager I am not a bitter middle manager. Just saddened by all the mis-steps the country seems to take every year. We never address the underlying causes. These recent mis-steps will prove to be the most egregious of them all imo though an alternative to avert disaster is not readily apparent either.

I feel badly for 95% of Americans.