“NASDAQ HITS ALL TIME HIGH!”, Donald Trump screeched into the digital void on Monday, as US stocks followed their global counterparts sharply higher in a rousing start to the new week.

To be sure, the president isn’t the only one inclined to scan today’s business headlines, shriek about records, and then move along, content in the notion that as long as equities are loitering in rarefied air, all must be right in the world.

The S&P gunned for a fifth day of gains (its best run of 2020) and Amazon hit $3,000 for the first time (one imagines that component of the rally doesn’t necessarily please the president).

The simple comparison in the top pane (between, on one hand, Jeff Bezos and, on the other, US banks and energy companies) is remarkable, not matter how many times you see it.

Last week, in “‘It Can Always Get Stupider’: Nasdaq Bubble Warnings May Be False Equivalence“, I spilled quite a bit of digital ink discussing whether tech is a bubble (again) and, if it is, whether it’s comparable to the dot-com boom.

The answer to the first question (“Is tech a bubble?”) is probably “yes”, or at least “yes” in a relative sense.

The answer to the second question (“Is it comparable to the dot-com boom?”) is certainly “no”.

Tech is where the growth is, both on the top- and bottom- lines. And while there’s something distasteful (and wholly disconcerting) about just five companies comprising more than 21% of the market, recall that Facebook, Apple, Amazon, Alphabet, Netflix, and Microsoft are almost solely responsible for sales and profits outperformance in US stocks. As discussed here in May, when you strip those out, corporate America hasn’t done much better than “corporate world”.

Again, that’s disconcerting on many levels. It doesn’t say much for the dynamism of America’s largest companies when, as a group, they owe their outperformance versus the rest of the world to just a half-dozen members.

On another level, though, it’s comforting to know there’s at least a fundamental rationale for the Nasdaq’s inexorable ascent.

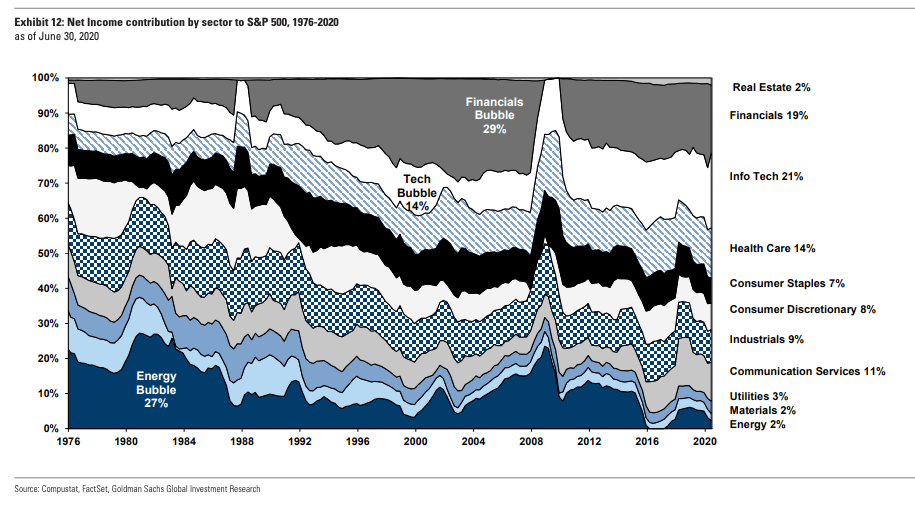

“At the peak of the tech bubble, Information Technology never generated more than 14% of the S&P 500’s earnings”, Goldman writes, noting that “the profit contribution from Info Tech increased over the past few years and the sector now accounts for 21% of S&P 500 net income”.

This isn’t an apples-to-apples comparison due to where the behemoths are classified sector-wise, but it speaks to the same, broader point — namely that if making money counts for something when it comes to legitimizing outsized gains and rising levels of concentration, things are far less disconnected than they were two decades ago.

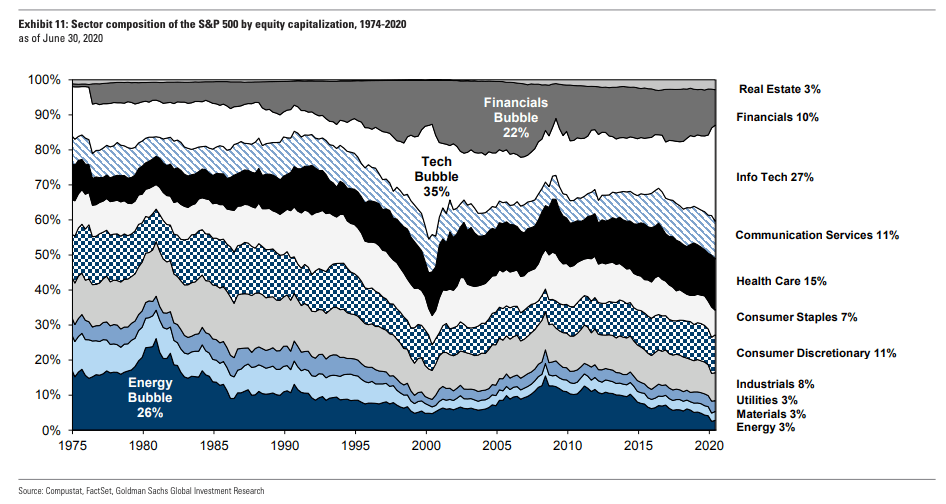

The following visual, also from Goldman, shows that at the height of the dot-com bubble, tech’s share of the S&P’s market cap was as high as 35%, despite it contributing just 14% of net income.

Obviously, it makes far more sense for a given sector to represent 27% of market capitalization when it contributes more than a fifth of net income, than it does for that sector to represent more than a third of of market capitalization while chipping in just 14% of total earnings.

Throw in the fact that secular growth works well in a “slow-flation” environment, and a post-pandemic reality wherein society is reevaluating the extent to which in-person interactions are even necessary, and you’re left with a pretty solid investment case, even if multiples are seemingly stretched to the breaking point.

Now if only we could get rid of everything that isn’t “useful” anymore, the S&P would be sitting at 4,000.