A quick glance at the new Fed dot plot that accompanied the June FOMC decision was all one needed to know that any pretensions to normalization have been abandoned.

To be sure, market participants expected (in some sense “demanded”) that the Fed telegraph its intent to keep rates at the lower-bound for the foreseeable future.

But expected or no, the bottom line is that they’ve stopped pretending. The “state of exception” is permanent (I’m not sure how many are buying the longer-term dots in light of recent events and past experience).

The reference to the “state of exception” will be familiar to long-time readers. It’s an allusion to a classic 2017 piece by Deutsche Bank’s Aleksandar Kocic, whose notes transcend Wall Street analysis to dwell in a realm all their own, where rates derivatives strategy commingles harmoniously with philosophy and political science.

Of all the frameworks for understanding the evolution of monetary policy, none has been cited in these pages more often than Kocic’s “state of exception” characterization. Late last month, for example, I employed it in a piece about “administered markets” (see “Why Would Anyone Expect Stocks To Price Rationally?“).

In a note dated Friday, Kocic delivers what I suppose we can call the “official” sequel to his original 2017 note. The new piece is called: “State of exception redux: This time it is here to stay”.

“In times of crisis, which shake up the accepted order of things, the enhanced power to transcend existing rules and laws in the name of ‘public good’ are given to a superior entity, ‘the sovereign’, until the crisis is over”, he begins, noting that “in the political context, this is referred to as the ‘state of exception'”.

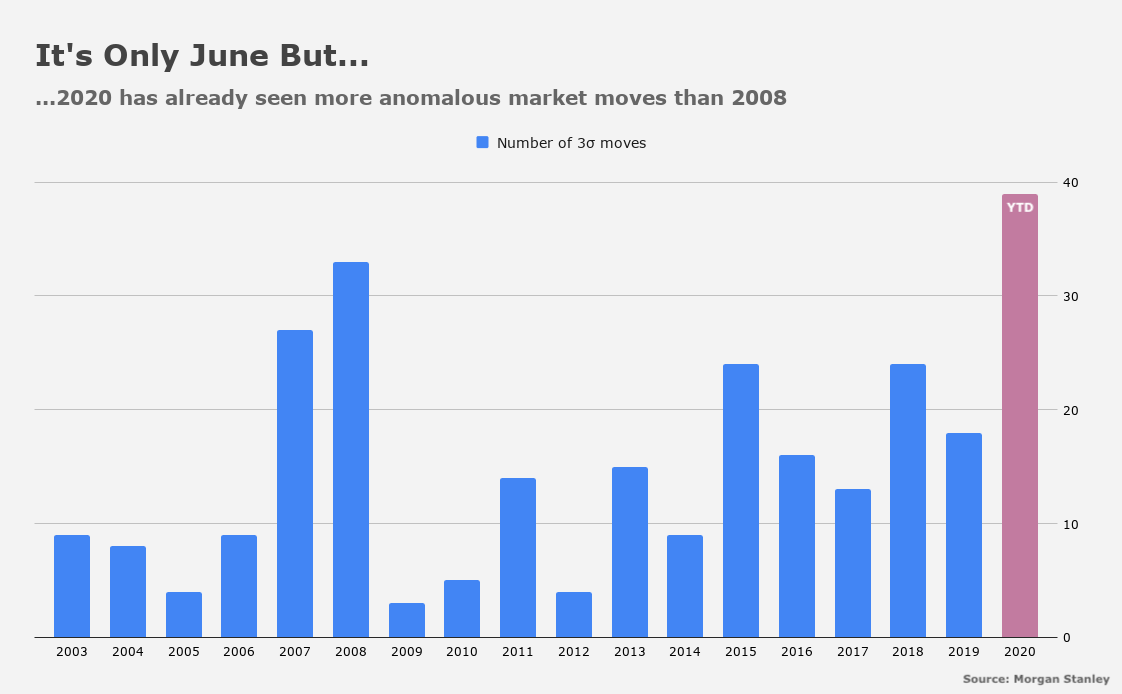

Obviously, “the sovereign” in this context is central banks, and particularly the Fed. The rules of the market must be suspended if the circumstances become too acute. Suffice to say the conditions that have prevailed in 2020 count as “acute”. In fact, this year has already seen more three-sigma cross-asset moves than all of 2008 combined.

Of course, the suspension of market rules and the subjugation of price discovery to concerns about stability is a controversial topic. There were critics post-GFC and there are critics of the Fed’s recent actions too. Criticism is usually couched in moral hazard terms, and the discussion is often spiced with hyperbolic rhetoric about the purported inevitability of hyperinflation.

Kocic describes how central banks establish what amounts to martial law, and how normative concerns are relegated to the background out of necessity. To wit, from his latest:

In the case of the last two financial crises, policy response in both cases has been articulated as the state of exception: “Traditional rules and norms of the market were suspended for the purpose of self-preservation with central banks acting as “the sovereign”. The markets continue to function while the rules withdraw. Central banks rise above the normative constraints of the free markets and decide about their validity. They are the subject taking the ultimate decisions, other rules become only antechambers of their power. These decisions free central banks from all normative ties and they become the ultimate rule that governs the markets.

One key feature of this environment is that market participants willingly surrender. Notwithstanding cat calls from some “brand name” fund managers and dire warnings from online commentators who no one on Wall Street takes any semblance of serious, there is no real “will to oppose” this power – that is, there is not a rebellious groundswell from market participants.

That harkens back to the idea of “smart power”, which Kocic has discussed previously. The following passage is from a 2018 note:

Power, in its traditional restrictive form, is an ineffective way of imposing a rule – its influence can be only temporary, it always encounters resistance. “Smart” power, one that aspires to be effective, cannot be restrictive; it must be permissive in order to eliminate a possibility of resistance. It should operate seductively and not repressively — it has to say “yes” more often than “no”. By the same token, smart power has to be a “good listener” calling on us to confide and share our preferences… Through their communication with the markets, central banks, and the Fed in particular, have become “good listeners” with their decisions and actions made with markets’ consent. After years of this dialogue, the markets have gradually surrendered to the ever shrinking menu of selections that converged to a binary option of either harvesting the carry or running a risk of gradually going out of business by resisting. Not much of a choice, really.

Of course, this can go “wrong” if central banks decide to cut the market out of what, over time, becomes something of a feedback loop. In 2018, for example, Jerome Powell arguably revoked the market’s license to co-author the policy script, and the result was a steep selloff by the end of the year.

[As an aside, Kocic repeatedly suggested in 2018 — and I use “suggested” because he doesn’t have Deutsche’s official house call on equities — that the S&P might close the year between 2,300 and 2,400. That ended up being more accurate than any equities strategist that I’m aware of, something I discussed at the time, and Bloomberg later took note of.]

Another, more fundamental, aspect of the “state of exception” is the understanding that, eventually, it will be lifted. This is the only way to resolve the contradiction inherent in the notion that market laws must be suspended in order to restore normal market functioning.

This time, it would appear that the market is starting to come to terms with the idea that the “state of exception” is permanent. Kocic discusses (and illustrates) the point.

In the past, “this state of suspension of traditional rules of yield curve dynamics is expected to be temporary [and] the options market expresses the view of the horizon over which the market would normalize”, he writes, noting that “the long dated ratios generally remain stable despite collapse of the short dated ones”.

What you want to focus on in the left pane is the red line (the 5Y vol ratio). You’ll note that the ordering of the lines (and I’m speaking colloquially now so that readers can follow along) in the left pane is consistent with past experience, but, as Kocic writes, “until 2020, the 5Y vol ratio has never declined meaningfully below 100%”. The red, dashed line in the left pane shows you the current level.

(Deutsche Bank)

This is a potentially meaningful development, and you can see it clearly when you look at 5Y2Y/ 5Y10Y in isolation (right pane above).

Kocic spells it out as follows:

The loss of the bottom of the 5Y ratios, their decisive and swift decline well below 100%, is indicative of something new — market’s skepticism that rates will normalize any time soon, if at all, that the traditional dynamics of rates cuts and hikes as the essence of monetary policy will not return in the foreseeable future.

Viewed in the context of the “state of exception”, and particularly the implicit promise that it will one day be lifted in order to resolve its inherent contraction, we have entered new territory. Or, if we’ve stepped into this territory before, we’ve never ventured as far as we have in 2020.

In 2017, Kocic noted that “engineering a state of exception comes with considerable risk”. Over time, he remarked, the suspension of normal market rules can cause “traditional transmission mechanisms [to] atrophy”. Investors’ attitudes and habits might change “irreversibly”, he said.

When that becomes the case, unwinding stimulus (lifting the “state of exception”) is difficult. Even as the “sovereign” (i.e., the Fed) wants to emancipate the market, disowning power becomes all but impossible.

“The only way to avoid facing the underlying dilemma is to never give up the power”, Kocic said, three years ago, on the way to suggesting that eventually, this would lead to “a new status quo”, which he called the “permanent state of exception”.

Fast forward three years, and here we are.

As ever, it is impossible to paraphrase Kocic in a way that enhances his exposition, and attempting to do so risks diluting it, so I’ll simply leave you with a trio of short additional excerpts from his latest, which I’m sure readers will agree are exceedingly brilliant and incisive. To wit, from Kocic:

We have been there before but not with this level of conviction. In the last decade, the state of exception was in place for almost seven years, and we saw how difficult it was to re-emancipate the markets after that, how reluctant the markets were to accept their own normalization, and how short lived that emancipatory state was. Current extension of the normalization horizon is a function of both the last decade’s experience as well as a recognition of the depth and non-linearity of the present crisis.

With every new crisis problems have become deeper and more difficult to manage. They pile up on top of the unresolved problems from previous crises forming an accumulated residual which, with time, erodes market’s ability to recover. As a consequence, new crises become increasingly more difficult to manage requiring an ever more extended accommodation and heavier handed policy intervention. This in turn diminishes market’s ability and/or desire to re-emancipate itself and to function on its own, producing the reinforcing loop between market’s “apathy” and Fed’s addiction liability.

The way the markets are pricing the evolution of the current crisis in combination with the policy response no longer looks like a state of exception, but as a new rule which is here to stay for an extended period of time.

I am betting that I am not alone in noticing the parallel in Kocic’s vision of permanent exception to the rising trend of autocracy we are seeing in the political universe .. The reactions of the public in that sphere are similar to what is described in this post……among investors in the financial sphere ….

I see it differently.

In the political sphere, in ‘normal’ times, people are content enough and politics is generally genteel/democratic, though it doesn’t make much of a difference since things only change at the margin.

In times of stress, people aren’t comfortable or content. They’re therefore more willing to explore extremes/radical solutions. We don’t have that many data points since the advent of modern capitalism but, when it comes down to either “blame the rich” or “blame the poor/the immigrants” for our problems, it seems the “blame the rich” side of the polity never quite manage to grab power. The “blame the poor/the immigrants”, otoh, is often a rioting success – and it leads to authoritarianism.

I wish I had hope.

Agree with you as well….In my case I was referring to the more and more radical solutions to problems that have a tendency to be unidirectional over a longer time frame….

An interesting point. While I agree with you, H, and Kocic about the ability of the “listeners” to passively accept the normalizing of exception, both in Hitler’s Germany and in Communist Russia the public finally seemed to realize it had been conned and said enough. Hitler never gave up on his version of normalcy and lost everything. Putin is not quite so dumb, it seems, as he seems to have found the new version of reality most will put up with, and created a new uber-rich group of oligarchs to rally round. While we’re not quite ready for revolution yet, it’s not impossible to imagine. Spoiler alert, I don’t think Trump’s the leader; he’s the catalyst.

Tremendous piece H, among several of your very best the last few weeks. I tend to ascribe my views on power to a mostly Foucauldian perspective. The subject of both the discursive and non-discursive norms being created by this dynamic going forward are worth deep analysis and equally deep consideration given the new “truths” it is creating. Kocic’s work implicitly points at some fascinating elements of what something like that might look like in just the few quotes noted above. Perhaps a future topic for Bjarne or someone else…

The most enlightening conversation I had in college was with Foucault in 1982. He would be having a field day today, as I expect you are given your Foucauldian perspective on power! I’ve never seen such a highly charged moment with scientific, social, economic, and political norms all very much in play. How disease prevalence, climate change, racial injustice, debt monetization, wealth and economic inequality, and individual rights across most of the globe are discussed six months from now will be the outcome of power struggles between, within, and transcending international borders that are potentially epoch-making.

State of exception… hope. Permanent state of exception…denial.

A thoughtful article. I have tried to read everything I could about the 2008 banking crisis. As far as I can tell it was greed. The original response by Bernanke was appropriate, as far as I can tell all the QE’s that we’re done after that we’re inappropriate. Now the market telegraphs its intention by pulling back 5-10% and than the Fed jumps in to save the day. Now we are at the market is no longer being used for true price discovery.

2008 sub-prime was a $450bn market and pretty much almost took tge world down. The Fed could have taken it all down and avoided the carnage. They could have backstopped the “Inv Grade” portion and avoided it. Their bal sheet was $700bn in 07. 2020 look at the amounts they have done. Bal sheet now 10x to $7tn.

The problems never get solved. Money printing doesn’t solve problems, just paper over them.

Education problems, security problems, lack of investment problems, inefficient “investment”, and in and on are the problems. Fed printing will not solve them. Future Chairs will have bigger problems to deal with.

In other words “we are screwed”. We are Japan on the way to Elvis. There is no turning back, we are in too deep.