The macro docket’s pretty light in the US this week, where that means the only scheduled release with the potential to move markets is Thursday’s personal income and spending report.

It goes without saying that the accompanying update on the Fed’s preferred price metric won’t be favorable in the context of the Committee’s 2% price stability goal. Simply put: Inflation ran hot last month, and not just because of the war, although that’s obviously a big part of it.

But it’s all relative in the 2020s. I think, by now, we’ve all come to expect that annual inflation’s going to run closer to 3% than 2%, and that’s during periods when we’re enjoying a reprieve from the rolling supply shocks that’ve characterized this decade.

Consensus sees a high 0.3% (or, at worst, a low 0.4%) from the MoM core PCE price print this week. On a YoY basis, core price growth probably ran 3.3% in May for a second straight month.

As the figure reminds you, the MoM prints need to be more like 0.13% if we’re actually trying to get back to something like a pre-COVID YoY rate for core PCE price growth.

I reckon I’ve beat up on Kevin Warsh enough by now, but I can’t help myself. Because when people say things like “…his tone at the news conference seemed notably hawkish to us” (from Bloomberg Economics), it strikes me that the vast majority of market participants are naive, inclined to give Warsh the benefit of the doubt or both.

If there’s a monetary policy solution to the kind of inflation we’re witnessing in this century’s Roarin’ 20s (and I’m not sure there actually is), it’s not awkwardly-worded reiterations of the Fed’s commitment to price stability, it’s not equivocation masquerading as directness and, forgive me, it’s not a goddamn “task force” with an unspoken mandate to find a “better” inflation metric.

I understand and respect that for a very long list of reasons, not all, or even most of which, have anything to do with Donald Trump, this isn’t a tenable option, but let’s not kid ourselves: Even in the context of consumer price growth driven by supply-side factors beyond the Fed’s control, the FOMC can bludgeon inflation back down to 2%. Or even lower. At least temporarily.

If Warsh hiked Fed funds to, say, 10% between now and year-end, I’m pretty sure the accompanying hit to demand — as lower-end consumers lose access to credit entirely, the middle-class starts missing payments on variable-rate debt and the upper-half of the so-called “K” sees their equity wealth haircut by 30% — would cool things off in a hurry.

So think about that when you consider Warsh’s ostensibly “ironclad” commitment to price stability. And let’s not forget: You don’t have to go back to Paul Volcker to find a Fed chair who implemented draconian rate hikes over a compressed time frame. You just have to go back to the guy who was Fed chair last month.

Of course, any rate hikes Warsh dares endeavor (and I don’t think he’ll brave any) will be from a much higher departure point for Fed funds compared to Powell. Having readily acknowledged the apples-to-oranges nature of the comparison, and having thus tacitly copped to a kind of intellectual dishonesty, I’m free to be abrasive: Let’s see if Mr. “Unambiguously And Unanimously” committed to price stability come hell or high TruthSocial tirade hikes rates by 525bps during any stretch of his tenure.

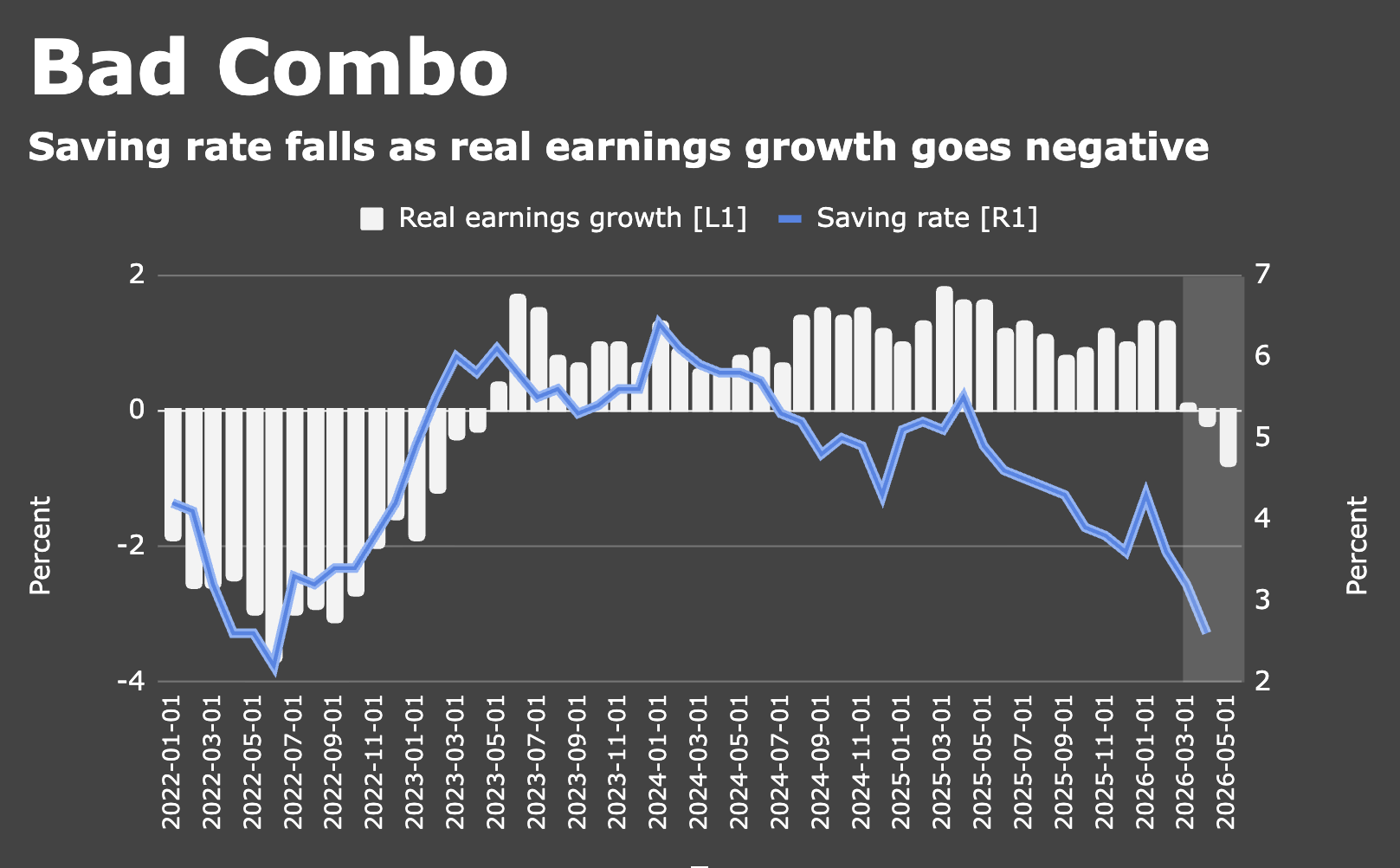

Anyway, the personal income and spending report will include an update on the saving rate, which is a hot topic right now. Recall that it fell to 2.6% in April, among the lowest readings on record if you exclude the lead-up to the GFC.

If the saving rate falls further, bears will shout that the end is nigh. Ironically — and this really can’t be emphasized enough — it’d be even more concerning if the saving rate rises, as that’d be a more urgent canary for consumer spending.

Speaking of consumption, consensus expects personal spending in Thursday’s release to show a 0.5% nominal gain for May, while incomes are seen posting a 0.3% advance. Note that when adjusted for annual CPI inflation, wage growth’s been negative for American workers since March.

Also on deck in the US: New home sales, the final estimate of Q1 GDP and the final read on University of Michigan sentiment for June.

Fed speakers include John Williams and Neel Kashkari. Given Warsh’s aversion to forward guidance, I assume officials will be encouraged to avoid making forward-looking statements during public speaking engagements. At least until the stock market sells off, at which point Warsh will either “guide” or be charged with mortgage fraud.

I’m just kidding. Or not.

{kind=link}

Every time I read the term “task force”, I immediately think of a magician’s trick using “distraction/art of misdirection”.

Exactly.

As you note I as well am a bit astounded by the media embracing the freshly minted “Fed Hawk.” I recall Van Jones losing all credibility at Trump8s first SOTU. He said following February 2017 address to a joint session of Congress, CNN commentator Van Jones said: “He became President of the United States in that moment, period. That was one of the most extraordinary moments you have ever seen in American politics, period.”

Gundlach and PIMCO are both saying to buy the 30. I guess it’s your money, go buy longs.

If he loses his preferred candidates in the midterms and is looking at a miserable 2 years under attack, he might contenance punitive rates as a lesson to us all.