What if the neutral rate’s higher now?

R-star’s an esoteric topic, but it was front and center in the macro debate during 2023, as the US economy remained resilient in the face of what, ostensibly anyway, were very restrictive monetary policy settings.

The implication of a higher neutral rate is that policy isn’t as restrictive as you’d be inclined to believe simply by looking at Fed funds, which is of course much lower today than it was the last time real neutral was in the news.

The figure above shows three Fed models of the neutral rate. In order to get nominal neutral, you add 2% (the inflation target) to a given model’s current estimate of the real neutral rate. On that score, the Fed’s only restrictive on the HLW model, which is the most famous.

This is a subject Kevin Warsh probably doesn’t want to address. Because if neutral’s higher, then cutting rates to appease Donald Trump risks overheating an economy that, in aggregate anyway, is perhaps performing a little too well given upward pressure on inflation.

As BMO’s Vail Hartman remarked on Thursday, all of Bloomberg’s so-called “surprise” gauges for the US — i.e., indexes which track over/undershoots versus consensus — are trending upward, implying data across all categories is beating estimates consistently.

“A simple moving average of [the growth, inflation and labor market indexes] is tracking just off the two-year high print seen in late-May [and] has tracked in positive territory since January,” Hartman wrote, in the same note, adding that “the upside surprises and overall resilience of the data offer the Fed the flexibility to shift its attention towards the inflation side of the dual mandate.”

That is of course if they want to. And “they,” as a Committee, certainly do. Just ask the April FOMC minutes.

For reference, market pricing still reflects better-than-even high odds of a hike by year-end. Ironically, peak hawkish pricing was achieved the day Warsh was sworn in.

Notwithstanding his “I’m no sock puppet!” assertions, Warsh is under immense political pressure from The White House to cut rates early and often, and I can only assume he’ll try his best to accommodate Trump.

That, despite elevated inflation (even on Warsh’s preferred “trimmed mean” measures). If the neutral rate’s higher, rate cuts will be an even dicier proposition.

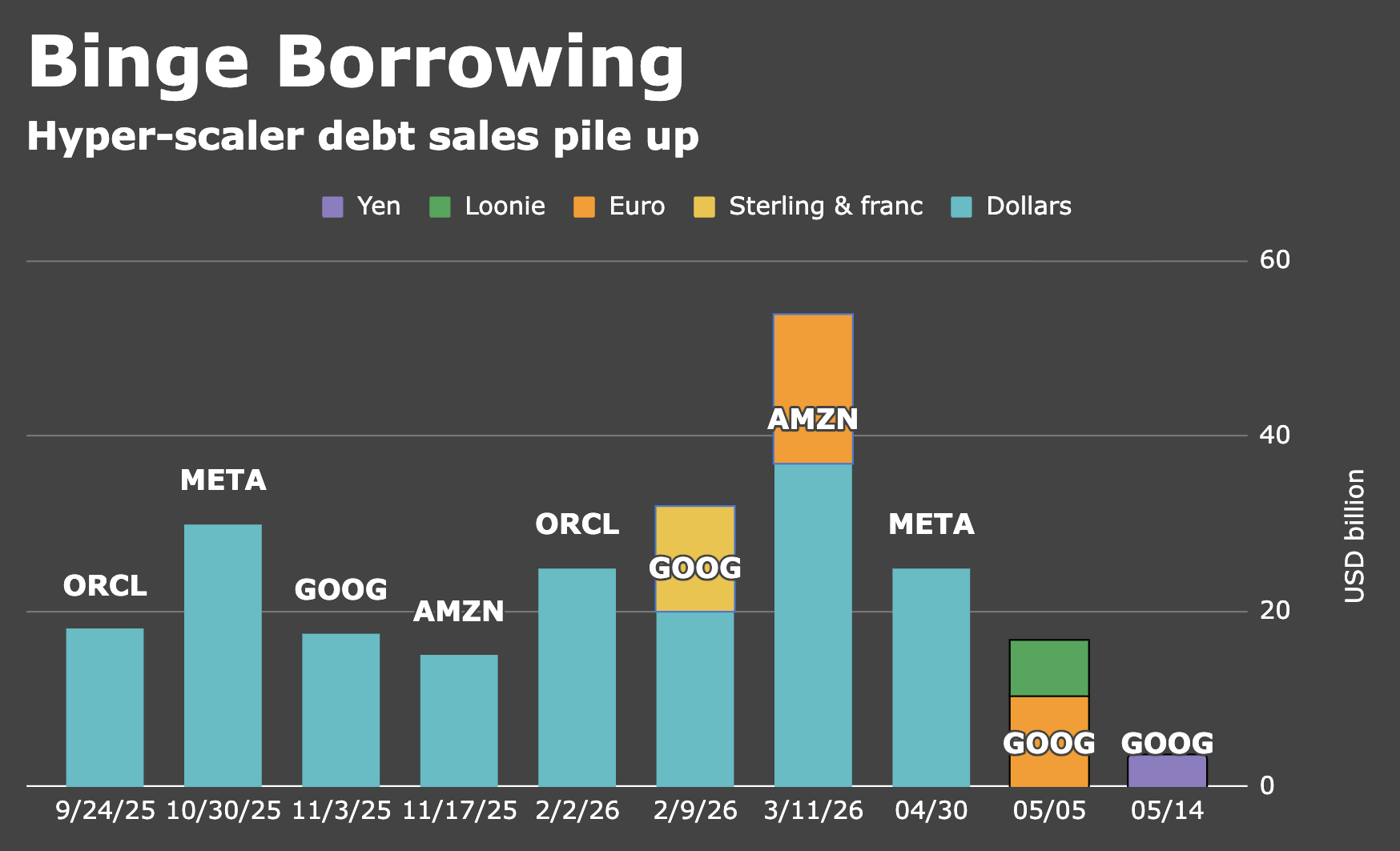

As Bloomberg’s Cameron Crise pointed out, the last time there was a “secular investment boom” like the one we’re witnessing currently with the AI buildout, r-star moved up.

The figure above shows you nonresidential investment as a share of GDP. After rising at a ~10% clip in Q1, it’s the highest since the dot-com bubble, and could well keep climbing.

“The AI boom has a created a thirst for capital,” Crise remarked, citing hyper-scaler bond issuance, big IPOs on deck and Alphabet’s massive equity raise. “That has very likely pushed up the neutral interest rate once again.”

In the same note, he illustrated what he described as “quite a strong link between trends in investment and monetary policy” using five-year percentile rankings for the share of business investment to GDP and Fed funds.

The figure above, from Crise’s piece, shows you the link.

When you “look at each factor relative to its own history… there is generally a nice little relationship,” Crise went on, noting that periods where the two diverge eventually end with policy tightening.

“The ancillary signaling from financial markets” in the presence of the new capex boom, Crise said, “suggests effective policy has become easier.”

Meanwhile, various measures of financial conditions reflect extremely loose conditions, credit spreads are near the pre-GFC tights and US equities are trying for their longest weekly winning streak since — checks notes — 1985.

{kind=link}

Thanks for this. I had forgotten all about r*. If it is indeed higher that would explain a few things. I know Powell was never a big fan of that metric, but now that massive corporate capex and borrowing are acting essentially like government stimulus, r* may be more relevant than ever. The problem is — as Powell used to point out — it can be very difficult to measure accurately in real time.

Glad you liked it. This was a stick-save article that turned out well. I was sure (sure) I was going to be able to close today with a selloff piece, but this just isn’t a tape that wants to sell off.

I think you’ll get that opportunity today.

A colleague helpfully sent around a breakdown of datacenter construction costs. He estimated that the electronic gizmo portion represented 60%.

In the context of your article, I wonder what portion of that 60% is being spent on imported gear. GPUs, memory chips etc. The most expensive stuff relative to steel racks, electrical wiring and such. Might that help explain why the inflationary impact of that capex is surprisingly muted?