Nothing to see here, just a double-digit plunge in fixed investment across the world’s second-largest economy, the fifth straight decline and the worst 10-month result on record.

It’s hard to find something nice to say about Friday’s top-tier data out of Beijing, where Xi Jinping’s apparatchik number crunchers said FAI through October shrank 1.7%, led lower by what’s now a 15% YTD contraction in property investment.

(If you were wondering whether the property bust is still dragging on the Chinese economy, there’s your answer.)

As noted, that 1.7% YTD contraction for the headline FAI readout counts as singularly poor and strongly suggests recent stimulus measures are both badly needed and, to the extent they’ve been enacted, ineffectual.

The figure above excludes 2020 and 2021 because the size of the plunge in early 2020 (at the onset of the pandemic) and the surge in early 2021 (as the figures lapped the 2020 comp) are hard on the eyes. For reference, the YTD, “through October,” tallies for those years were +1.8% and +6.1%, respectively.

The NBS didn’t mince words. China, officials dryly remarked, “is facing quite a few challenges” and they aren’t confined to the “external environment,” which the Party habitually (and, to be fair, quite aptly) describes in conspiratorially foreboding terms.

On the home front, China’s central planners are grappling with “rather big pressure” as the Party endeavors to rebalance and restructure the economy, an effort hobbled by what, during some months, looks like hopelessly moribund domestic demand (it’s no more “resting” than the Norwegian Blue parrot was).

Speaking of domestic demand, the lackluster fixed investment figures were accompanied Friday by the slowest YoY retail sales growth since August of 2024. 2.9% marked a fifth straight decline in the annual growth rate. The figure below also shows industrial output which, like retail sales, posted the slowest YoY growth of 2025, at just 4.9%.

Note that retail sales growth has lagged IP growth in 21 of the last 22 months. That’s not just “a problem” for a country trying to mark a transition to a consumption-led economic model, it’s evidence of failure.

Friday’s data completes an unfortunate picture of the Chinese economy in October when, you’re reminded, export growth unexpectedly slammed into reverse.

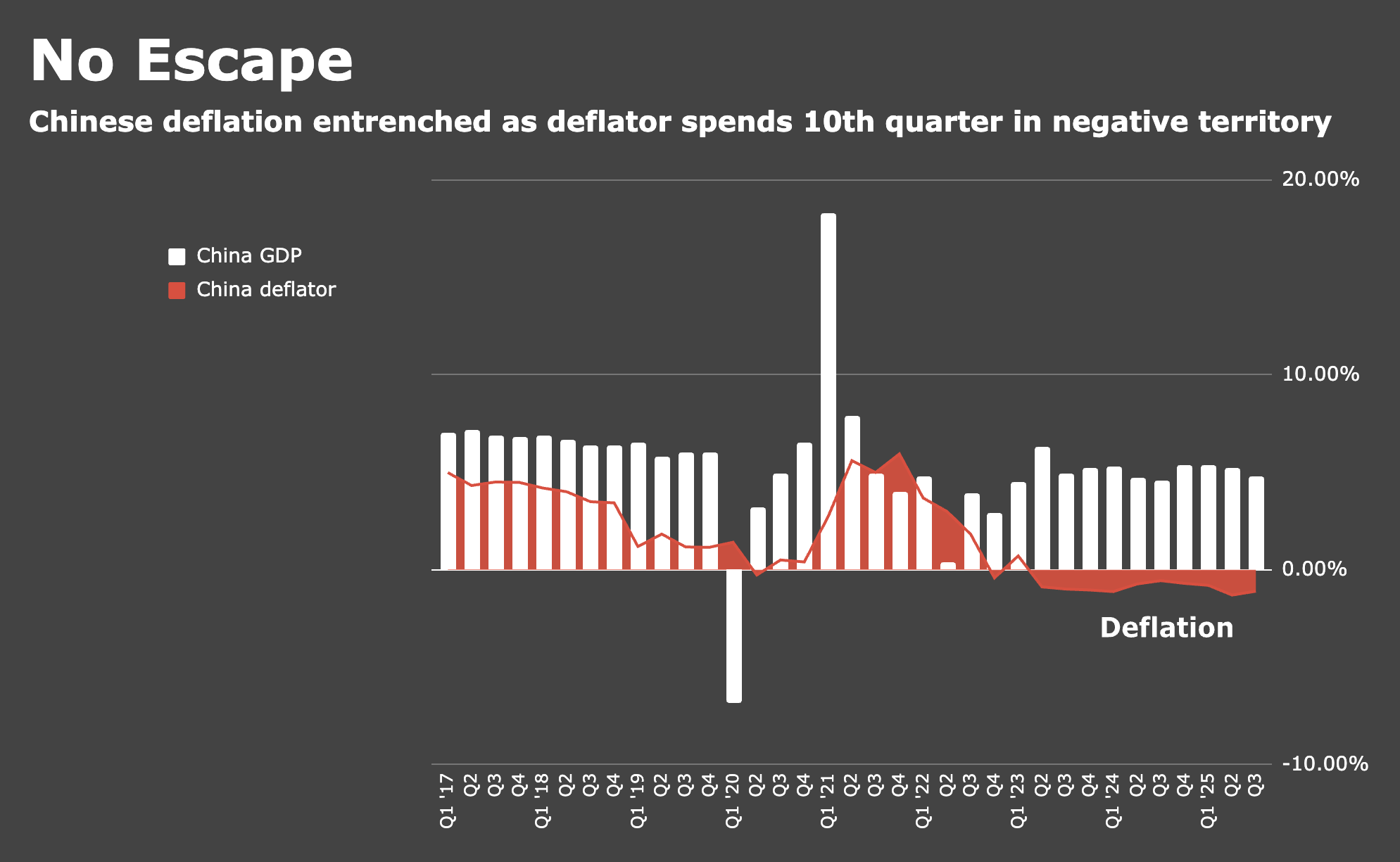

With the caveat that Beijing’s going to hit this year’s growth target — even as savvy observers know to take the headline real GDP figures with a grain of salt given the deflator’s been negative for two and a half years (!) — it’s difficult to escape the notion that China’s suffering from policy failure after policy failure.

However well-meaning, Xi’s “COVID zero” strategy and “common prosperity” social engineering push together served to torpedo consumer sentiment, and the Party spent the last two years pushing on a string to stave of a deflationary balance sheet recession. The legacy of Xi’s property curbs is a never-ending slump in investment, and it looks like the Party doesn’t have any great ideas to stanch the bleeding there either.

It’s not a disaster by any stretch, but it’s kinda sad all the same. Most of this malaise is directly attributable not to one-party rule necessarily, but rather to one-man rule.

China had a pretty good thing going: Inherently contradictory or not, communism with a dash of capitalism and political oppression with a tinge of economic liberty, was working out. And the rest of the world was willing to look the other way on one-sided trade as long as the Party pretended to liberalize. Then they pivoted (back) to totalitarian dictatorship under Xi and here we are.

The Chinese economy’s probably too large to ruin by now, but Xi’s demonstrating a remarkable adeptness at making things harder than they need to be. And for what? The posthumous glory of a 50-years-dead dictator who purged Xi’s father.

{kind=link}

H-Man, trying to manage 1.4B people in the same space as the U.S. is quite the task, while Xi’s economy is not resting maybe it is just tired.

It’s all tuckered out after a long squawk.

Look, I took the liberty of examining that parrot, and I discovered that the only reason it had been sitting on its perch in the first place was that it had been nailed there.

Those numbers need to be adjusted for population growth – slightly down since 2023 – and the aging of the population – older people don’t buy much. Maybe the growth level is sensible and even properly managed.

John, nominal growth’s outstripped real growth for 10 quarters in a row. They’re in deflation. And how does one go about “adjusting” retail sales for age? Smartphone sales of CNYwhatever billion were actually > CNYwhatever billion after you control for more old people? I mean, I get what you’re driving at, but I’ve been listening to people tell me that China’s not stuck in a rut for two years and the implied deflator’s been negative every single quarter for that entire period.

“China had a pretty good thing going: Inherently contradictory or not, communism with a dash of capitalism and political oppression with a tinge of economic liberty, was working out. And the rest of the world was willing to look the other way on one-sided trade as long as the Party pretended to liberalize. Then they pivoted (back) to totalitarian dictatorship under Xi and here we are.”

That’s exactly right. I remember thinking they had created a new “hybrid” that held an unfair advantage over traditional capitalism.