I’m avowedly not a Michael Burry fan. Most of you know that.

He’s crazy, and in some respects good for him. The kind of crazy Burry is can be conducive to genius, and indeed there’s a strong argument to be made that most geniuses are some stripe of crazy. Being a genius, in turn, can be conducive to the acquisition of large sums of money. It’s thus no coincidence that Burry’s very rich. Another thing geniuses tend to be (in addition to crazy and rich) is depressed, and I’d argue Burry’s that too.

I speak from some experience here. I’m not nearly as crazy as Burry or Elon Musk or, say, Kanye West, but I am crazier than most people.

I’m also a genius compared to most people (but certainly not compared to Burry, West or Musk). Not coincidentally, I’m better off financially than most people (but not properly rich, let alone Burry-style rich, to say nothing of West, a billionaire, and Musk, a centibillionaire on his way to trillions).

I’m also depressed, but not the sort of depressed that manifests in bizarre behavior like that which next-level geniuses often exhibit. (Burry’s behavior is erratic and although he turned out to be correct, his bets against US housing during the subprime bubble were nevertheless akin to something one might conjure during a manic episode. West suffers from acute bipolar disorder. Musk is — I don’t know. Something. Else. Elon’s something else.)

I say all of that to say this: Burry operates in a realm (the world of stock investing) that’s not as amenable to the peculiarities of eccentric genius as, to keep with the West and Musk parallels, music and entrepreneurship. If Kanye West weren’t crazy, we wouldn’t have My Beautiful Dark Twisted Fantasy, nor The Blueprint, nor DAYTONA, three of the greatest albums ever conceived. If Elon Musk weren’t crazy, we wouldn’t have Tesla, SpaceX and whatever’s next.

Much as I despise the two them, West and Musk, by virtue of the unique interplay between mental illness, creativity and their respective scopes of interest, will continue to amaze us until their dying days even as they disappoint and disgust us at regular intervals. By contrast, long-term success in the world of capital markets isn’t generally a function of eccentric genius, or any sort of genius at all. If you look at modern history’s best traders, they’re not geniuses in the Michael Burry sense of the term. Paul Singer’s a sort of genius, but not that sort. David Einhorn’s a genius, and a different sort than Singer, but not the sort that Burry is. I could go on. Stan Druckenmiller and David Tepper aren’t geniuses at all, or at least not as far as I’ve ever been able to tell.

People like Burry thrive as creators. Artists. Entrepreneurs. Writers. And so on. You can’t “create” a short case. I mean, you can, but the methods for generating a short that wasn’t there already are generally illegal. Rather, you have to find good shorts, and the fact is, they’re few, far between and tend to be small potatoes.

Yes, Burry’s genius helped him ferret out “The Big Short,” proper noun. The grandaddy of them all. But while West can create more awe-inspiring modern symphonies between extolling the many virtues of the Third Reich, and while Musk can (hopefully) reconcile quantum mechanics with relativity in the service of making interstellar travel a reality between dog-whistling to white supremacists, Burry can’t conjure new “Big Shorts” between sometimes irritable social media posts he later deletes.

On Tuesday, Burry was in the headlines for accusing the hyper-scalers of fraud. Maybe he wouldn’t put it that way, but it’s hard to understand his allegations as anything other than… well, than allegations.

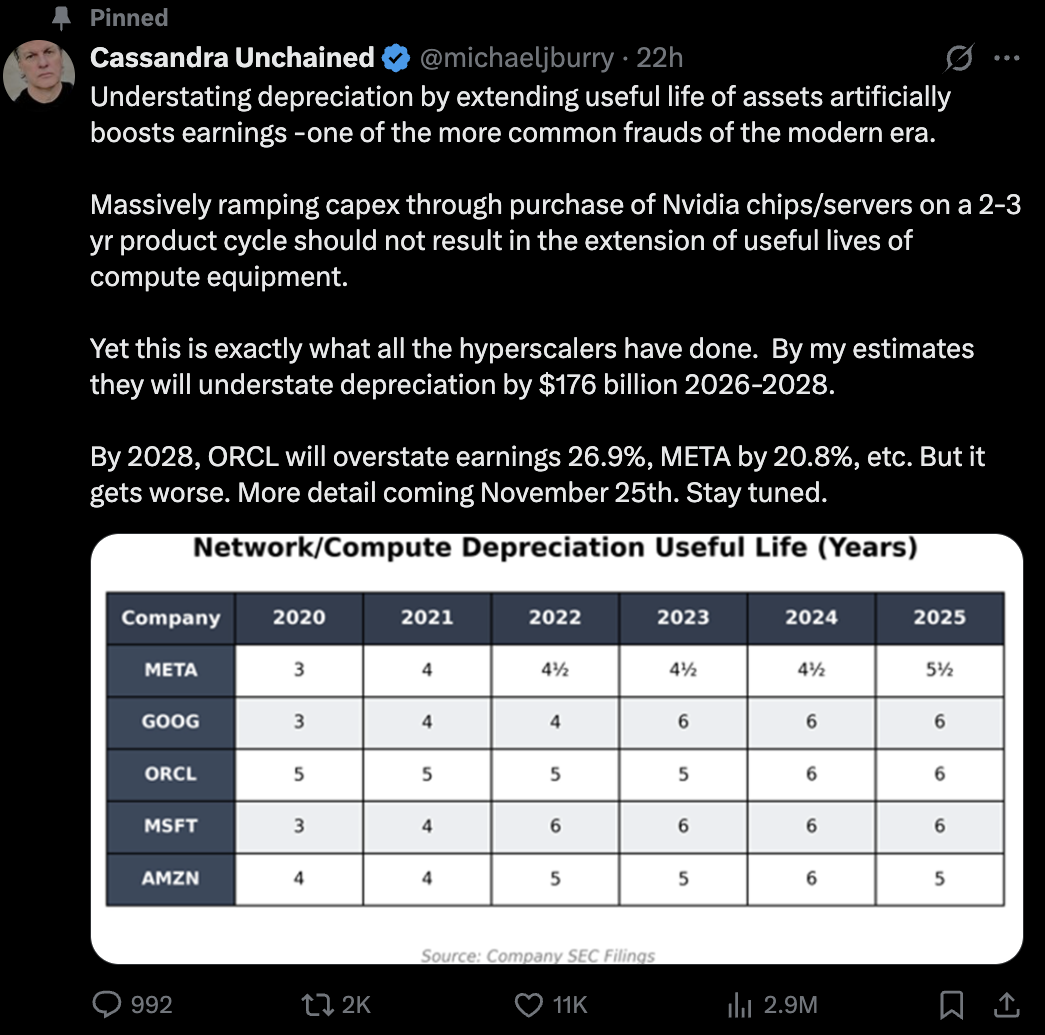

“Understating depreciation by extending [the] useful life of assets artificially boosts earnings — one of the more common frauds of the modern era,” he wrote, in a post accompanied by a hyper-scaler depreciation schedule.

“Massively ramping capex through [the] purchase of Nvidia chips/servers on a two- to three-year product cycle should not result in the extension of useful lives of compute equipment, yet this is exactly what all the hyper-scalers have done,” he went on, in the course of suggesting that Alphabet, Amazon, Meta, Microsoft and Oracle “will understate depreciation by $176 billion” from 2026 to 2028.

He singled out Oracle and Meta which, according to Burry, “will overstate earnings [by] 26.9% [and] 20.8%,” respectively by 2028. “It gets worse,” Burry wrote, teasing “details” he plans to reveal on November 25.

A few things. First, modern history’s most famous short-seller has just publicly accused the world’s most important companies of fraud, a pretty bold step given those companies’ litigation budget is unlimited.

Second, Burry seems to believe this analysis is somehow akin the epiphany he had in 2006/2007 while parsing MBS at the individual-loan level. It’s not. Everyone with an MBA (and that’s a lot of people) is aware of the potential for this type of “fraud.” Note the scare quotes. It’s famously difficult to prove. Except in egregious cases, this is a subjective judgment, and while there may come a day when it’s black and white, we’re not there yet and even if we get there, someone would have to prove intent.

Third — and this isn’t an accusation, it’s just a little comic relief — of course there’s some of what Burry’s describing going on in the current environment. There’s a “wink-wink” argument to be made that you’d be derelict to shareholders if you weren’t fudging this a little bit because, again, it won’t be provable.

Maybe what Burry means isn’t that these companies will be taken to task legally, but rather that the inevitable result of this alleged “fraud” will be a stock crash as investors come to terms with the pervasiveness of these (again, alleged) shenanigans among companies which comprise ~40% of benchmark market cap. If that’s the argument, I buy it, but it’s entirely unoriginal. The idea that Burry’s the first person to suspect this is laughable.

At the end of the day, it’s difficult to escape the sense that Burry’s burdened by his own genius and, more to the point, that the “Big Short” is a curse for him. Everyone’s waiting for Burry to find the next one, but unlike geniuses in other fields, he can’t will an encore into existence. It’s either there or it isn’t, and in the case of the hyper-scalers, I think he’s mistaking their bubble-like valuations for the sort of universal blind eye dynamic that typified US housing ca. 2006.

Everyone’s aware that we’re likely experiencing a bubble in AI-related stocks. Whatever Burry’s going to say in the days, weeks and months ahead isn’t going to be new, nor will it be news to anyone who follows the space. No one other than Burry (not even the people who packaged MBS) went line by line through pre-GFC mortgage securitizations. By contrast, the companies he’s accusing of fraud are the most heavily scrutinized, widely covered corporates in the history of capitalism.

All of that said, I’d be remiss not to note that there is a parallel between the counterparty risk on Wall Street exposed in 2008 and the interdependence inherent in the self-referential web of deals at the heart of the AI hype cycle. If the whole thing implodes, that’ll be why.

{kind=link}

Whew.

I recall when Zuck announced Meta’s shift to longer term depreciation of servers on their quarterly call a few quarters back, and not a single Wall Streeter blinked. I thought it a yellow flag, because protestations to the contrary he admits that earnings are being managed. Burry’s just using inflammatory language to describe common corporate behavior. I do believe Meta and Oracle bear watching in this respect, as both are investing beyond their means. Blue Owl/Meta’s SPV to offload capex from Meta’s balance sheet is another clear signal.

Has anyone estimated the hyperscalers’ AI profits vs their AI capex, for a rough EBIT/capex ratio? I tried this for AMZN and got, with lots of handwaving and licked finger in wind, a guesstimated EBIT/capex of about 3.5%. 1/0.035 = 28.6. So why does it matter if the useful life of an AI GPU is 3 years or 6 years?

Seems Burry just following standard short seller procedure – Dump and Pump, no? Maybe he can move the market just a little enough to capture a sizable trading profit…but, really, isn’t this depreciation thing just another can that can be kicked down the road for a long time and never really matter (perhaps until someday it does – but, when? Just like our Federal Government deficits…).

That’s not Burry. Even if he could move these names with a tweet (he can’t), he doesn’t care about making a few million bucks on a short. That’s kinda the whole point of this article. Burry’s chasing the unattainable: An encore to history’s most famous short.

Excellent insight Mr. H. Burry is more interested in cementing his legacy as one the all-time best short sellers. He isn’t interested in a few million from volatility by headlines. If and when the AI bonanza fizzles, the cracks will likely appear first where we see the froth coming out quickly already: the companies with the weakest balance sheets incurring more debt, and/or a nebulous path toward sustained AI profitability. The recent price action of Oracle, Coreweave, Meta, tells that story.

Honestly, I’d choose to follow someone, who is all about the money; than someone who is all about the notoriety. At least, I’d know what I was following.

Still running the home streaming server on 10 year old plus HDD, depreciate that Burry!

Jim Simons. Mathematician. Hedge fund manager. Investor. Philanthropist.

1976 Oswald Veblen Prize in Geometry. Elected to the National Academy of Sciences in 2014. Code breaker. Renaissance Technologies.

yup, was surprised to not see that name in the roster, but more isn’t always better.

Burry is far from the first one to cry foul about AI capex and depreciation – on the contrary, this seems to be fast moving towards the consensus view.

Also, if we are in a bubble, it is in its very embryonic stages, and likely not contained in the big end of town. They are far from cheap as a basket, and far from truly bubbly valuations too.

Sigh, two days late so no one will read this, but I do believe there’s a different dynamic to watch for regarding depreciation. Hyperscalers pay $40K – $55K for current GPUs. When a manufacturer (Apple) defines the “expected” lifetime of a technology (laptop) and there are over 100M customers, the manufacturer prevails in the discussion on depreciation timing, because the market is liquid. When the individual deal size for a product (GPU) is $10B+ (quantity 10K+ of chips), and there are only 10 customers in the industry (that matter), then the customer prevails in the discussion because the market is not liquid. If the hyperscalers say they are going to use those chips for 6 years (following initial buildout), then the market structure dictates that they can have their way, and subsequent tech may be relegated to a high-performance niche for some time. So the risk is out-year under-performance by NVDA, not “fraud” by the hyperscalers.