Surprise! Existing home sales in the US fell far more than expected last month, according to Wednesday’s sole notable US macro release.

The 3.93 million annual rate tipped by the NAR’s monthly update counted as the slowest since September and represented a 2.7% drop from the prior month. Consensus expected a much shallower decline.

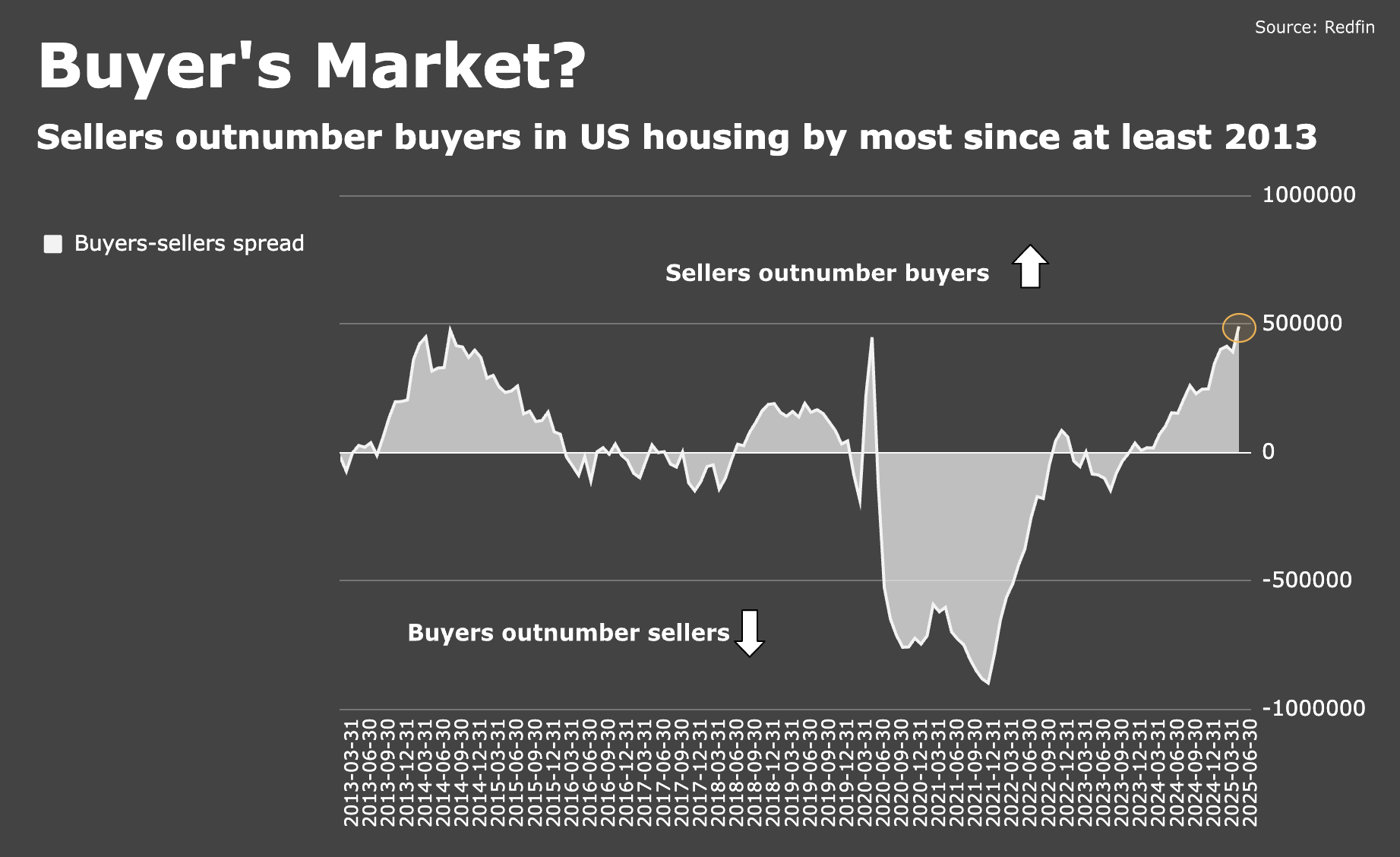

As the figure below reminds you, this situation’s disconsolate. The resale market suffered a brake-slam moment when rates took off and it’s been frozen since.

Sales were down in every region except the West, where they rose “modestly,” to employ the NAR’s adjective.

There’s no mystery here. “High mortgage rates are causing home sales to remain stuck at cyclical lows,” NAR Chief Economist Lawrence Yun said Wednesday, adding that if only rates fell closer to 6%, more than 150,000 current renters could realize the American dream.

There’s just one problem with that: The average 30-year fixed just hit a four-week high at 6.84% on the MBA’s gauge.

84bps (the distance from current levels to Yun’s hopeful scenario) may not seem like a lot, but it is. That kind of decline would generally be associated with a rip-roaring rally in 10-year US Treasurys. It’s hard to see that happening outside of a growth scare which, while eminently possible, could blunt the home-buying impulse if it’s accompanied by (or defined by) a sharp deceleration in hiring.

Recall that mortgage rates fell ~110bps from April to September of last year, but more than half of that drop occurred from early August 2024, which is to say ~60bps (give or take) was attributable to the false-alarm growth panic which at one juncture found traders wagering on an emergency, inter-meeting Fed cut.

Although there are ostensible parallels between this summer and last, that kind of shock isn’t especially likely to repeat itself. And, to reiterate, even if it does, the accompanying macro angst could offset rate relief for the purposes of home-buying activity.

Anyway, the median home price in Wednesday’s NAR release was $435,300. That looks like a new record to me, and it counts as the 24th straight YoY gain.

For context, the median price this time four years ago was $366,900.

As Yun pointed out on Wednesday, the five-year windfall enjoyed by the average American homeowner now comes to nearly $141,000. “The record high median home price highlights how American homeowners’ wealth continues to grow — a benefit of homeownership,” he remarked.

That statistic serves as a not-so-gentle reminder that when we argue against home-buying in the context of elder GenZ and younger Millennials (and it says a lot about the state of things when rational Americans are in some cases advising younger generations not to buy a house), we’re making some fairly optimistic assumptions about their level of discipline and some fairly aggressive assumptions about the ROI on hypothetical alternative investments for money that might’ve otherwise gone towards a downpayment.

Of course, that’s hindsight talking. It’s unlikely that the typical homeowner will enjoy another $150,000 equity windfall (i.e., free money) between now and 2030. But… well, to the point above, are we being honest with ourselves when we suggest, implicitly or otherwise, that a 30-year-old with $65,000 (a hypothetical downpayment) and a $2,000 monthly rent payment can be trusted to keep that $65,000 invested and regularly invest $1,000 in monthly “savings” (i.e., the spread between the median rent payment and the median mortgage payment, which’ll anyway narrow due to rent inflation)? I doubt it. My sense is that the vast majority of young Americans leaning on that crutch will be worse off financially five years from now than if they’d just bought a house today.

And look, I hate that for young Americans. Really I do. They shouldn’t be forced to choose between making a poor financial decision or living in a house that on any objective measure (i.e., stepping outside the bubble) isn’t worth $450,000. But that’s where we are, and the situation’s made immeasurably more vexing by the fact that for a lot of younger people, the issue isn’t necessarily the downpayment, it’s the monthlies. Maybe you can come up with the $80,000 you need to buy the half-million dollar home you (don’t) want, but can you afford the monthly payment on a $420,000 loan financed at 6.85%?

“Multiple years of undersupply are driving the record high home price [as] home construction continues to lag population growth,” Yun went on, adding that “this is holding back first-time home buyers from entering the market.”

And yet, the new construction market’s oversupplied and so’s the resale market in at least some locales. Remember: Builders are sitting on the most unsold inventory since 2009. Single-family starts ran at the second-slowest pace in two years last month and have managed just one month-to-month increase in 2025. Even Yun admitted Wednesday that “some” resale markets “appear to have a temporary oversupply at the moment.”

Bottom line: It’s total gridlock in US housing. There are just too many headwinds and crosscurrents for would-be buyers to navigate, and the confusion’s prompting many to throw up their hands. That’s reflected in the huge imbalance between buyers and sellers, with the latter outnumbering the former by almost half a million, the most ever in Redfin data back to 2013.

{kind=link}

So if new construction is oversupplied (which I assume is a combination of unaffordability – rates and construction costs – and location) and existing supply is constrained, we will continue to see new starts lag. Are we setting ourselves up for more whiplash when rates drop (they have to go down eventually, right)? Is there another leg up in prices coming in the next couple years when Trump finally gets the lower rates he wants?

This hurts in another way as well. My Silent Generation mother’s house, which her and my father built and bought in 1964 just got a tax assessment increase. In one year, the house that has never been bought or sold in over half a century just had yearly property tax go up $4000 a year. Yes, she is in a high tax state, but the county assessed the value of the house rose $250k in 2 years to be paid by the same fixed income…

I don’t know what state you are in but my state caps the annual tax increase at 2% so when there is a run up in housing prices, the tax bill continues to increase for years after the market peaks. This causes a lot of discontent from people who don’t understand how this works.

Home ownin’

https://www.tiktok.com/@jessewelles/video/7407448801465699614

Nominal home price gains are running behind inflation, nominal incomes and mortgage rates. The market is now pretty much flat and is in the process of correcting in real terms. That is the kindest correction. Imagine if we got a major nominal correction? That kind of deflation is not good for anyone- banks, sellers and yes buyers. The backdrop in that scenario is a major recession. A sharp correction is in the category of the cure being worse than the disease.