On Thursday, a Fed pondering the outlook for the US economy received two potentially impactful data points.

One of those data points was the September CPI report. There are a lot of adjectives you can fairly use to describe that release. “Good” isn’t one of them. Neither is “favorable.” “Mixed” works if you’re feeling generous. “Concerning” works if not.

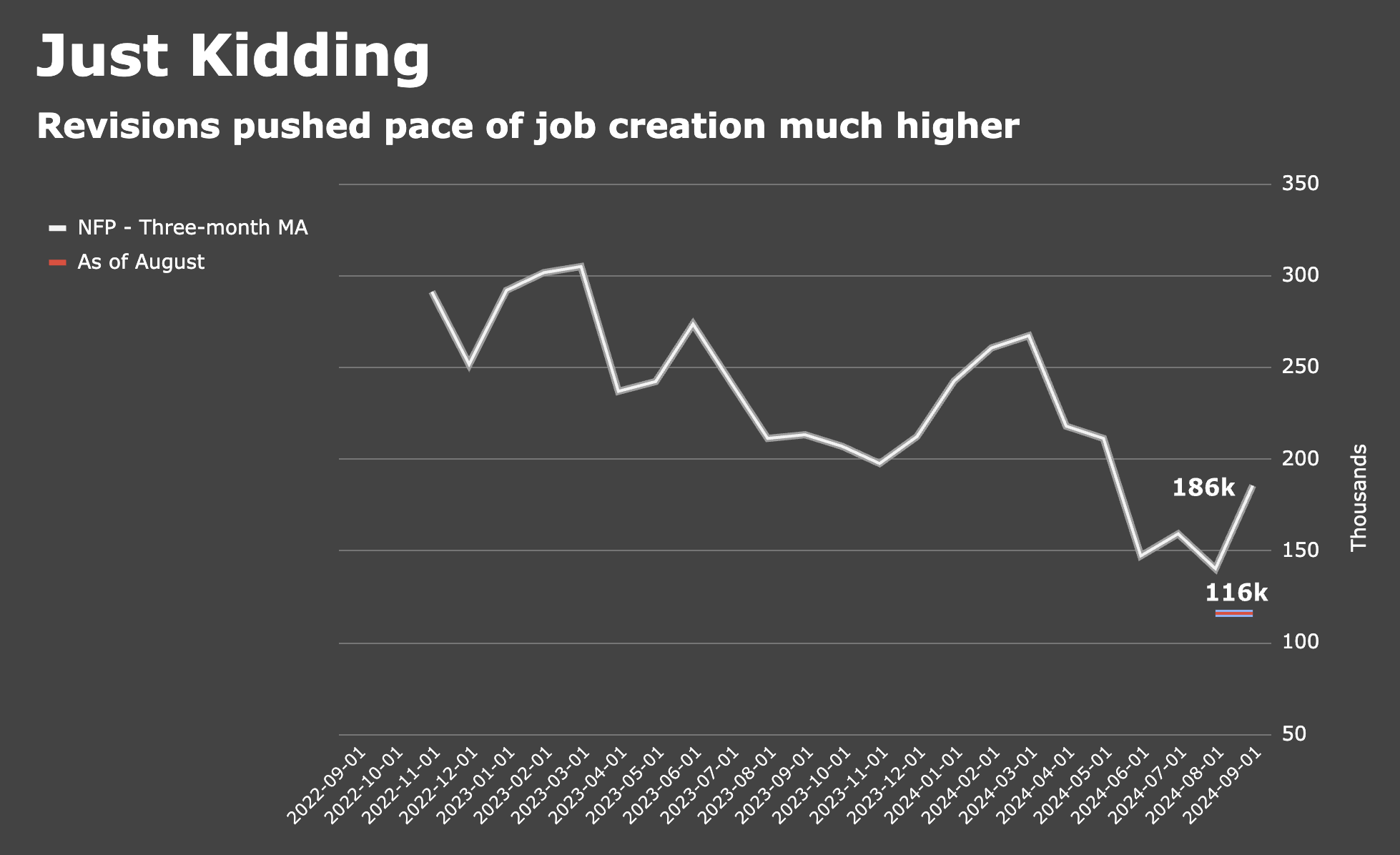

The other data point was jobless claims for the week to October 5. They rose. A lot. By 33,000 to be exact, the largest week-to-week increase in more than three years. The headline filers print, at 258,000, was the highest since August of 2023.

The big increase pulled the three-week moving average up to 231,000.

Any time you see an anomalous inflection like the one illustrated above, your first question should be: Has something unusual happened recently that might’ve caused this? The answer here’s obviously “yes.” There were hurricanes, one of them really bad. And on the off chance you don’t live in Florida and haven’t checked the news in the past 48 hours, another one just tore a path across the “free state” of Ron.

I don’t know about anybody at the Fed, nor about all of the “experts” quoted by the mainstream financial media on Thursday, but the very first place I’d be inclined to look if I were interested in explaining an otherwise inexplicable jump in weekly jobless claims is the state where scores — tens of thousands, at least — of people just lost their livelihoods to an aggressive shoulder tap from Mother Nature.

The chart above shows unadjusted initial claims in North Carolina, parts of which are still being governed on a caretaker basis by Aquaman. You’ll have to ask an economist whose credentials are current, but my suspicion says the spike highlighted in red isn’t a coincidence.

To be fair, Michigan showed a large increase too but… well, do I really have to finish that sentence? Hurricanes — and the lives they take, black, white and every color in-between — matter.

The US labor market data, the reliability of which was already the subject of considerable debate post-pandemic, will be even less dependable and more volatile in the weeks ahead given recent weather events. NFP survey week for October will capture the aftermath of both Helene and Milton.

There are a couple of ways you can look at this if you’re the Fed. Here they are:

- If you’re determined to cut again in November, you could argue that the September jobs report didn’t change the overall trend in the labor market (even though it plainly did) and that if anything, the hurricanes are a reason to err on the side of easier policy given the adverse effects on people’s economic lives. Besides, claims could be artificially suppressed in the weeks ahead if people who need to file can’t because they’re — you know — stuck on a roof or doing their best Thor Heyerdahl impression across one of North Carolina’s great oceans or practicing for a gondolier exam in Florida.

- If you’re truly data-dependent, and thereby aren’t determined to cut again in November in the absence of evidence to make the case, you might argue that in consideration of i) upside surprises to every, single line item that counted in the September jobs report, ii) yet another warm core CPI release, iii) what’s sure to be a robust advance read on Q3 GDP later this month, iv) the meaningful revision to the BEA’s income series, and given the impossibility of deriving anything like a signal from the noise that’ll invariably define the next several jobless claims releases, not to mention October payrolls, a pause in November isn’t just the right decision, it’s the only decision people who’re ostensibly concerned about being taken seriously can make.

The idea — and this was floated on Thursday and also in the wake of the September jobs report — that the Fed would somehow damage its credibility by not following through on expectations for another rate cut in November ignores the fact that rate cuts aren’t supposed to be based on traders’ policy expectations. They’re supposed to be based on data.

For a Fed that wants to preserve whatever inflation-fighting credibility they managed to win back since 2022, I can scarcely imagine a worse decision than forging ahead with rate cuts in the dark two days after a highly contentious US presidential election. That’s a policy suicide mission and importantly, it’s completely unnecessary.

The whole point of cutting 50bps out of the gate last month was to ameliorate the urgency. If the situation turns out to be urgent, there’s another meeting in December. The Fed can always cut 50bps at that meeting, when they’ll have the new SEP for air cover should they need it.

{kind=link}

+1

Years another great piece of analysis and writing. Thanks!

Boom:

*BOSTIC SAYS DOOR OPEN TO SKIPPING RATE CUT IN NOV.: WSJ

*BOSTIC: COMFORTABLE ‘SKIPPING A MEETING’ IF DATA BACKS THAT

And so it begins.

Love the Thor Heyerdahl reference.

Yeah, I had to google that one. I always enjoy a good dive down the Wikipedia rabbit hole.

Surely no pun was intended when you wrote about an idea being “ floated”.