“It’s vital,” Andrew Bailey said Thursday, after the Bank of England left rates on hold at its September policy gathering, “that inflation stays low.”

As BoE decisions go, this one admitted of something that looked vaguely like unanimity. It had the trappings of consensus. Only Swati Dhingra voted for another cut. The BoE, you’re reminded, cut rates for the first time since the pandemic at the August meeting, at which four dissenters preferred to hold Bank rate at the highest since 2008.

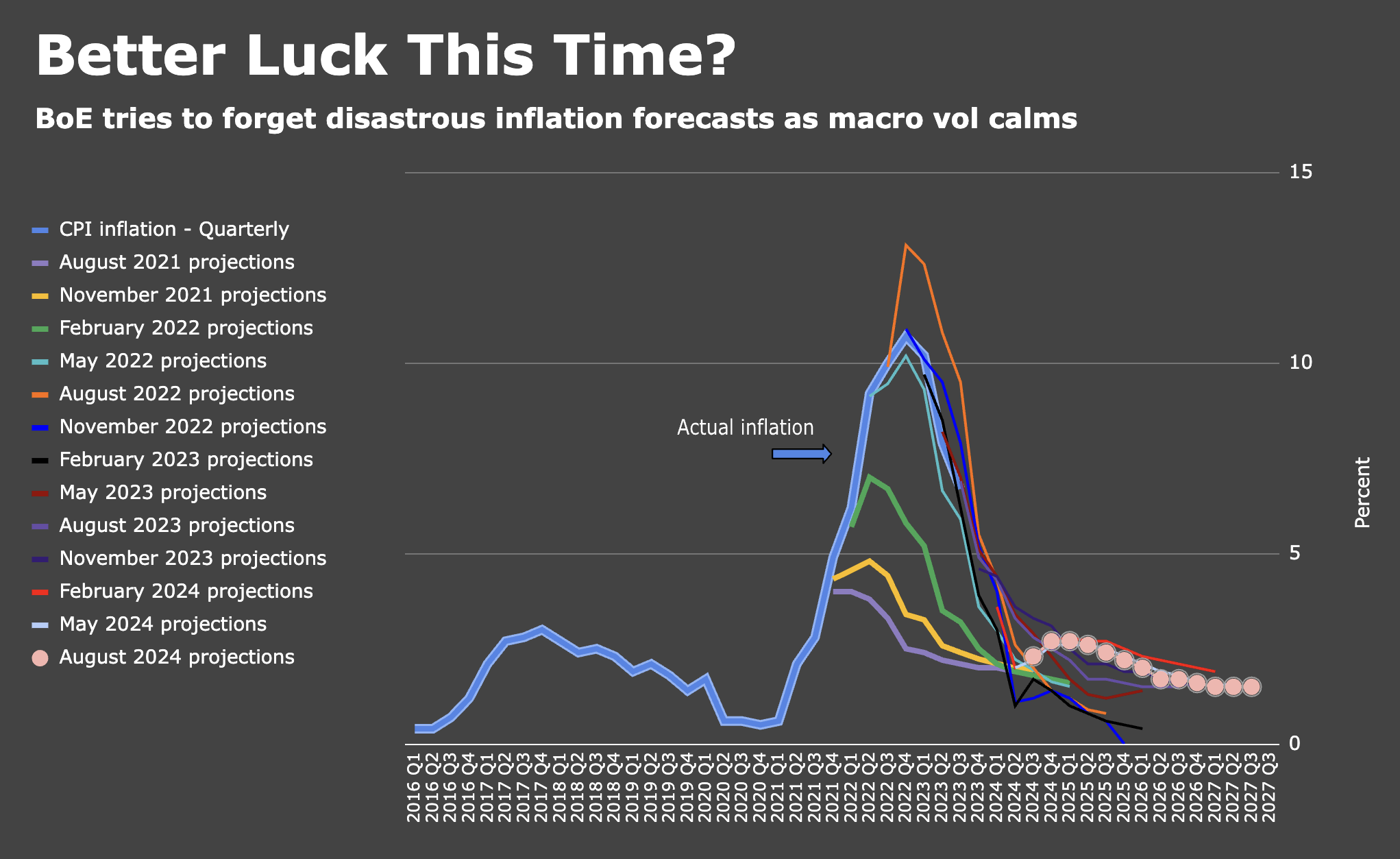

Among advanced economies, the UK arguably had the toughest time grappling with back-to-back macro shocks in the pandemic and the outbreak of full-on war in Ukraine. Liz Truss’s star-crossed, and ultimately disastrous, tenure at No. 10 didn’t help.

Earlier this month, the BoE released its latest quarterly survey of public attitudes. Among other things, the poll queries voters on whether the bank’s “doing its job to set interest rates to control inflation.” The responses to that question are used to construct what amounts to a public approval rating. As the figure above shows, the August vintage showed a positive net satisfaction balance for the first time since early 2022.

Bailey doesn’t want to squander that hard-won goodwill. “We need to be careful not to cut too fast or by too much,” he said Thursday.

Although inflation finally receded in the UK, price growth in the services sector remains quite brisk. In August, services inflation ran 5.6%, up meaningfully from the prior month’s annual rate.

I don’t want to be disingenuous, but neither do I want to present as any sort of Pollyanna. The uptick on the services gauge was expected, and 5.6% is lower than the BoE’s forecast. Further, the bank, as well as private sector economists, expect the re-acceleration to be a fleeting affair. But that glosses over the simple reality that 5.6% is too damn hot, particularly for a services-driven economy.

Simply put: Policymakers can’t be confident in stable headline price growth if services inflation sports a five-handle, let alone a six-handle. Those aren’t mandate-consistent readings. And the BoE, you’ll kindly note, has a single mandate (a “primary objective” to keep inflation low and stable that comes before all other aims). Here’s what the MPC minutes had to say on services inflation:

The Committee discussed momentum in services price inflation and price-setting behavior in firms. Strength in services price inflation was supported by evidence from the DMP Survey which showed firms’ own-price inflation continuing to fall, but to a lesser extent among services firms. July CPI microdata pointed to a higher proportion of services prices being raised each month than was the case pre-COVID, though with some easing in catering services where food input costs had moderated. The monthly annualized inflation rates of a seasonally adjusted services price measure, which excluded indexed and volatile components, rents and foreign holidays, had averaged around 4% in the three months to August, close to its average since the end of 2023. Although it had fallen from its peak level, the apparent stability in this measure suggested further pass-through from lower labor costs and easing inflation expectations was still to come. Accordingly, Bank staff expected services inflation to ease slightly further in Q4.

Draw your own conclusions. Make your own forecasts. Yours can’t possibly be any worse than the BoE’s.

Anyway, Bailey’s data dependent. Actually data dependent. Or at least he does a decent job of pretending. “In the absence of material developments [since the last meeting], a gradual approach to removing policy restraint remains appropriate,” the BoE said Thursday, explaining the near unanimous decision to stay on hold. “Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further.”

Markets didn’t expect a second cut today, and the somewhat cautious forward guidance prompted traders to trim bets on the scope of additional 2024 easing, although I think 50bps (i.e., 75bps of total 2024 cuts inclusive of the August move) is probably a lock.

As for the bank’s big QT decision, the vote was 9-0 in favor of maintaining the £100 billion annual runoff target. As a quick reminder: The BoE’s QT effort involves both passive runoff and active sales. Maturities are about to go up dramatically, which means that in order to keep the overall rate of QT stable, the BoE will need to pare back active selling, which is what they decided to do on Thursday. The other option would’ve been to keep active sales steady even in the face of larger maturities, but that would’ve meant a meaningfully higher annual QT run rate.

Tellingly vis-à-vis the Fed’s 50bps cut and (narrow) inclination to deliver another 50bps by year-end, the pound was the strongest since early 2022 on Thursday.

{kind=link}