Jackson Hole’s on deck.

That’s pretty much all you need to know about the third week in what’s already been an extraordinary month for markets. The theme for this year’s festivities is “Reassessing the Effectiveness and Transmission of Monetary Policy.”

Jerome Powell will speak from Wyoming at 10:00 AM ET on August 23. Obviously, he’ll confirm the Fed’s intention to start dialing back whatever degree of restriction current policy settings are exerting on a US economy that by and large refuses to submit.

Data since the last US jobs report was generally constructive, and the early August growth scare was a bit of a false optic in my view. There is evidence to suggest elevated rates are having an effect, though, and not just in housing. The figure below shows early delinquency transition rates for credit cards (in blue) and serious delinquencies for the 18-29 cohort (in grey).

Although still nowhere near GFC levels, delinquencies are rising. The share of 90-day past due accounts among young adults is in the double-digits now.

“The rate at which total household debt is flowing into early delinquency is still solidly below anytime before the pandemic [but] there’s been a clear and consistent increase in the pace at which borrowers are missing payments,” BMO’s US rates team remarked, editorializing around aggregate delinquencies from the same NY Fed data. “Households are becoming increasingly concerned about falling behind on their debt payments in the coming months.”

Still, between the anomalously easy financial conditions that prevailed in 2020 and 2021 as fiscal and monetary policy responded to the pandemic and structural factors unique to the US economy (where that basically just means the prevalence of the 30-year fixed-rate mortgage), the monetary policy transmission mechanism was in some respects inhibited this cycle.

Recall that as of end-2023, the effective rate on the nation’s mortgage stock was just 3.8%, up a mere 0.5ppt from the all-time low reached in Q1 of 2022.

So, ~70% of US household debt sports a three-handle fixed rate. That’s guaranteed to blunt the impact of rate hikes, and when you consider that well-to-do households are getting paid 5% on their savings cushions, it’s not at all surprising that spending continues to hold up.

Effectively, the Fed’s leaning on the lower-end of the income distribution to facilitate the disinflation process. That’s where there’s less home equity, less savings and more sensitivity to variable-rate debt. It’s also where job security tends to be tenuous. The same’s true on the corporate side. Junk-rated companies have a steeper maturity wall and less cash, while small businesses have no access to capital markets and are thus dependent on loans priced off the prime rate.

In other words: The harsh reality of the Fed’s tightening campaign is that the burden falls disproportionately on the economy’s “have-nots,” who are effectively asked to suffer for their own good: Because inflation disproportionately affects them too.

All of that should come up at any symposium dedicated to “reassessing the effectiveness and transmission of monetary policy,” and some of it will come up. But the brutality and inequity of the situation won’t get top billing, if it gets a mention at all.

Anyway, the big question about the September FOMC meeting is obviously whether the Committee will go for 50 right out of the gate. Spoiler alert: Powell won’t answer that question this week.

I can assure you there’s nothing like consensus on the Committee currently about the relative wisdom of “going big,” which is to say the odds currently favor a 25bps cut. The Fed will see another jobs report and another CPI update before next month’s meeting. My intuition is that it’d take a sub-50k headline payrolls print to get the Fed to 50 in September absent some additional market shock.

Traders will also listen for any hints from Fed officials about the evolution of rates beyond September and/or any nods to a QT wind down. Minutes from the July FOMC meeting are due Wednesday, for whatever that’s worth to you.

The data docket’s sparse: The BLS will deliver its first pass at revising the payrolls benchmark, preliminary PMIs are due Thursday and there are a pair of housing updates due (existing home sales on Thursday and new home sales on Friday).

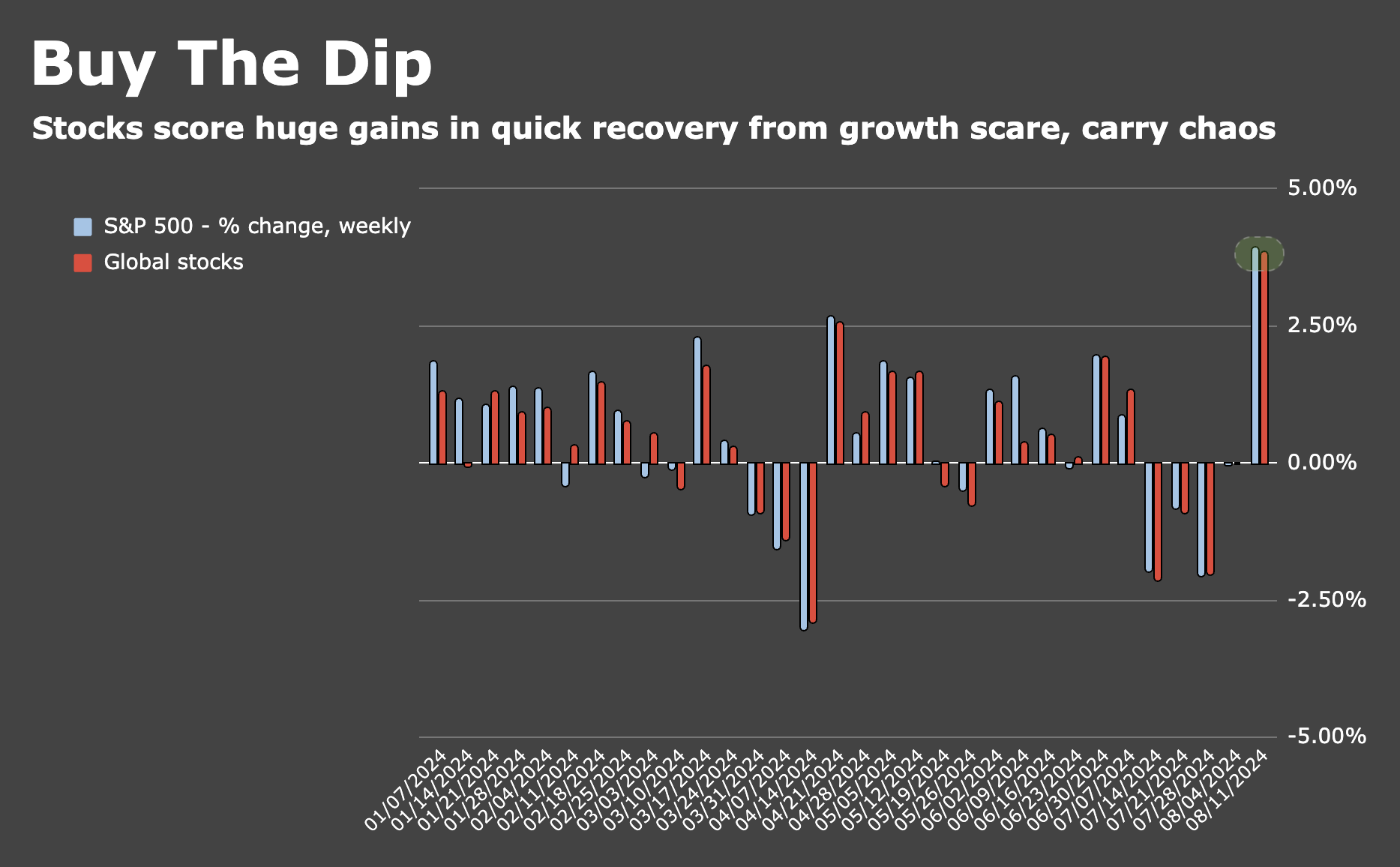

Equities — both US and global — are coming off their best week of 2024.

{kind=link}

Some who read this will probably consider my comments unfair and cynical, but from who and what I see, my guess is that most of the younger half of the population with rising debt problems has those problems because they lack self-control, not because interest rates are 3.5-5%. They want everything their friends have and a bit more. No one “needs” four or five cell phone lines to play games on with expensive data plans. Two or three cars cost money, especially when they carry good insurance. One of my hot buttons is these now common ads for debt collection companies. “I had $50,000 in debt and I didn’t know how I was going to pay for food.” Easy answer, by keeping your wallet in your pants (or purse), by not “refreshing” your wardrobe every six months. Then the deadbeats they tell you how so and so company made half their debt go away. As far as I’m concerned that’s stealing. No difference between buying stuff you don’t pay for or stealing it to sell. Someone does, in fact, have to pay for all these deadbeats and it comes in the form of higher prices, lower earnings and other effects. Nothing is free. Debts don’t go away magically; we all pay. To all the delinquents out there who can’t control themselves, wait your turn. Earn your rewards. Stop stealing them.

That’s a funny one, Lucky. Though I’m very far from young, I can still be old and naive at times. I was once, indeed, young and naive. Furthermore, I lived in a time of sparse wealth for everyone. So I had to try really hard to hurt myself. And when I erred, the pain wasn’t so profound.

I learned and moved on. But how does a young person with significant cash in his pocket learn how to manage it without making mistakes? Financial mistakes are necessary in anyone’s learning.

It’s a free country. All of us armchair traders who may have taught ourselves about how to pick stocks and manage a portfolio have had to learn lessons from time to time.